The US Federal Reserve policy decision on Wednesday is forecast to give fresh impetus to foreign currency markets this week.

The next phase in the US dollar's evolution will be determined by the outcome of the upcoming US Federal Reserve policy meeting will determine whether the US dollar’s poor June extends - Fed funds markets are assigning a zero probability of an interest rate in June but they will be looking for hints that a July rise will take place.

If this is the case, then the prospect of a second rate rise in 2016 becomes possible - something that will be music to the ears of dollar bulls.

The promise of higher US interest rates in the future remains the life-force behind the dollar’s multi-year cyclical upturn which has stalled over recent months.

With no interest rate rise forecast this week markets will be scrutinising the wording and tone of the accompanying statement.

“The likelihood is we see a repeat of Janet Yellen’s recent speech: that they want to put up rates, but it purely depends on the outcome of potentially destabilising events, such as the UK referendum. The Fed will be happy to raise with corporate credit spreads narrowing, but the US yield curve is a clear issue at 91 basis points. Falling inflation expectations are a huge concern, not just for the Fed but many other central banks,” says Chris Beauchamp at IG in London.

IG is expecting a slight downgrade to their growth forecasts for 2016 and 2017, with a shift lower in their view on where interest rates are likely to head in 2017 and 2018.

“Recall, interest rate traders are positioned significantly more negatively than the Fed’s own projection, so there is a chance we see a modest USD rally,” says Beauchamp.

Latest Pound / US Dollar Exchange Rates

| Live: 1.3473▼ -0.25%12 Month Best:1.3867 |

*Your Bank's Retail Rate

| 1.3015 - 1.3069 |

**Independent Specialist | 1.3284 - 1.3338 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

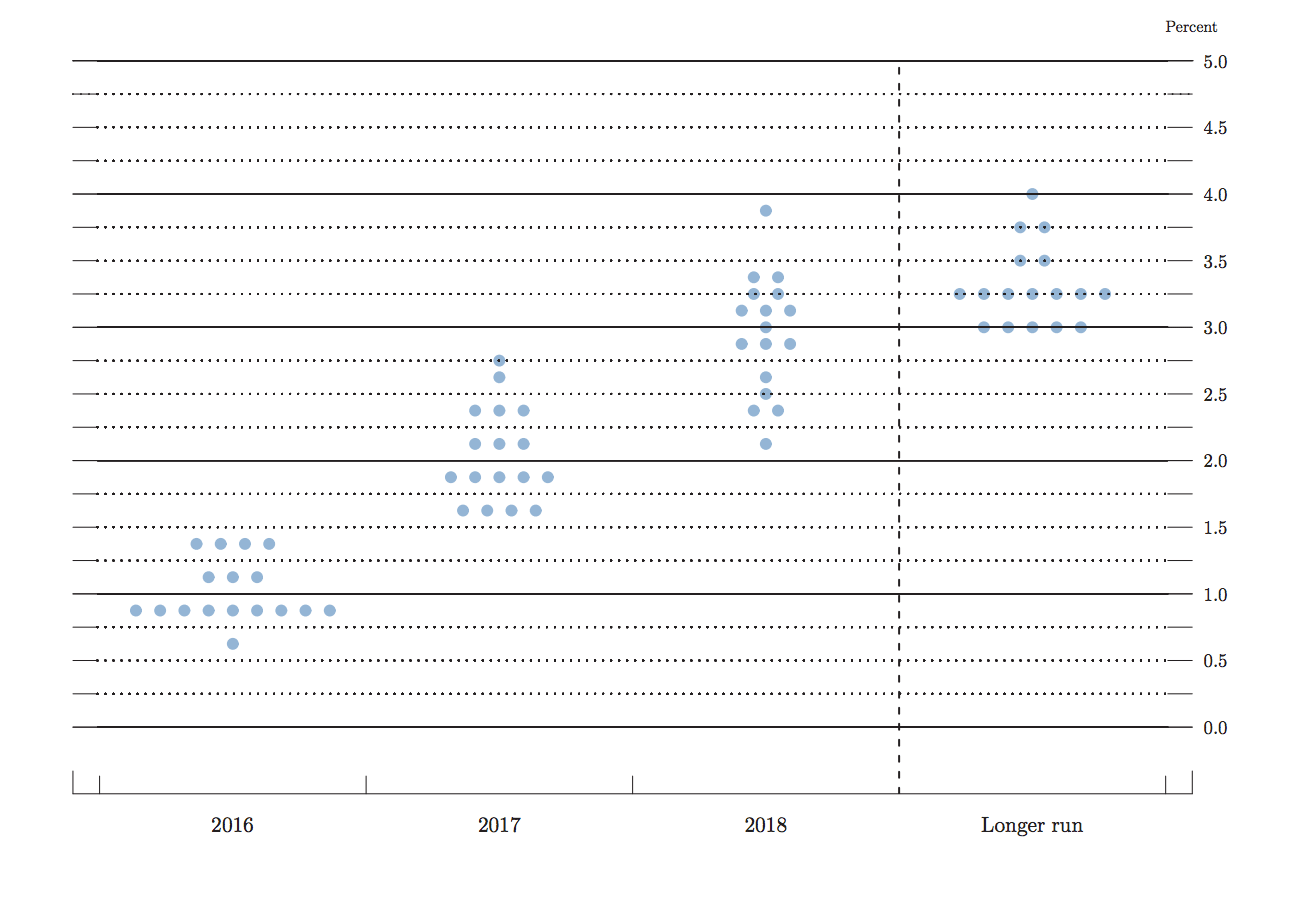

Movement in the Dots Could be Where all the Action is

The Federal Open Market Committee (FOMC) will update its economic and policy projections at this meeting.

The most likely change will be a modest shift lower of the dots for 2016, and probably for 2017 and 2018 as well.

The dots being referred to is a chart that shows where each participant in the meeting thinks the fed funds rate should be at the end of the year - for the next few years and in the longer run.

Take a look at the March meeting’s dot plot chart:

As we can see, the majority of members see it appropriate that the Fed has a base rate of 0.75% by year-end.

“With a majority of 9 among 17 members calling for 2 hikes in 2016 it seems unlikely the median will shift in the 2016 dots. This group would need to move almost en masse to force that median down to 1 hike,” says a briefing from Westpac Institutional Bank in Sydney. “The distribution of dots around that median should take on a dovish bias though, certainly the 7 calling for 3 to 4 hikes this year could see some trimming, if only because there is one less meeting this year.”

The long term neutral rate (3.25%) probably comes down another 25bp, as it has done so at virtually every dot plot refresh in recent years. “All told hardly a USD bullish backdrop,” say Westpac.

Westpac have told clients this week that they see it appropriate to be long on the euro / dollar exchange rate as a result.

Westpac have told clients this week that they see it appropriate to be long on the euro / dollar exchange rate as a result.

Bank of America Merrill Lynch’s Michael S. Hanson agrees that the most likely change will be a modest shift lower of the dots for 2016, and probably for 2017 and 2018 as well.

However, “the median number of hikes is likely to remain at two for 2016, while we see a relatively low probability that the median number of hikes for 2017 or 2018 will decline to three from four: for 2017, that would require all five Fed officials currently signalling four hikes to switch to three,” says Hanson.

In the statement, the FOMC is expected to acknowledge that the employment situation has softened recently, hardly surprising in light of this month’s poor payroll report.

Nevertheless, some expect this negative to be offset by suggestions that the US has reached full employment and by noting that current-quarter GDP growth is expected to be stronger.

Bank of America believe it is also unlikely that the Committee will provide any indication of policy action at subsequent meetings beyond the standard language in the statement; any such hints would be seen as hawkish by the markets and could well boost the US dollar.

Too Soon to Sound the Alarm say Goldman Sachs

Striking a more optimistic tone are Goldman Sachs, where analysts argue, "it is much too soon to sound the alarm," following the poor employment report.

Goldmans argue that too pessimistic a tone has been struck over the report noting that adjusted for the Verizon strike, payroll employment growth was not much below our estimate of its trend or “breakeven” level.

And, "downward revisions to prior months reflected seasonal adjustment changes, so we would caution against extrapolating a trend."

Further, other labour market indicators, such as jobless claims, have held up better. "We see a slowing, not a slump, in the latest labor market data," argue Goldmans. "We expect the Fed to stand pat next week, but to keep a rate hike in the near future on the table."

Can the Dollar Recover?

The big question then is whether or not the Fed can shift the dollar’s fortunes?

Analysts are in agreement that the weak May NFP report eliminated the possibility of a June FOMC hike, particularly ahead of a still close EU Referendum in the UK (according to opinion polls).

“The FOMC statement and Janet Yellen's press conference will still rock the dollar because investors are on the fence about the timing of the next rate hike,” says Kathy Lien, an Director with BK Asset Management.

Lien says if Yellen refrains from saying that rates could rise in the coming months and expresses concerns about the economy, the dollar will extend its slide.

But if she is even slightly more hawkish than the market expects, the dollar will rise quickly and aggressively.

“The USD’s price action in response has been severe as it registered its largest daily change on a negative NFP surprise since 2001. Historically, these moves persist underlying our continued cautious stance,” says Bank of America Merrill Lynch’s FX Strategist Ian Gordon.

Gordon believes that with a rate move off the table, the USD will respond to any signal of action in coming meetings the FOMC gives.

Chair Yellen’s balanced tone in her recent Philadelphia speech suggests we will not see a repeat of the October 2015 statement when the FOMC specifically laid out conditions they wanted to see before raising rates at the “next meeting.”

“Such a move would be USD-supportive alongside a rise in front-end yields. However, given our expectation for the FOMC to adopt a cautious, data dependent stance, it is

unlikely the FOMC will alter the dollar’s recent fortunes, and indeed will weigh on the USD further through a continued decline in real yield differentials. Therefore, we remain biased towards further USD downside,” says Gordon.

The Dollar’s Advance is Not Yet Done: Morgan Stanley

The question of whether the dollar can advance further rests with how the Federal Reserve reads the slowdown in the US labour market argues Hans Redeker at Morgan Stanley.

Will the Fed take the view that the slowdown in hiring is because the labour market is approaching NAIRU and the decline in new-job creation will come along with rising wages?

(Non-Accelerating Inflation Rate Of Unemployment - NAIRU - is the natural state of equilibrium between the state of the economy and the labour market. If the US has achieved this then the slowdown in wages is unlikely to be of concern).

The Beige Book reporting tighter labour market conditions in 14 districts and average hourly earnings holding steady at 2.5% may be evidence of this.

“In this case, the Fed would keep its tightening bias intact, pushing the USD higher, and we would be wrong to make the above adjustments to our portfolio,” says Redeker.

But what if the US economy really is in worse shape than it appears?

“We would certainly then see the Fed maintaining its dovish tone and pushing out rate hikes even further,” says Redeker.

All in, Morgan Stanley stay firmly convinced that the USD's secular bull market is not yet complete.

“Should US wages turn higher, the USD would likely move higher later this summer. Should the US been entering a cyclical slowdown, the USD would have more short-term downside potential of around 5% from here, before EM overcapacity worries put the USD back into its bull trend,” says Redeker.