Image © Adobe Images

New research shows the market is vastly underestimating the work the Federal Reserve must do.

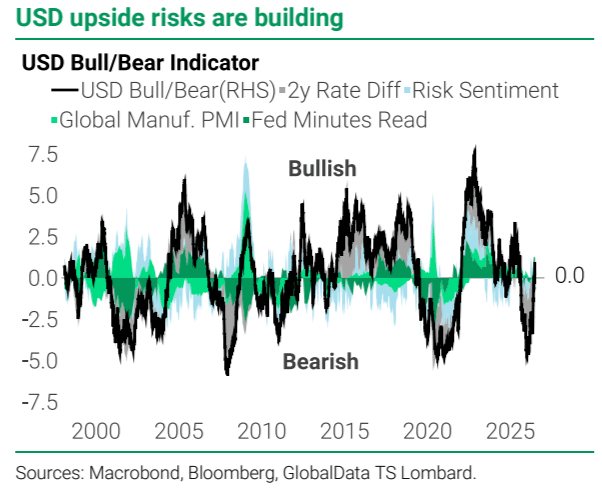

The dollar could be entering a far more powerful rally than markets currently anticipate if the Federal Reserve embarks on a full tightening cycle rather than the single 'recalibration' hike investors have priced.

That is the view of TS Lombard, which has shifted to a bullish stance on the greenback after concluding the U.S. labour market has turned a corner.

"We move to a positive stance on the dollar as US hiring seems to be at an inflection point," says Daniel Von Ahlen at TS Lombard.

The call stands in sharp contrast to current market pricing: while investors largely expect one corrective rate hike before the Fed resumes cutting rates, TS Lombard thinks the central bank is at the beginning of a sustained tightening cycle.

The independent research house expects the first increase in September, followed by four more next year, taking the total to five hikes.

That outlook rests on a combination of strengthening employment and stubborn inflation.

"Our view of a sustained rebound in the US labour market and sticky core services ex housing inflation" underpins the forecast, says Von Ahlen.

"Core services inflation ex housing remains sticky and the fact that the labour market is rebounding cannot instil confidence in the FOMC that inflation returns to target," he adds.

The implication for the dollar is significant, "we reduce portfolio risk to take into account a looming Fed tightening cycle, a stronger dollar and weaker global growth signals."

Markets Are Not Ready For This

TS Lombard argues foreign exchange markets continue to underestimate the risks; “the market sees the Fed cutting rates again after a near-term ‘recalibration’," reflecting expectations that Fed Chair Kevin Warsh will ultimately talk markets back towards lower yields.

TS Lombard explains that the reason for the underestimation by investors is a belief that slowing wage growth, moderating inflation measures and the longer-term disinflationary effects of artificial intelligence will prevent a prolonged tightening cycle.

"If this view turns out to be wrong, bond yields would face meaningful upward pressure and could cause stocks to wobble," says Von Ahlen.

That combination would reinforce demand for the dollar through both higher yields and a more defensive market backdrop.

The firm also notes that the Fed’s abandonment of explicit forward guidance has increased uncertainty over the future path of policy, leaving markets more exposed to incoming economic data than in previous cycles.

For now, TS Lombard believes investors have not fully appreciated the implications of a strengthening labour market.

"USD upside risks are building," says Von Ahlen.

If he's right, the biggest adjustment may not be in the bond market, but in currency markets, where investors remain positioned for a Fed that pauses after one hike rather than one that is only just getting started.

The Fed's Hawkish Surprise

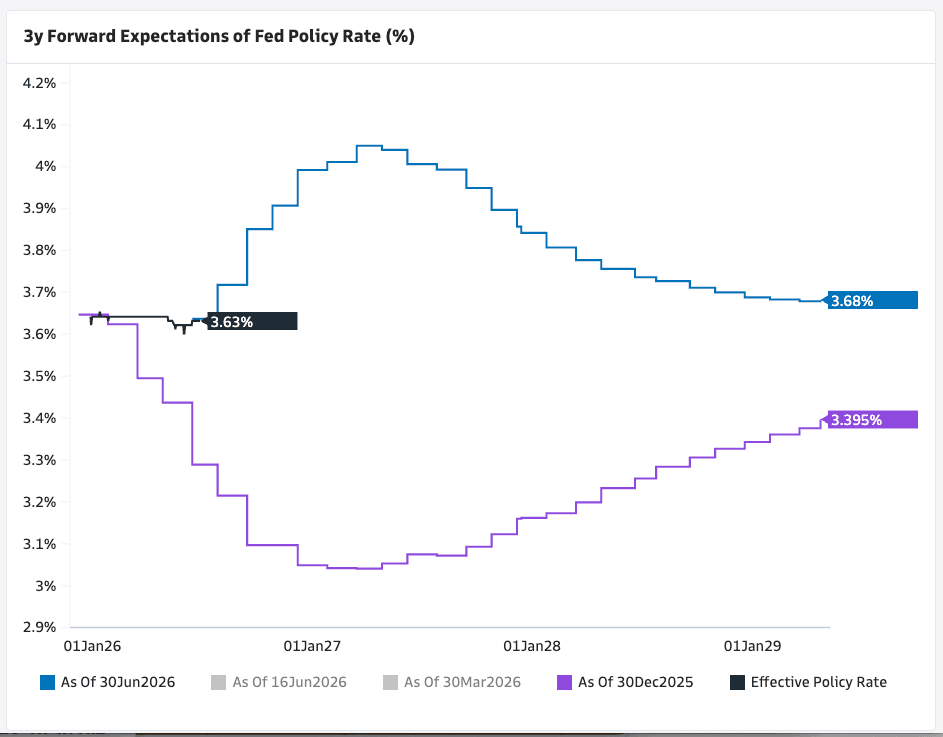

As the above shows, the market has already moved a long way in 2026, from expecting a series of rate cuts to now expecting a hike.

The odds of that hike grew markedly when new Fed Chair Kevin Warsh reaffirmed the Fed's inflation-fighting objectives under his guardianship, which calmed fears that he would be more open to tolerating higher inflation in order to guarantee strong economic growth and employment.

That commitment to the inflation mandate reduced any negative premium weighing on the dollar due to fears of institutional erosion. But it's the rates story that will ultimately determine the length and strength of a dollar rally.

"The hawkish outcome of the June Fed policy meeting has been the most important recent event for FX markets, helping propel the USD to its highest level in more than a year of late," says Valentin Marinov, Head of G10 FX Strategy at Crédit Agricole.

Numerous institutional-grade studies are showing the same thing: rate differentials are increasingly important for exchange rates, and five Fed rate hikes would almost certainly bolster the dollar's rate advantage, particularly against currencies belonging to central banks that oversee weaker economies.

The pound and euro could be disadvantaged, as neither the ECB or BoE look to have scope to match an agressive Fed hiking cycle.