Image © Adobe Images

Foreign demand for AI exposure is proving an additional tailwind for the dollar.

Analysts at Goldman Sachs say they began the year expecting a moderation in U.S. economic outperformance to weigh on the greenback.

Instead, an important development has altered that outlook:

"Not only has the conflict in the Middle East disrupted expectations for more notable relative underperformance, but a surge in AI momentum has also challenged that narrative," say analysts in a weekly currency strategy briefing.

According to Goldmans, the AI investment boom has driven another wave of U.S. equity outperformance, reinforcing international demand for American assets.

"The strength of the AI trade has driven another leg of U.S. equity outperformance."

Ordinarily, that would imply an even stronger dollar.

Interestingly, Goldman says the currency has actually lagged what equity markets alone would have suggested.

"If anything, the Dollar has appeared slightly weaker than expected from this perspective alone."

The bank offers three explanations.

First, U.S. equity outperformance has been less pronounced against emerging markets than against developed markets, limiting the usual boost to the dollar.

Second, markets are rewarding long-term earnings power rather than short-term upgrades.

"We find evidence that durability matters: sharp upgrades to near-term US earnings expectations do not generate as much Dollar demand as more sustained earnings power would."

Finally, the AI rally remains concentrated in a relatively small number of technology companies. "Narrow equity market breadth appears to limit FX spillovers."

Even so, the broader conclusion is constructive for the dollar and Goldman argues that equity performance is an important signal for international capital flows, which ultimately help determine exchange rate trends.

The bank says this year’s AI-driven rally may exaggerate the degree of U.S. economic outperformance, but it has nevertheless transformed equities from a potential headwind into a tailwind for the currency.

"The broader equity impulse has clearly shifted from an expected drag to a source of support for the Dollar."

The Fed Story is Still Pre-eminent

To be sure, the AI-demand driver will likely prove of secondary importance to the rates story as it's widely understood that building bets for a Fed rate hike later in the year (and maybe even four more next year) are foundational to recent USD strength.

So although the AI-dollar link is real, it is the slower, structural, capital-flows undercurrent, not the week-to-week driver.

AI is the reason the dollar has a structural bid beneath the cyclical noise, turning "U.S. exceptionalism" from a slogan into a balance-of-payments reality.

Global investors who want exposure to American AI equity and credit have to buy dollars to do it, and the scale of that demand is now enormous.

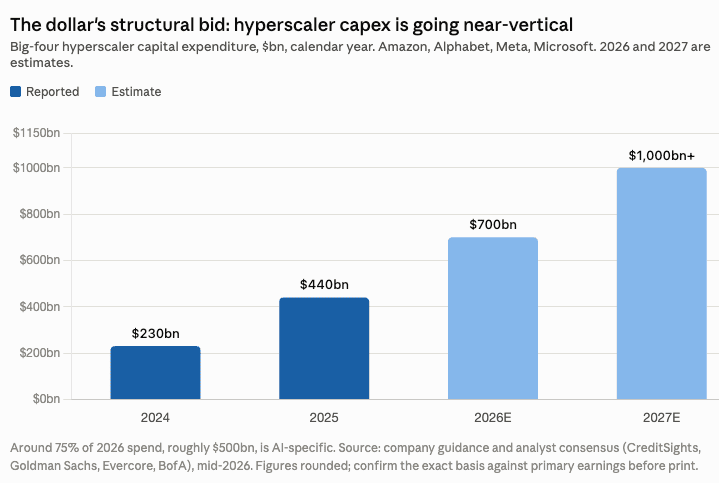

The Scale of the AI Boom

The numbers are genuinely without modern precedent:

- The five largest US hyperscalers (Microsoft, Alphabet, Amazon, Meta, Oracle) are committed to roughly $600–700bn of capex in 2026, up between 36% and 60%-plus year on year depending on whose cut you use.

- Around 75% of that, some $450–500bn, is AI-specific.

- Each of the four largest now exceeds $100bn in annual capex individually. Amazon around $200bn, Alphabet $175–185bn, Meta $125–145bn (roughly doubled from $72bn in 2025).

- As a share of the economy, hyperscaler AI capex is put at roughly 1.6% of US GDP for 2026 (some framings using the Magnificent Seven reach ~2%). For context, that rivals or exceeds the dotcom-era peak on a spending-to-GDP basis, though valuations are far tamer than 2000.

- Capital intensity has hit 45–57% of revenue at the big four, ratios that belong to utilities and heavy industry, not software.

- Wall Street now models 2027 total AI capex above $1 trillion (Evercore and BofA both went there after Q1 earnings).

- The BIS says the five biggest hyperscalers will spend over $1 trillion on AI capex across 2025–2026 combined, increasingly funded by debt rather than cash flow