Image © Pavel Ignatov, Adobe Images

- BRL has risen over 10% in September

- Markets approve of choice of next president

- Implementation issues a probable spoiler

The Brazilian Real is forecast to fall in the second half of 2018 as hopes that a new right-wing administration will deliver much-needed fiscal reforms fall on hard ground, as they encounter 'blockages' and implementation delays.

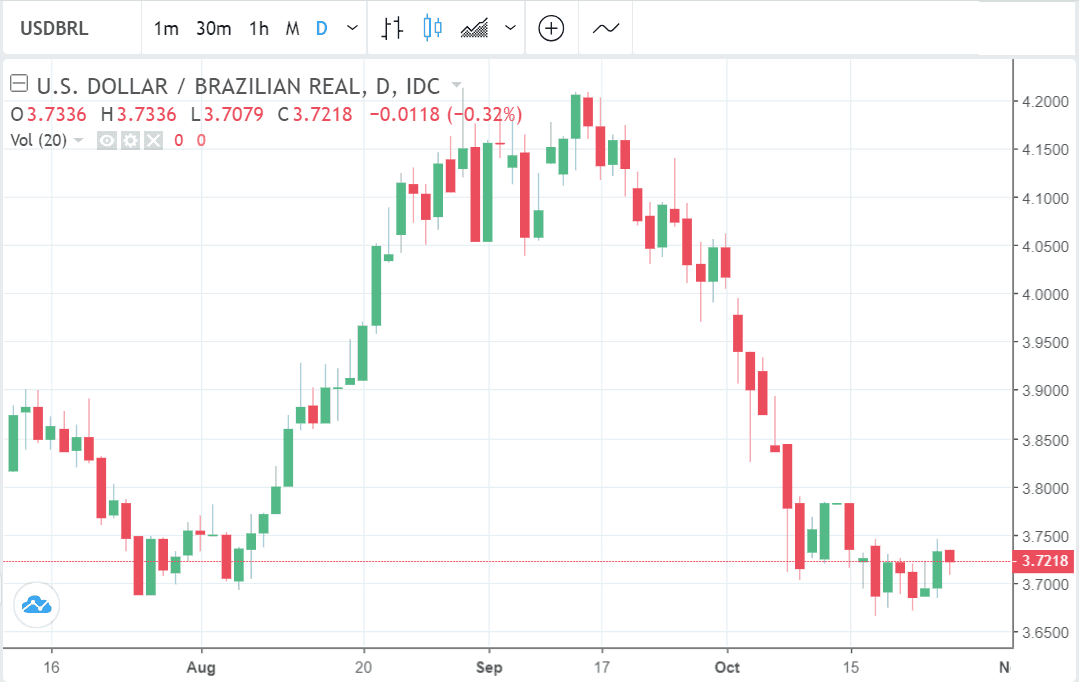

The Real has clawed back some of the loses it suffered at the hands of the rampantly appreciating US Dollar in the first half of 2018, recovering an impressive 11% in September alone, as it became increasingly clear that the next president of Brazil was going to be the market's favourite, Jair Bolsonaro.

Above: The Real has been in recovery mode against the Dollar since mid-September.

Although the elections are officially not yet complete - the final round is on Sunday, October 28 - Bolsonaro has won the heats so convincingly and is so far ahead in the polls, that everyone is convinced he will win.

So sure is the market Bolsonaro will win that the news has already been absorbed by the Real in its recent rally and the actual result is not expected to have much of an impact.

"Strategists say most of the optimism is already priced in by investors counting on him to restore the country’s finances with a series of fiscal measures," say Aline Oyamada and Felipe Saturnino, correspondents for Bloomberg news.

If anything some analysts think that there is a chance the Real could actually fall after the election result, even if the winner is Bolsonaro, in a version of the familiar 'buy the rumour; sell the fact' Wall Street strategy.

After an almost 10 percent advance this month - the biggest among the world’s major currencies - the real is poised for a reversal after Brazilians vote Sunday to pick the next president, according to Commerzbank AG’s You-Na Park and RBC Capital Markets’s Tania Escobedo, the two analysts who topped Bloomberg’s accuracy rankings this year.

Their view is further backed-up by Mauricio Oreng, a strategist at Rabobank, who argues most of the "electoral/fiscal idiosyncratic risk premium" has now been "recouped".

"Our models seem to confirm the perception that this rally follows a reduction of risk premium in Brazilian assets, as financial markets take a sanguine view on the next administration’s willingness and ability to both to maintain a credible economic policy," says Oreng.

Risks from Blockages and Delays

For the Real to sustain its uptrend Bolsonaro will have to prove he can 'walk-the-walk' as well as 'talk-the-talk' and this is not expected to be easy.

Once traders wise up to the gap between reality and fantasy real-politic could take a scythe to the Real.

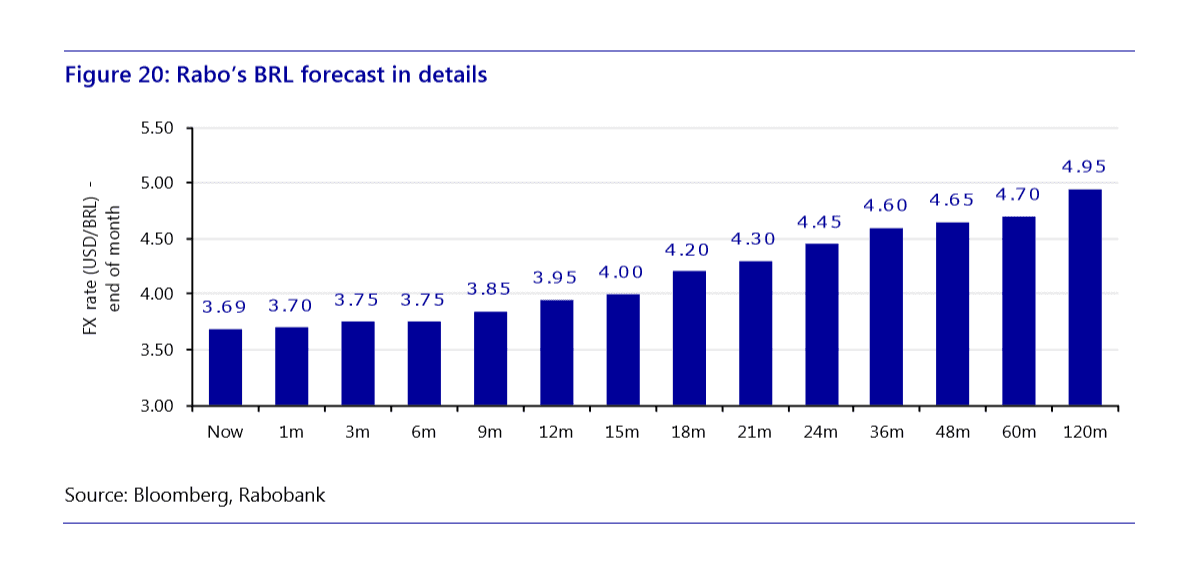

Rabobank's Oreng sees "execution risks ahead" as Bolsonaro struggles to pass his reforms through a divided lower house.

"We see relevant execution risks ahead, so that we look for FX rate at 3.80 for end-2018 (with huge downside risks) and at 4.00 for end-2019 (with risks skewed to the upside)," says Oreng.

To make matters worse, the Brazilian congress is considered one of the most challenging political arenas in the world.

"By any international standards, Brazil’s congress is fragmented, unruly and brutal, with dozens of parties vying to promote their pet projects and interests," say the Bloomberg correspondents. "While Bolsonaro’s PSL party saw its ranks swell to 52 seats from eight in the 513-member lower house, he may struggle to get bills approved and will have to build alliances in a difficult environment."

Park and Escobedo are even more cognizant of the risks the new administration faces in getting its reforms through parliament.

Escobedo notes the lack of political experience amongst Bolsonaro's top advisers as a potential stumbling block.

"There is plenty of space for disappointment there, as the lack of political experience from Bolsonaro’s cabinet will probably get in the way of reform," says the strategist.

Even the highly considered financial brains of Bolsonaro's team, finance minister Paulo Guedes - who is one of the founders of Rio de Janeiro-based private equity firm Bozano Investimentos and a University of Chicago-trained economist - nevertheless, lacks real political experience.

Park, meanwhile, sees the Real as likely to be dogged by high levels of uncertainty during the early period of the Bolsonaro regime.

“There will be some uncertainty in the first months of his presidency and there might be some potential for disappointment regarding fiscal consolidation and pension reform,” says Park.

“There is still a lot of uncertainties regarding Bolsonaro.”

In the near-term there may also be a down-draught for the Real, which is currently trading at 3.72 to the USD and 4.80 to the Pound, caused by the removal of FX support by the central bank, says Rabobank's Oreng, who notes FX swap redemptions on the horizon, and says these could, "trim a bit of BRL momentum in the short-term."

Above: The Pound has been under pressure against the Real over recent weeks.

Commerzbank's Park forecasts a temporary strengthening after the election to 3.6 Real to the Dollar, but then a depreciation into year-end leading to a 3.9 at the start of 2019.

RBC Capital Markets’s Tania Escobedo, meanwhile, forecasts the Real to strengthen even more in the aftermath of Sunday's election, "overshooting" to 3.5 followed by a period of depreciation to 4.2 after 3-months.

The same effect is likely for GBP/BRL although Sterling weakness may complicate the picture in the absence of a Brexit compromise.