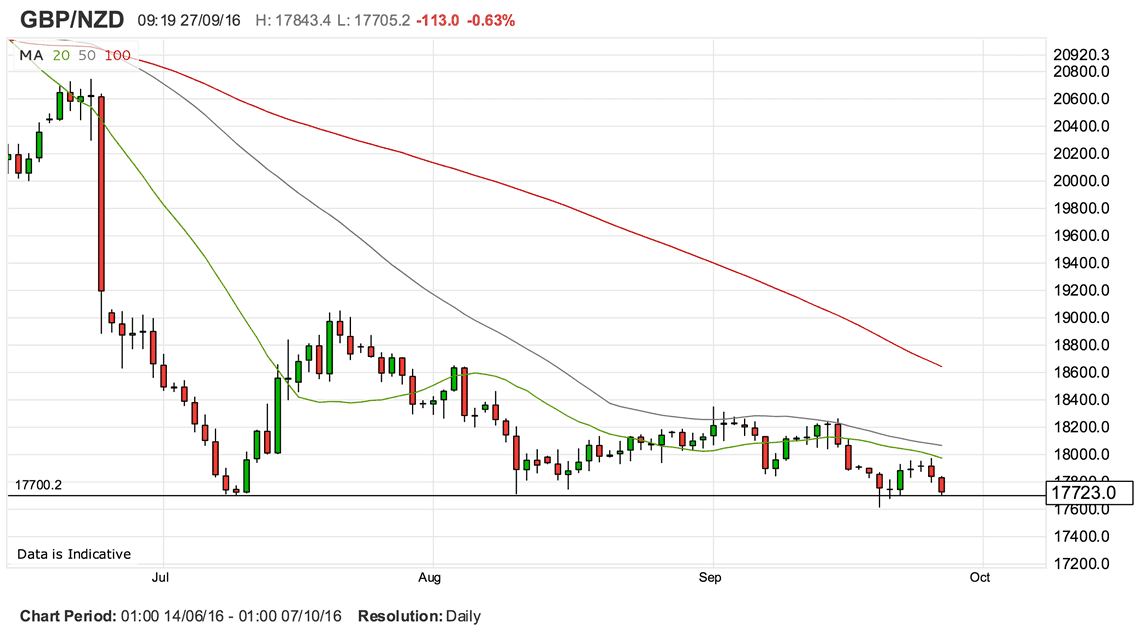

The Pound to New Zealand Dollar exchange rate is coiled to register fresh multi-year lows with charts suggesting a notable break-out is nigh.

GBP/NZD trades at 1.7730 at the time of writing, just above the 2016 support line at 1.77.

It is worth noting that the pair has not yet closed below 1.77 in 2016.

However, the inability to rally above 1.80 over recent days suggests there is simply little fuel in the Pound's tank to sustain any strength ensuring movement in the exchange rate becomes increasingly compressed:

Compression inevitably leads to explosion, and as such we are watching this pair for a notable breakout.

With momentum since June being one-directional, we would have to be overwhelmingly in favour of the move being to the downside.

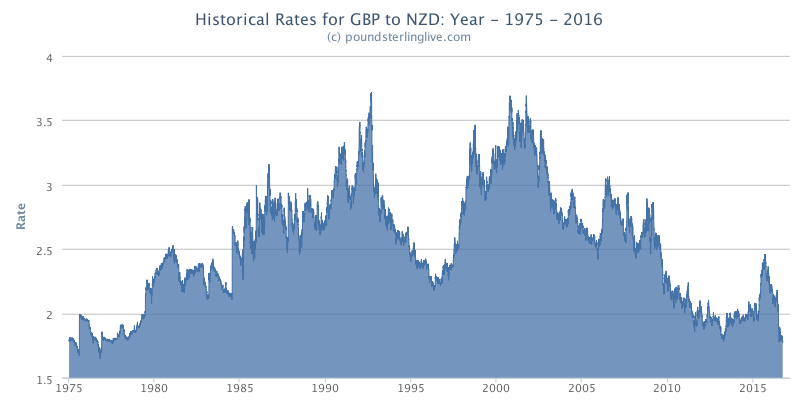

If this were to happen then the New Zealand Dollar coule be about to register its best performance against the Pound since 1976:

Next Target Could be 1.72

The NZD and GBP were the two worst-performing currencies in the G10 complex in the previous week with a long-term outperformance in the New Zealand currency finally hitting the buffers.

Whether or not this fresh NZD weakness heralds the start of a period of underperformance or a mere bout of profit-taking will be answered this week.

The Pound to New Zealand Dollar has bounced off the significant support level at 1.77 level on eight occassions since July and is yet to end a day below here.

After making a sequence of smaller recovery highs on each rejection of 1.77, it has ended up tracing out a right-angled triangle:

Once complete, right-angled triangles normally break below the flat edge, which in this case means a break down, below the 1.75 level.

Such a break, confirmed by a move below 1.75 would probably run to support at 1.7200, initially from the S2 monthly pivot, a level of support and resistance, traders use to gauge the trend and launch counter trend trades.

The triangle is almost complete as it rises and finishes wave ‘e’, since these patterns normally contain a minimum of five waves.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3521▼ -0.03%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.2721 - 2.2815 |

**Independent Specialist | 2.3192 - 2.3286 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Fundamentals Continue to Support NZD

As mentioned, both the NZD and GBP underperformed their peers last week so a break to fresh lows in GBP/NZD is by no means a given.

Nevertheless, the New Zealand dollar continues to have an advantage over the pound because of its much higher, 2.0% interest rate which attracts a lot of foreign capital inflows.

Returns of 2.0% plus are much more favourable to the UK’s 0.25% base rate.

However, the kiwi is also faced with the threat of action from the Reserve Bank of New Zealand (RBNZ).

At their last meeting they warned they may act to bring interest rates down in order to weaken the kiwi, so as to encourage a rise in inflation.

“The RBNZ left rates on hold but cited concern for the high flying Kiwi, while highlighting subdued inflation and the need for more rate cuts. And so, it’s no surprise to see Kiwi lagging in Thursday trade as the market looks to reposition and rotate away from long Kiwi exposure,” say LMAX Exchange, summarising the significance and impact of the meeting.

For the kiwi, the part of the statement of most importance was that stating that a decline in the exchange rate, “is what is needed.”

Given the main reason the kiwi’s strength is foreign capital inflows attracted by the country’s relatively high 2.0% interest rates, the way to curb the kiwi would be to reduce the interest rate.

“Our current projections and assumptions indicate that further policy easing will be required to ensure that future inflation settles near the middle of the target range,” said the RBNZ, signalling an imminent cut is on the cards.

However, the RBNZ is also faced with the risk from an overheating housing market, and although policies aimed at making mortgage borrowing more difficult have cooled the market down, it remains a financial risk.

This might prevent the RBNZ from cutting base lending rates as such a cut would only exacerbate the housing boom by making it cheaper to get a mortgage.

A supportive factor for the kiwi going forward are the recent recovery in Dairy prices, the country’s main export.

“The New Zealand dollar traded lower after the Global Dairy Trade auction results. We were surprised by the reaction but the increase marked the fifth consecutive rise in GDT prices. Admittedly, the 1.7% increase was a stark drop when compared to last month’s 7.7% rise, but the fact that dairy prices have been continually increasing is a good sign for the RBNZ,” comments BK Asset Management’s Kathy Lien .

Citbank put the chances of an RBNZ interest rate cut in November at 60%.

Interestingly they saw the statement as expressing a more neutral stance from the central bank, saying, “the overall tone of the statement suggests the risks are more weighted towards a neutral stance and against a backdrop of limited USD volatility supportive of the 'carry theme', NZDUSD dips are likely to be bought with the 0.7250 support area looking to hold.”

For sterling, the currency does seem to continue to gain support from economic data which suggests the economy is holding up remarkably well after the referendum, but this is offset by weakness from uncertainty over what sort of a Brexit deal the government negotiates with the EU.

UK Chancellor Hammond has indicated the UK may leave the common market, which would be expected to impact negatively on trade and would have a detrimental short-term impact on the pound.

The threat of a ‘hard’ Brexit will probably cap sterling until dismissed.

NZ Exports Slip, UK GDP is Next Major Data Release on the Agenda

The main data release for the New Zealand dollar this week was the Trade Balance data released on Monday the 26th of September.

The trade deficit rose to 3.1BN, worse than the 2.7BN markets were forecasting.

Statistics New Zealand reported a fall in milk powder to a seven-year low saw exports fall 8.7% overall in August 2016.

This is significant in that a currency would typically expect to weaken on falling exports. While the NZD can rely on strong investor inflows owing to the high basic interest rate at the RBNZ, we would suggest this is a potential crack in the NZD's support.

For the pound, Friday September 30 sees the release of the most significant statistic for the pound, this week, in the form of the first revision of second quarter GDP.

The preliminary result already released, surprised to the upside, coming out at 2.2% rather than the 2.0% forecast, but on Friday we shall see if that upbeat result holds.

Although it does not cover much of the period after Brexit, and is therefore not representative of the impact of the referendum, it still reflects the high degree of uncertainty prevalent in the run up to the vote, and so is some sort of barometer for how the economy coped under uncertain conditions.

Second-quarter Business Investment is also out on Friday and will also be closely watched by analysts trying to make sense of how well the economy has managed with the uncertainty stemming from the referendum – again in the run up to the vote in this case rather than afterwards.

Common sense dictates that Business Investment would fall in the run up to the referendum as many businesses would have delayed investment decisions on major projects until after the vote, however, Friday’s data will tell for sure.

There is a possibility of a surprise to the upside since data has up until now, more often than not, beaten expectations which were tilted to the downside for the referendum period.