New Zealand’s BNZ have upped their forecasts for the New Zealand dollar as an RBNZ hamstrung on high interest rates will be unable to prompt the kind of weakness analysts had previously expected.

- GBP still forecast to advance against NZD through 2016 but targets downgraded but 2017 forecasts upgraded

- Australia's decision to cut interest rate heaps pressure on Governor Wheeler to cut rates more agressively

- NZD v USD to maintain higher range than previously anticipated as Fed delays interest rate rises

BNZ have upgraded their forecasts for the New Zealand dollar thereby conceding the declines they had expected to take place in 2016 will not be as severe as previously thought.

We reported earlier this month that BNZ were looking to make adjustments to their forecasts having warned that they were expecting the currency to stay ‘stronger for longer’.

The decision to revisit the NZD’s outlook centres largely on the actions of the Reserve Bank of New Zealand (RBNZ) who this month opted to keep interest rates unchanged.

This indicated to BNZ analysts that while the Bank had the chance to knock the NZD lower with another easing in policy they chose not to go after the weaker currency they aim for.

“While the RBNZ desires a weaker NZD, it is unwittingly keeping the NZD elevated by maintaining NZ’s interest rate premium to global rates,” says BNZ’s Jason Wong.

Wong seeks to lay the blame for the decision to delay at the doorstep of rising house prices.

Weaker house price inflation early in the year gave the RBNZ some confidence to surprise the market with a NZD-negative rate cut, with a seemingly renewed vigour to achieve its inflation target.

However, with the latest data showing a renewed uptick in house price inflation, the Governor wasn’t prepared to deliver another easing in policy so soon which suggests the NZ dollar can retain support.

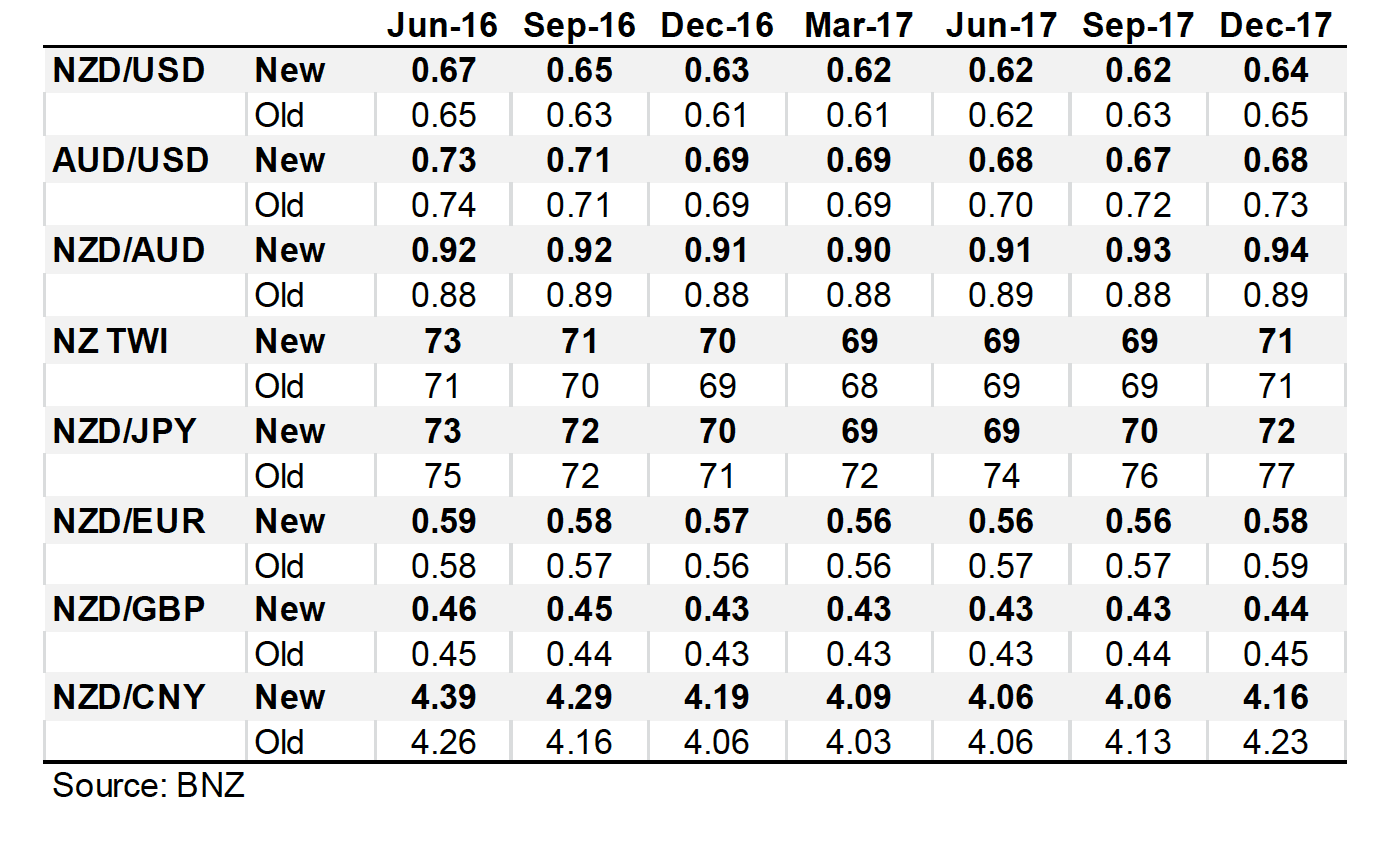

Having taken all the above into account, BNZ’s new forecast targets are now out.

The pound to New Zealand dollar exchange rate is expected to appreciate from its current levels at 2.1421 and by June GBP/NZD is forecast to trade at 2.1740.

This is a downgrade on the previously forecast 2.2222 for the same period.

The rate is forecast at 2.2222 in September, with the target lowered from 2.2727.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3518▲ + 0.14%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.2719 - 2.2813 |

**Independent Specialist | 2.3189 - 2.3283 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

By December GBP is expected to trade at 2.3256, an unchanged forecast to previous levels.

The currency pair is expected to trade at 2.3256 through the first three quarters, interestingly this is an upgrade on the previously assumed 2.2727 suggesting the New Zealand dollar could have a weak year.

By the end of 2017 the exchange rate is expected to be at 2.2727, up from 2.222.

The upgrades in the GBP to NZD conversion’s forecasts for 2017 would presumably reflect the commencement of interest rate rises at the Bank of England which will be waiting for the mid-year referendum on EU membership to pass before raising interest rates.

Until we get indications that the Bank is looking to raise rates we would imagine sterling will continue to struggle to find any meaningful degree of upside traction.

New Zealand to US Dollar Forecast: Fed-Dependent

BNZ see the NZD largely trading in a 0.65-0.70 range against the US dollar over the next few months, a higher range than previously thought.

This is largely down to the Fed and the RBNZ seemingly proceeding cautiously with rate hikes and cuts respectively.

We have reported in the past 24 hours that Lloyds Commercial Banking have cut their US dollar forecasts as they account for fewer-than-previously-expected interest rate rises at the US Fed in 2016 confirming a growing consensus around the matter.

“On NZD/USD, the expected downturn has effectively been pushed out a quarter or two. A Fed on hold has created a more positive risk appetite environment, pushed up global commodity prices and led to a recovery of Asia-Pacific currencies,” says BNZ’s Wong.

The NZD has moved in sympathy with this trans-Pacific currency play, even despite the all-important dairy price finding traction.

Recent months have also witnessed the return of the ‘carry trade’ as a more stable global financial market place has allowed investors to borrow cheap euros and dollars and invest in high yielding destinations like New Zealand where the 2.0% OCR offers decent returns.

However, the interest rate gap between the US and New Zealand is still expected to close.

“As the second half of the year gets underway, the next Fed tightening is expected to come into play, reversing those market movements – not fully, but enough to see some renewed downward pressure on the NZD,” says Wong.

BNZ’s year-end target on NZD/USD is at 0.63 having previously been set at 0.61.

Australian Rate Cut Suggest New Zealand Will Have to Cut Interest Rates More Aggressively

Previously Australia shared the burden of being the target destination of the carry trader as it too had a base interest rate at 2.0%

The recent rate cut at the RBA to 1.75% now leaves New Zealand’s 2% base rate a soft target for global investor flows.

Such flows will only keep the NZ dollar elevated at a time when the country needs a weaker currency to stimulate export growth.

The RBNZ will have to cut interest rates again in order to keep in light of moves in Australia.

“After the RBNZ’s April decision, weak Australian CPI data led to the RBA easing. This led to a stronger NZD/AUD exchange rate and adds to the chance of the RBNZ cutting the OCR by 25bps in June, which is now widely anticipated,” says Wong.

However, markets widely anticipate the RBA to cut interest rates again, noting that one Australian rate cut is typically followed by another.

Therefore, just to keep up with its neighbour and maintain the status quo the RBNZ will likely have to cut twice more in the current cycle. This could really stimulate house price inflation and shows just what a difficult task lies ahead for RBNZ’s Governor Wheeler and his team.

The RBA/RBNZ dynamic has seen BNZ scale back their forecasts for a lower NZD to AUD exchange rate.

“With RBA easing back in the spotlight and the RBNZ reasserting itself as a reluctant cutter, our

previous call that NZD/AUD could settle around the 0.88-0.89 mark for an extended period has been abandoned,” says Wong.

The downward trend in the NZ-Australia 2-year swap rate has now been arrested and is now expected to range trade through the rest of the year.

This removes one of the key downward drivers of the cross BNZ had previously expected.