The New Zealand dollar is suffering at the start of the new month, however strength should return argue BNZ who have conceded that their initial forecasts for NZD weakness made at the start of the year were overly pessimistic.

May has not gotten off to the best of starts for the New Zealand dollar with an Australian interest cut and some poor dairy price data undermining sentiment.

The Kiwi fell in sympathy with its larger trans-Tasman cousin after the Reserve Bank of Australia cut interest rates by 25 basis points sending the AUD notably lower.

Lower interest rates in Australia keep the door ajar to further rate cuts at the Reserve Bank of New Zealand (RBNZ) which should in turn diminish some of that pro-NZD investor demand for New Zealand’s high-yielding assets.

With sentiment towards the NZD already soft, news that the Global Dairy Trade Price Index fell to -1.4% from 3.8% spurred NZD selling further. "Between the RBA's decision to ease and the 1.4% drop in the Global Dairy Trade index, the pressure is on for the RBNZ to act next," says Kathy Lien, Director at BK Asset Management in New York.

The New Zealand to US dollar exchange rate (NZD-USD) extended losses to 0.6932, an eye-watering 1.24% lower than seen at the previous day’s close.

The pound to New Zealand dollar exchange rate (GBP-NZD) was seen higher at 2.0990.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3518▲ + 0.14%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.2719 - 2.2813 |

**Independent Specialist | 2.3189 - 2.3283 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Stronger for Longer

While the new month certainly has not gone the way of the NZD bulls, weakness should be viewed as temporary argue analysts at BNZ Research in Aukland.

“A ‘stronger for longer’ NZD path seems a better description of the near-term outlook for the NZD. Over coming weeks the risk is that we see more upside than downside and a weaker NZD path might be deferred until the second half of the year,” says BNZ strategist Jason Wong.

BNZ entered 2016 with a bearish stance on the Kiwi dollar and have conceded that their NZD targets against the US dollar of 0.65 for end-June and 0.61 for end-December look increasingly difficult to achieve.

Their soft stance on the NZD-USD rate has been challenged by the US Federal Reserve which stood back from looking to raise interest rates at the FOMC in March.

US interest rates staying lower for longer means global investors will likely continue borrowing US dollars and investing them in higher-yielding New Zealand assets propped up by a base rate at the RBNZ of 2.25%.

This will continue driving demand for the NZ dollar. However, a US rate rise would likely see the advantage of this investment practice wane as the cost of borrowing dollars rises.

The RBNZ added fuel to the NZD rally in late April by failing to cut interest rates ensuring the gap between US and NZ interest rates remained wide open.

“The Bank had the chance to knock the NZD lower with another easing in policy, but chose not to. While the RBNZ desires a weaker NZD, it is unwittingly keeping the NZD elevated by maintaining NZ’s interest rate premium to global rates,” says Wong.

Wong argues that the job of getting inflation back within the target range is even harder, with the TWI up over a percent and looking likely to track higher over coming weeks.

Why the Federal Reserve is so Important to the New Zealand Dollar’s Outlook

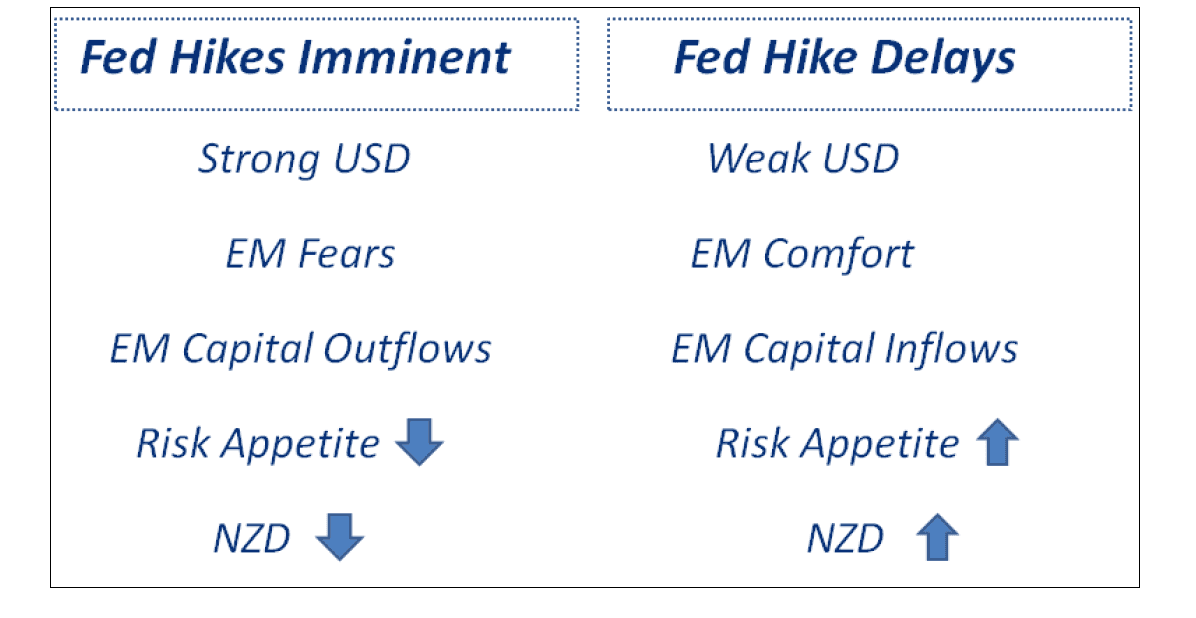

Looking at the below Wong explains how the US Fed exerts its influence on the NZD and why it is the Fed that ultimately matters for the NZD going forward:

From mid-2014 to early this year the left hand side of the chart prevailed – the USD rocketed ahead as Fed hikes became likely; this invoked fears in emerging markets exposed to trillions of dollars of USD-denominated debt, leading to significant capital outflows from that region; risk appetite fell as the strong USD effectively drove a de-facto tightening in global financial conditions; and the NZD fell significantly in that environment.

Fast forward to March this year when the Fed surprised the market by pulling back on projected rate hikes, from four hikes to two for 2016.

That led to a weaker USD, fears dissipating in emerging markets and net capital inflows returning; risk appetite perked back up and the NZD has since recovered.

In short, a requirement for the NZD to revisit the 0.65 handle is that Fed tightening becomes imminent again argues Wong.

More RBNZ Cuts Ahead

If the RBNZ opt to cut rates faster than markets are expecting then we would certainly expect the NZ dollar to find it harder to make gains.

At present markets are in agreement that the RBNZ will have to act by cutting rates again in 2016. As mentioned, the cut to Australian rates almost makes a cut in New Zealand a certainty as one rate cut of 25 basis points will merely take us back to where we were ahead of the RBA cut.

BNZ still expect a cut at the RBNZ’s June meeting, though beyond that a further cut is a line-ball call. (Note this call was made ahead of the RBA cut, we would expect the stance at BNZ to have changed as a result).

There is also the question of whether the NZD is itself to high and posing a threat to economic growth.

The RBNZ took a swing at the strengthening NZD at their April meeting saying it “remains higher than appropriate given New Zealand’s low commodity export prices.”

However it must be noted that there remain compelling reasons as to why the RBNZ will keep rates where they are - the housing market continues to heat up with regions outside of Aukland also starting to see prices rise at an uncomfortable pace.

The Bank’s low interest rate settings aren’t helping and risk making it even worse were they to be cut again.

Then there are the signs that, despite the weakness in the dairy industry, the economy is faring reasonably well, overall, and with little to no spare capacity.

All this suggests the RBNZ will unlikely be able to cut by enough to really hurt the NZD and it is hard to see anything other than the US Federal Reserve that will be able to pressure the currency.