Image: Federal Reserve.

The Fed and ECB are leaning hawkish; the pound will fall if the Bank of England ignores them.

Currency markets were caught by surprise when the new Chairman of the Federal Reserve, Kevin Warsh, showed he would still prioritise the central bank's fight against inflation above all else, and that raises the prospect of an interest rate hike in the near future.

Clearly, the market had other ideas: after all, he was appointed by President Donald Trump, who continuously harried the previous Chair, Jerome Powell, to lower interest rates.

The Fed kept rates unchanged Wednesday and released a statement reaffirming its focus on price stability and released a new dot plot projection chart that showed 9 of 18 governors favour rate hikes this year, as they raised their inflation projections.

"Persistently high prices are a burden for the American people," said Warsh during the press conference. "Members of the (FOMC) are unambiguous and unanimous: this committee will deliver price stability."

The prospect for tighter interest rates tends to raise U.S. bond yields and penalise equities, in turn hitting risk-adjacent foreign exchange pairs, such as the pound-to-euro rate, which fell for the third consecutive day to 1.1554.

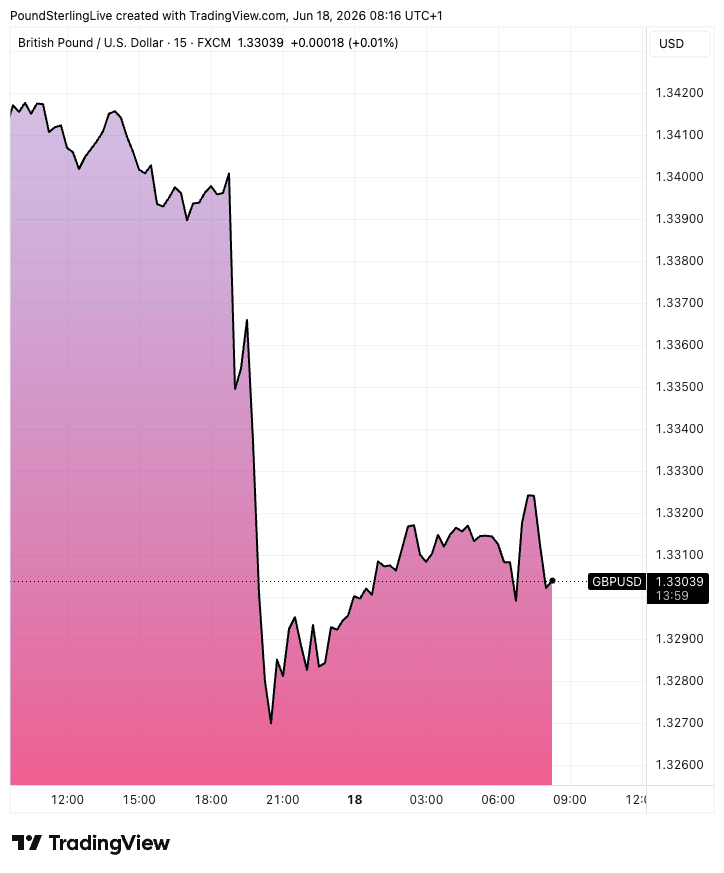

The dollar rose across the board. The pound-to-dollar rate fell 1.0% on the day to 1.3375.

Above: GBP/USD showing Fed impact.

The Credibility Premium

The first statement of the Warsh era said, "inflation remains elevated... the Committee will deliver price stability."

That's a clear-cut and watered-down statement that leaves little ambiguity as to what the Fed's doing and plans to do. Little surprise here, as Warsh has long stated the Fed's communication has to be rationalised.

What is surprising is that Warsh doesn't seem to be bothered by upsetting President Trump, who had, through 2025, tried to push the Powell Fed into lowering interest rates.

Economists warned, and markets feared, his pick to replace Powell would most likely hold a similar view.

However, it seems the President has landed himself another Chair who will prioritise the economy and the institutional integrity of the Fed above his whims.

So we're looking at dollar strength as a result of two developments: a 'hawkish' steer and a recovery in institutional credibility; the re-anchoring of the Fed under Warsh can reduce any negative premium on U.S. assets that had built up.

A Big Ommission

Perhaps the biggest sign of intent in the watered-down statement was the omission of the need to maximise employment.

The Fed's dual mandate demands that it both control inflation and maximise employment. This can seem contradictory as maximising employment is short-hand for lowering rates, and controlling inflation is short-hand for raising rates.

The omission of the employment function is therefore clearly significant. "This raises, in our view, questions about a possible change in the FOMC's reaction function," says Marc Giannoni, economist at Barclays.

"We are changing our Fed call: In light of the FOMC's hawkish turn focused on restoring price stability and the participants' upward revisions in the dots for 2027, we now expect the FOMC to maintain rates unchanged until the end of 2027," he adds.

This is a Big Deal for the Bank of England and the Pound

For the dollar, the consequences of the readjustment of the Fed's approach are constructive; for the pound, it poses a risk.

Why? Because we now face the prospect of a significant divergence in central bank policy on either side of the Atlantic and the English Channel.

The ECB raised rates last week and now the Fed is reiterating its commitment to fighting inflation; the Bank of England risks being an outlier.

"Weaker Sterling, on the perception of the BoE lagging peer central banks’ response to the energy shock, could end up leading to forecasts for higher imported inflation for the UK and be the factor that forces a belated BoE rate hike," says Sam Hill, Head of Market Insights at Lloyds Bank.

Central bank policy divergence is a powerful driver of FX and the risk is that the Bank of England leans toward a preference for lower interest rates in order to defend against rising unemployment.

Such guidance would be enough to trigger a fall in UK bond yields relative to those of the Eurozone and the U.S., which would weigh on the pound.

"Despite friendlier inflation data again yesterday, the UK policy outlook can’t be determined in domestic isolation, if other central banks are hiking it could be harder for the BoE to stand aside," says Hill.