- Quotes:

- Pound to Dollar Rate: 1 GBP = 1.3002

- Dollar to Pound Rate: 1 USD = 0.7690 GBP

The US Dollar is outperforming the Pound at the start of the new week with gains being registered against both the Euro and US Dollar.

GBP/USD continues to find selling interest above the key 1.30 level and is trying to keep in touch with this point ahead of what will be a week filled with US-orientated events.

“Although GBP remains on an appreciating trend, with market positioning and valuation providing a boost, further near-term upside will likely require a catalyst, in our view. Baring further unexpected negative political headlines from the US, we do not think this week will provide such catalyst and expect the Cable to range-trade,” says Hamis Pepper, an analyst with Barclays in London.

Traders appear to be increasingly willing to build tactical short positions on the Pound before June 8 general election.

Any decision to start selling the Pound will certainly have been helped by weekend news that the ruling Conservative party’s lead in the polls have been slashed.

Are we entering a period of uncertainty as to the outcome? Recall markets are expecting a big win for May, anything less will be met with disappointment.

"GBP/USD remains trapped in a well-defined channel, with support at 1.2880 and resistance 1.3060. Our studies still look for a top to try to develop around this 1.30 region," argues Robin Wilkin, a technical analyst with Lloyds Bank.

A decline through 1.2880 would be the first trigger to suggest further weakness is likely, with daily trend support below lying at 1.2800 argues Wilkin. "A break of these levels adds confirmation to our view".

Politics: Will Risks Fade and Help the USD?

Washington politics will likely remain a key driver of market sentiment and the Dollar this week.

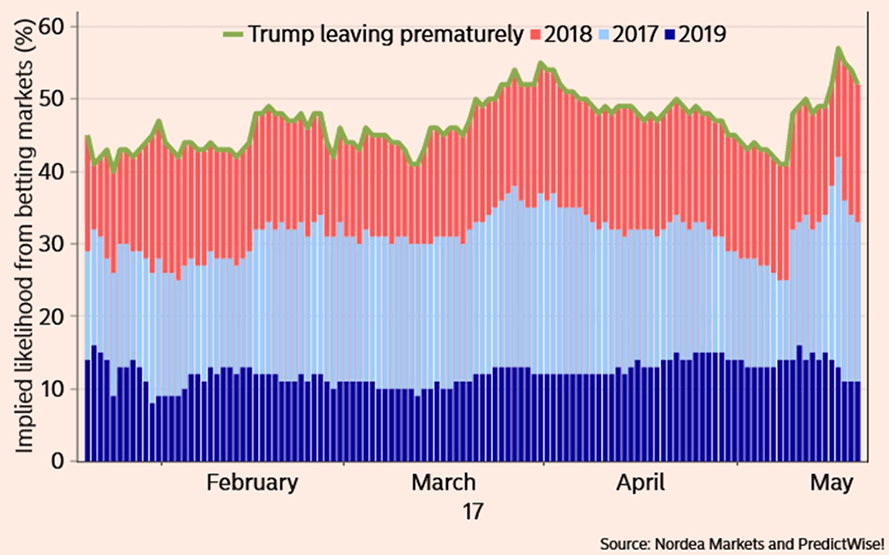

The US Dollar has suffered of late amidst a barrage of allegations relating to the Trump administration’s relationship with Russian officials.

The currency sank as expectations for a Trump impeachment grew, something that would put the pro-USD policies the President has proposed in jeopardy.

Prediction markets have however shown the chances of Trump being ousted from office in 2017 have diminished somewhat, while chances for a 2018 impeachment has risen somewhat.

The appointment of a special counsel is likely to dampen the impact on markets from further allegations, as well as postpone any negative fallout for the President.

“This shift in market pricing is rational given that a special counsel likely won’t deliver short-term. While further headline noise is likely, the effects on markets should be more muted as a result of this deferment of expectations,” says Johnny Bo Jakobsen at Nordea Markets.

Tomorrow President Trump is expected to present his full fiscal year 2018 budget proposal.

“The proposal will likely include a "massive tax cut", but no border-adjustment, and rely on optimistic growth assumptions to offset the impact on the budget deficit. In terms of US economic data, this week only brings second-tier releases,” says Jakobsen.

Federal Reserve Key

The other driver of Dollar movements over coming days will likely be the US Federal Reserve.

A number of Fed officials, including Evans, Harker, Kashkari and Kaplan, will have the opportunity to give markets an updated view on the potential for a June hike following the recent market turmoil.

Mid-week sees the release of the minutes to the May Federal Reserve Open Markets Committee meeting and traders will assess the discussion of the Fed’s balance sheet outlook.

“All eyes will be on the Fed meeting minutes, and any hint that rates may rise in June. Even a whiff of a hike could be enough to help the troubled Dollar to recover,” says Kathleen Brooks at City Index. “The Dollar, unfairly in our view, took the biggest hit from the Trump scandal, falling in line with Treasury yields. However, the 10-year yield found good support at 2.20%, so if it can capitalise on that this week and move back towards 2.30%, then the Dollar could be in with a chance of recovery.”

A hint of the Fed being more aggressive on tightening monetary policy will help yields higher, and thus potentially the Dollar too.

The Fed will release the minutes of the 3 May FOMC meeting, when the committee decided to leave rates unchanged but signalled that the outlook for gradual policy normalisation remains intact, which most likely includes another rate hike in June.

In addition, the minutes should highlight that, while the committee discussed the weaker US 1Q numbers (GDP and employment), it concluded that the underlying momentum in the economy has remained solid.

“We expect that the FOMC used the most recent meeting to discuss details about when and how to start shrinking the Fed’s large balance sheet,” says a note from the economics team at UniCredit Bank on the matter.

According to recent speeches by Fed officials, notably Vice Chair William Dudley, the Fed will “later this year or next year” begin to gradually decide to normalise its balance sheet.

“This should also be the key message from the minutes. Additional emphasis will be put on the attempt to minimise any market disruption from a balance-sheet reduction,” say UniCredit.

Analysts at DNB Markets say they believe in positive US growth effects from expansionary fiscal policy and expect a rise in US Treasury yields in 2017.

The Norwegian bank expects the Federal Reserve to hike 2+2 in 17/18, more than market is currently pricing while they also believe the Fed will signal a reduction of the balance sheet by end-of-2017.

Analysts tell clients they have lifted their EUR/USD forecast short-term due to reduced political risk in the Eurozone and increased Trump turmoil but going forward they still believe in EUR/USD at 1.02 in 12m.

This week's US data docket sees the release of another Fed survey in then form of the Richmond Fed index. Comparable indices have come in mixed.

Whereas the Empire State index clearly disappointed, the Philly Fed index surprised sharply to the upside.

“Overall, however, expectations should not be pegged too high as the Trump euphoria has fizzled out altogether with the political chaos that erupted for days last week. Data releases scheduled for later this week are likewise expected to be underwhelming,” says Ralf Umlauf at Helaba Bank in Frankfurt.