Image © Adobe Images

"Worries towards the status of the USD can ease as fast as they arise" - Nordea Markets.

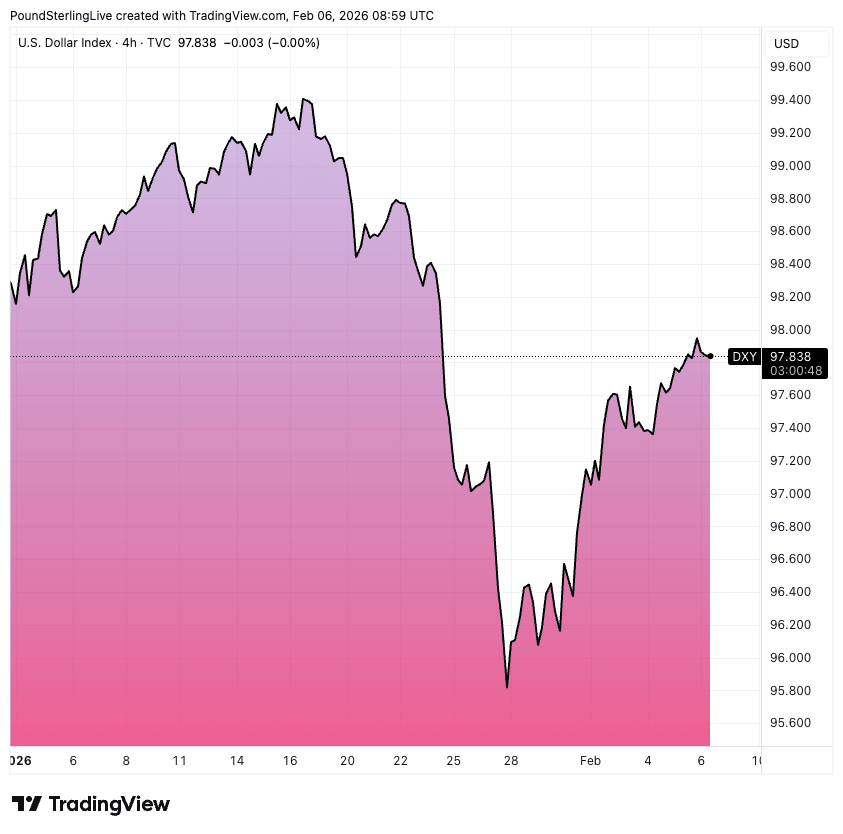

The U.S. dollar is not showing signs of imminent collapse, with recent rebounds against the pound, euro and the yen highlighting how quickly market fears around US policy and reserve-currency status can unwind.

"Such moves once again suggest that the USD is not on the verge of collapse and worries towards the status of the USD can ease as fast as they arise," says a new research note from Nordea Markets.

Price action in major dollar pairs indicates that episodes of sharp USD selling, driven by political uncertainty or intervention speculation, continue to fade once official signals and relative yield dynamics come back into focus.

“EUR/USD saw a big jump in late January, first driven by renewed concerns about the USD outlook amidst increasingly uncertain policies from the US administration, and then by speculation of FX intervention to support the JPY,” Nordea Bank says, linking the move to both US political risk and developments in Asia.

Speculation around yen support reflects the long-standing sensitivity of USD/JPY to sharp moves, with markets historically alert to the possibility of coordinated or unilateral action when yen weakness or strength becomes disorderly.

Above: The USD rebounds.

“Such interventions were denied by the US Treasury Secretary, and the JPY has started to weaken again, while the USD has rebounded clearly also against the EUR,” Nordea Bank says, describing a sequence familiar to currency traders once official pushback dampens intervention expectations.

Dollar recoveries following denied or absent intervention have been a recurring feature of G7 FX markets, reinforcing the idea that shifts driven by speculation rather than policy action tend to unwind quickly.

“Such moves once again suggest that the USD is not on the verge of collapse and worries towards the status of the USD can ease as fast as they arise,” Nordea Bank says, framing the rebound as evidence of the currency’s continued central role in global markets.

Highly accurate consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

Reserve diversification and hedging against US-specific risk remain active themes among investors, however, particularly as geopolitical fragmentation and fiscal debates persist.

“That said, we continue to think the USD will weaken further going forward, as investors continue to seek alternatives to the USD, even if such a moves will not take place on a one-way street,” Nordea Bank says, emphasising a gradual rather than abrupt adjustment.

Institutional developments in Washington also shape dollar expectations, especially when markets assess potential implications for Federal Reserve independence and the future path of US interest rates.

“In financial markets, Warsh was probably perceived as the lesser threat to Fed independence among the candidates under consideration, and in the end his nomination came as a small surprise,” Nordea Bank says, reflecting how closely FX and rates traders track governance signals.

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

Perceived threats to Fed independence have historically influenced US yields and the dollar by altering expectations for inflation control and policy credibility.

“Looking at Warsh’s policies overall, they would likely be in line with lower short rates and possibly higher long yields,” Nordea Bank says, outlining a policy mix that markets often associate with steeper yield curves.

“They could at least initially boost the equity market (lower rates and less regulation), while the impact on the USD would probably be in net somewhat negative (lower short rates could weigh more than higher growth would help),” Nordea Bank says, reinforcing its view that near-term resilience does not preclude longer-term dollar softness.