Image © Adobe Images

Pound sterling could see a relief-style rebound against the dollar in the coming days, but the building downside momentum is increasingly hard to ignore.

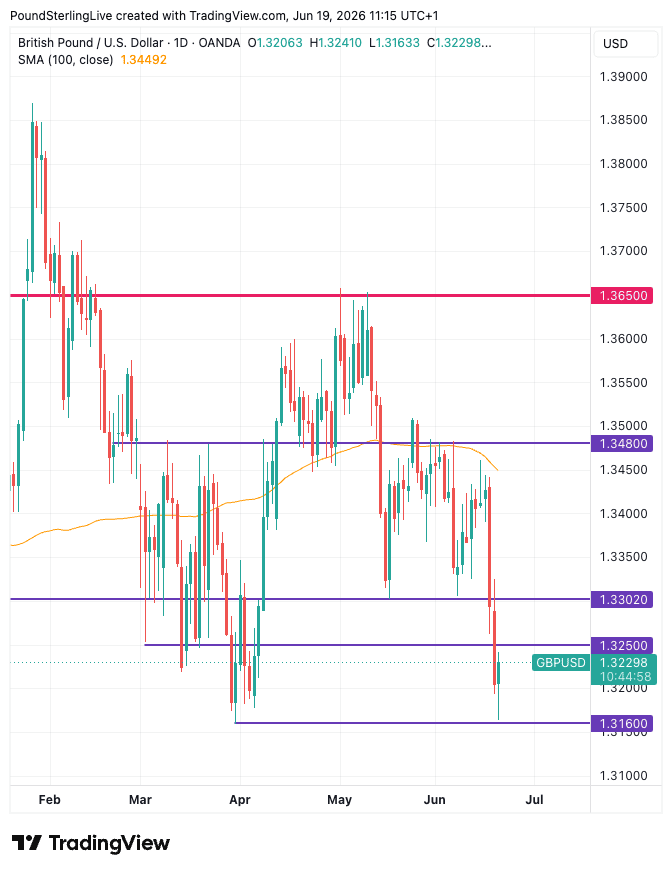

The pound-to-dollar (GBP/USD) outlook has deteriorated markedly over recent days, to the extent that a test below 1.30 looks to be increasingly likely in the coming weeks; this is thanks to a 'hawkish' shift in Federal Reserve policy and a broad underperformance by the pound.

The pound-to-dollar conversion kissed the 1.3160 support line in early Friday trade, which marked its lowest level since March 31, before it bounced off the support line and pared losses, leaving it a quarter of a per cent up on the day, albeit down 1.30% on the week.

Near-term, there's a likelihood that some mean-reversion of the hefty losses of recent days allows the pair to stabilise above 1.3160: "If a short-term rebound develops, the May trough near 1.3300 may serve as initial resistance," says a technical research analysis from Société Générale, released today. "March low of 1.3159 must hold to avoid deeper drop."

Although some gains are possible in the coming days, rallies are likely to be shallow as we look to have entered a more durable run of USD outperformance.

"GBP/USD has broken below the ascending trendline established since April 2025, extending its decline toward the March low (1.3150)," says Soc Gen. "Failure to reclaim this hurdle may lead to continuation in the decline. Next support levels are seen at the November 2025 low of 1.3065/1.3000, followed by projections around 1.2940."

Dollar Relief at Restored Fed Credibility

The dollar's fortunes look to have swung dramatically midweek when the Federal Reserve's policy decision reaffirmed the central bank will be acutely focused on bringing inflation down under the new Chairmanship of Kevin Warsh.

"The unanimous support of all 12 voting members suggests that he has succeeded in building consensus within the committee, a committee that has now become noticeably more hawkish. The magnitude of the upward shift in expected policy rates in the latest dot plot surprised markets, which now price one and a half rate hikes by year-end, up from less than one before the meeting," says a market note from J. Safra Sarasin, the Swiss bank.

Hearing that interest rate rises are likely if inflation doesn't settle was a relief to a market that was worried Warsh would engineer the Fed's reaction function to suit President Donald Trump, who chose him as Fed Chair.

The concern was that a Warsh Fed would swerve rate hikes to ensure the economy ran hot and above-target inflation rates would become entrenched.

Dollar strength therefore reflects a receding credibility deficit as much as it reflects expectations for higher rates.

"The FOMC and chair Warsh put price stability at the heart of the statement and press conference, boosting the bank’s credibility, squeezing Treasury yields at the long end of the curve... rate differentials swung the tide in favour of the dollar," says the Soc Gen note.

GBP's Hard Labour

The pound has meanwhile struggled in an environment of falling oil prices, which have lowered the chances of inflation running hot, in turn ensuring less need for the Bank of England to raise interest rates.

With rate expectations falling due to a drop in oil prices, UK short-term bond yields have declined faster than elsewhere, including in the eurozone and U.S.

That's weighing on the GBP.

Interestingly, we've seen UK bond yields outperform on Friday, and that's correlating with a recovery across the GBP strip.

That could be due to a combination of left-leaning Andy Burnham winning the Makerfield by-election and UK borrowing for May coming in well ahead of expectations.

The new PM will have to face up to the intractable reality that he won't have the money he needs to pursue his utopian socialist agenda. For markets, there's some risk there and that could weigh on sterling in the coming months.