The NZ dollar is the under-performer on Tuesday as domestic data opens the door to further Reserve Bank of New Zealand easing.

Three data points have gone against the New Zealand dollar today: The diary auction, inflation numbers and retail sales.

Firstly, Reserve Bank of New Zealand (RBNZ) inflation expectations fell to their lowest levels since 1994 having read at 1.63%, down from 1.85%. The RBNZ has a mandate to keep inflation within the 1-3% range.

The trajectory in prices is clearly lower and bets on another interest rate cut at the RBNZ have risen as a result - interest rate cuts decrease New Zealand's yield advantage, therefore demand for the NZD falls accordingly.

The pound to New Zealand dollar rose notably higher having reached 2.1875 while the NZD to USD exchange rate is sharply lower at 0.6569.

Secondly, news that retail sales volumes grew by 1.2% quarter on quarter in Q4, weaker than the market’s expectations of 1.5%.

Thirdly, the most recent Fonterra dairy auction saw prices fall 2.8%, this is the fourth auction in a row where declining prices have been recorded. Dairy exports are a key foreign exchange earner for New Zealand and the impact on NZD of the continued downturn is understandable.

"Over the coming few months we expect low interest rates, strong migration and strong tourist inflows will continue to provide support to spending. However, uncertainty around the dairy outlook may dampen confidence, and limit sales growth," says Kim Mundy, Economist at ASB.

ASB join Westpac Bank in forecasting a June interest rate cut at the RBNZ.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3402▲ + 0.19%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.2606 - 2.2699 |

**Independent Specialist | 2.3074 - 2.3167 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Westpac Forecasts Warned these Declines Were Coming

The New Zealand dollar has been an outperformer of late, dodging negative market conditions, to register strong gains on a combination of strong domestic labour market data and an across-the-board rout of the US dollar.

However, Westpac’s custom foreign exchange forecasting suite suggested before the week event got under way that that the outlook is cooling on the New Zealand dollar following a strong performance this February.

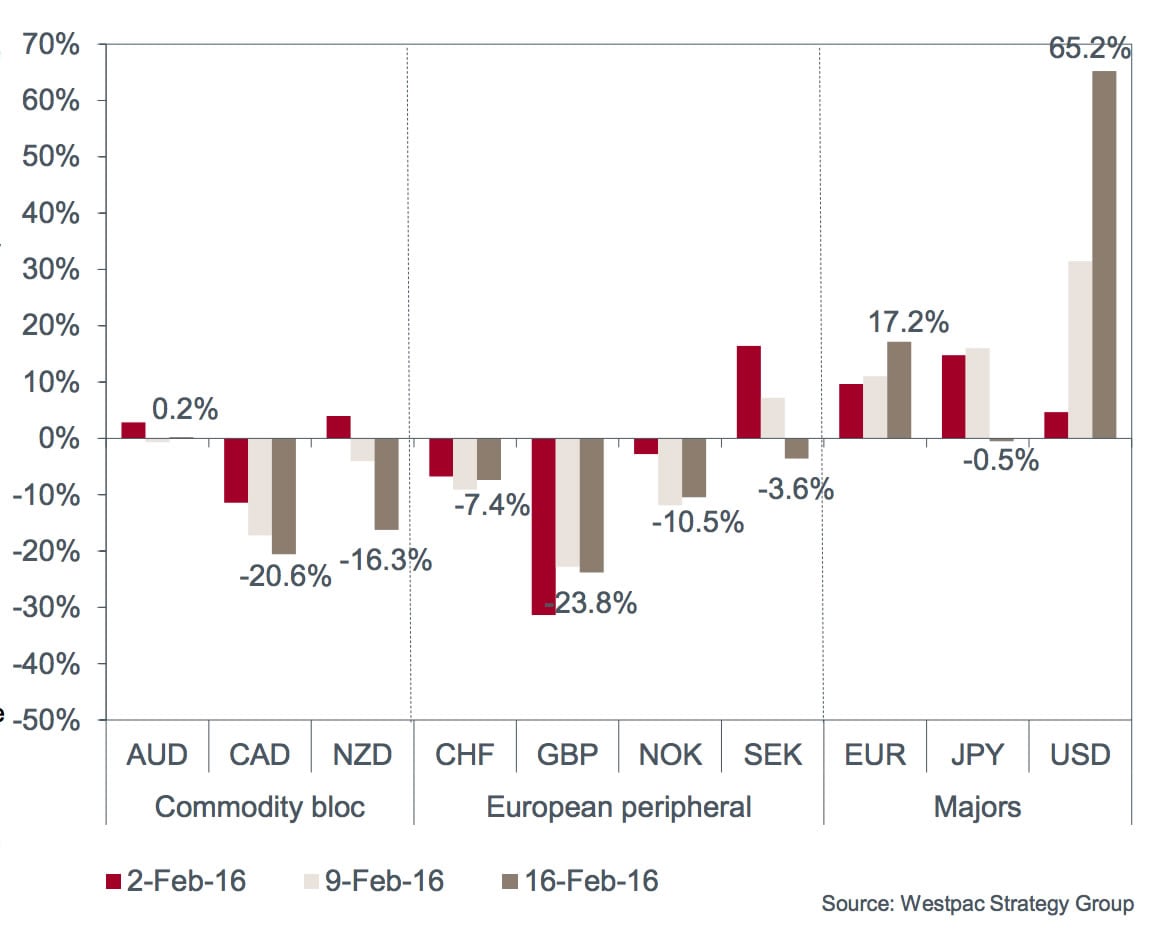

Westpac's G10 model, which uses a combination of 9 forecasting variables, has cooled on the NZ Dollar and recommends selling the currency in the week ahead.

This is the first time the model has had a decent NZD short in many months.

“Despite some more constructive risk appetite signals the narrowing in 10yr NZD v G3 bond spreads is the more important signal for the model,” says Richard Franulovich at Westpac.

Elsewhere the model sees little to do in AUD, a stronger growth signal but still poor long term valuation leaving the model neutral.

Westpac’s model remains long on EUR another week too, however it is against the US dollar where the potential for gains exist.

“A bullish US data surprise index signal remains the feature theme for the G10 FX model portfolio. The signal remains live for another two weeks, betting on yet further improvement in the complexion of the US data,” says Franulovich.

A slightly firmer total yield signal for the USD adds to the model's strong predilection for USDs.

For the week ahead the model has an over the top 65% long USD exposure, almost double last week's long USD position.

New Zealand Dollar Bullish Against Sterling

Looking at the pound to New Zealand dollar exchange rate (GBP/NZD) we note that further declines are likely from the present spot level of 2.1707.

Sterling remains trapped in a downward move, in place since late November. The declines have however subsided having met the 2.16 support zone.

The strength of this support line has held through 2016 and has allowed the price to converge with the 20 and 50 day moving averages.

The 20 day moving average is at 2.1914 while the 50 day moving average is at 2.1949.

Thus, it won't take much to break above these important technical levels; a bullish signal that more sustainable strength is returning.

That said, a fall below support at 2.16 would open the door to declines towards the magical 2.0 where rest-assured heavy buying interest will lie.

Why the New Zealand Dollar has been Stronger

The resilience of the NZ dollar of late - in the face of global market turmoil to boot - has impressed many in the foreign exchange community.

“Typically it would fall on global credit and equity unease. For sure, USD weakness is adding buoyancy to

the NZD. But the resilient NZD is symptomatic of a nation that, while not without its challenges, is wearing one of the cleanest of the dirty shirts,” say ANZ.

Why is New Zealand in a better position now than it was say in 2011 when we last saw negative market conditions, as we are presently witnessing?

A couple of pointers:

The New Zealand current account deficit is smaller. In 2008, the deficit was 8% of GDP. It is now at 3.3%, and actually below its historical average.

The national balance sheet is stronger. Net external debt, at 56% of GDP, is the lowest in 12 years and down from 85% in 2008.

Roll-over risk has reduced. The country’s international debt liabilities maturing in less than 90 days has fallen from half of the total in 2008, to less than a quarter now. That buys time.

Domestic economic momentum is still strong.

“Now that could change quickly, if the signal provided by the tightening seen in financial conditions is anything to go by. But to date, the economy has reasonable momentum, as shown by the latest activity data. Momentum is important; many forget that the economy was already in recession before the GFC actually hit,” say ANZ.

Lingering Concerns Remain

There is always a but, and this is where the NZ dollar story could potentially unravel.

“New Zealand’s balance sheet metrics are better than pre-2008, but still not strong, and they have shown signs of deterioration recently: household saving is slipping, and leverage is rising,” say ANZ.

Furthermore analysts argue that commodity dependency is still high, and dairy price action is poor amidst high leverage in the sector.

Housing is showing bubble-like characteristics in Auckland. We are linked into China both directly and indirectly (via Australia).

“The balance of power globally is shifting back to the savers; New Zealand is a net borrower. So we can’t simply blow off the potential flow through,” say ANZ.

So while the justification for the recent New Zealand dollar outperformance exists, there remain lingering concerns.

That said, the tone towards the currency is certainly fundamentally more constructive than at the same time last year.

Inflation Data, Dairy Auction Ahead

A couple of pit-falls for the Kiwi lie ahead this week.

On Tuesday, lower petrol prices may see the two-year ahead measure of inflation expectations (from the RBNZ’s survey) ease further.

In Q4, the two-year measure dipped to 1.85% from 1.94%, although this is still consistent with the inflation target midpoint.

"Admittedly, we have our misgivings about this survey (and focusing solely on any single particular measure of inflation expectations, for that matter) given its small sample size. Nevertheless, a further dip in expectations at a time when headline inflation is already low reinforces the risk around the OCRn profile," say ANZ.

Also on Tuesday another fall in prices looks likely at the next GlobalDairyTrade auction. Short-term dairy market dynamics are very challenging.

The issue is too much supply, which is partly seasonal, but also linked to structural shifts in the form of increased European supply from efficient producing regions and a lowern cost of production (i.e. feed, energy and capital).