The GBP to USD conversion remains in recovery mode and we could see gains extend through February owing to a growing negative sentiment on the US dollar. However, global stock markets look shaky and this could undermine the UK unit.

Recent price action has left the GBP/USD looking notably more constructive with Fed Chair Yellen providing little support to the Greenback in her testimony to US lawmakers.

While Yellen did not say anything to accelerate dollar selling in her appearance before congress on Wednesday she did not say anything supportive of the currency either. In short, recent foreign exchange trends are expected to continue.

Indeed, the engine to the gains in GBP/USD is the weakening US dollar, a theme that we are becoming more familiar with.

We have reported that JP Morgan are warning of a 8% slump in the dollar index should the US Federal Reserve step back from raising interest rates again.

Danske Bank meanwhile tell us that the euro to dollar conversion should be as high as 1.24 - 1.28 according to their models.

And all this confirms that the team at HSBC were right back in 2015; we reported their predictions for a lower USD in 2016 as being an outside view.

Latest Pound / US Dollar Exchange Rates

| Live: 1.3198▲ + 0.05%12 Month Best:1.3867 |

*Your Bank's Retail Rate

| 1.2749 - 1.2802 |

**Independent Specialist | 1.3013 - 1.3066 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Perhaps the loudest cheerleaders of the US dollar in 2016 were Goldman Sachs. But, the most read story on Bloomberg over the last 8 hours is the news that Goldman Sachs has ditched five of the top six trades for 2016.

These trades were largely based on the assumption that we would see US dollar strength in 2016.

"The fact that long USD vs JPY and EUR, or long US 10-year breakevens, have been axed is a cue for much chortling in some quarters but just confirms that writing ‘year-ahead’ trade ideas in December is fraught with danger," says Kit Juckes at Societe Generale.

Sterling is looking handy mid-week as Janet Yellen tells Congress that her team are growing ever more cautious on the outlook for the US economy.

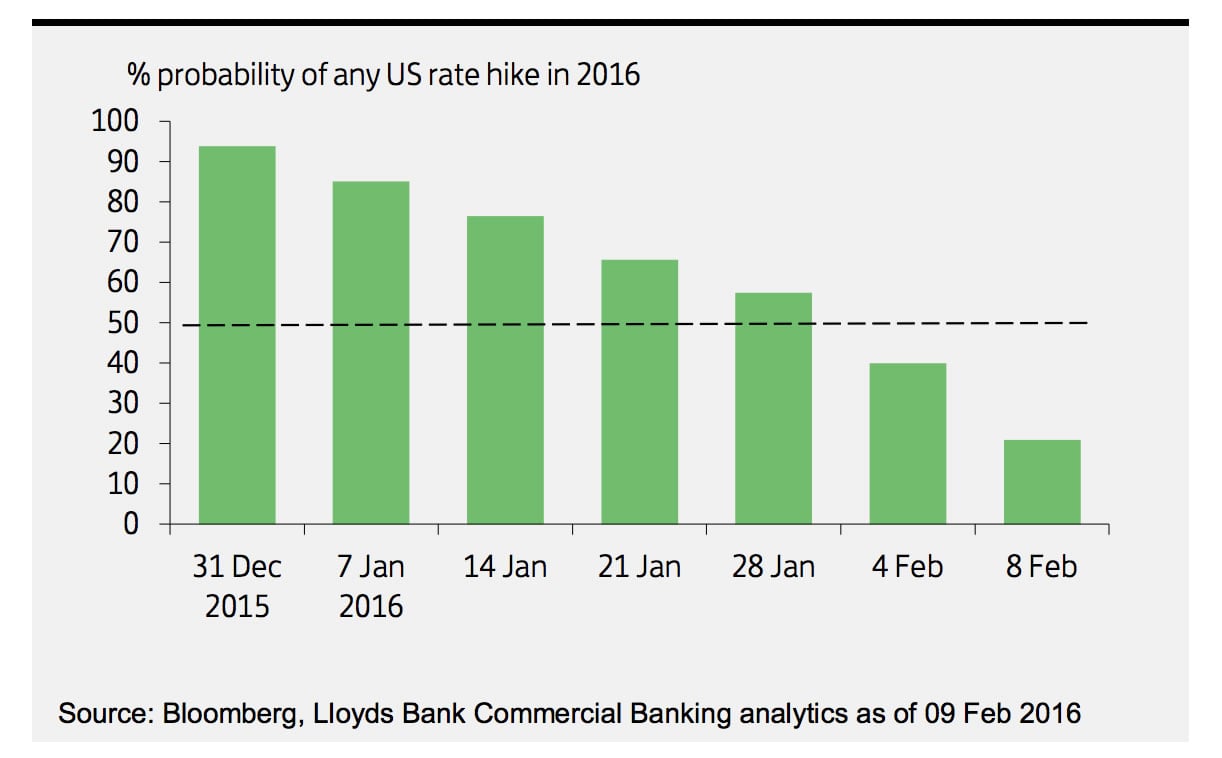

Indeed, this shift in interest rate expectations is all you need to know about the US dollar’s turn in fortunes:

“We expect bearish GBP against EUR but bullish against USD on the back of USD weakness,” say Hong Leong.

As always in a market there will be opposing views. The Investec Economics team for instance believe the Fed will raise interest rates at a steady pace, by 75bp this year taking the Federal Funds Target range up to 1.00-1.25%.

This is faster than financial markets are currently pricing.

Technically Speaking, the Pound Could be About to Head Higher Against the US Dollar

The GBP to USD daily chart is interesting, take a look at the below:

The pound appears to have bounced off the area that denotes the lower bound of the longer-term trend.

I had drawn this line back in 2015 and should the GBPUSD stay above here then the channel will remain valid, in my opinion.

Of course this only suggests that the move lower is falling back into an historical trajectory and more losses can therefore be expected.

This does however leave the prospect of a stronger February alive with a target at 1.46 being live.

Should the 1.46 region be broken then we will grow more confident in saying the pound to dollar exchange rate has bottomed out.

Why the US Fed is Changing Direction

The dollar is essentially a play on US interes rate policy where higher rate expectations support a higher currency. Lower rates and quantitative easing encourage a lower dollar.

Here is an interesting thought, could the US Federal Reserve actually embark on quantitative easing again? (Thanks to Demitri Theodosiou at Investec for the following pointers).

Ray Dalio, founder of Bridgewater, which manages $154 billion in global investments, last year famously stated that although the Fed may raise interest rates one or two times, he believes they will need to reverse course and embark on a fourth round of QE as their economy ends a ‘Super cycle’.

Larry Summers, a previous US Treasury Secretary and current Harvard professor seemed to agree, with similar calls that renewed QE will be needed.

IMF Chief Christine Lagarde last September warned the Fed against raising interest rates prematurely, not only because the American economy isn’t ready, but also because of the global implications.

Economist Carmen Reinhart penned a Dec 31 opinion piece asking the question, will 2016 be a year of sovereign defaults?

Reinhart concluded that “from a historical perspective, the emerging economies seem to be headed toward a major crisis. Of course, they may prove more resilient than their predecessors. But we shouldn’t count on it.”

George Soros, who needs no introduction, said he sees a crisis unfolding in global markets that echoes 2008 as the developing world finds it difficult to return to positive interest rates.

With China struggling to find a new growth model, its currency devaluation is transferring problems to the rest of the world.

The worst-case scenarios mentioned above appear to be playing out and we are therefore now more open to the suggestions made by these leading thinkers than we were at the start of the year.

Yellen Shows a Steady Hand

Fed Chair Yellens’s keenly awaited semi-annual testimony to Congress will be watched closely by markets today to guage whether the US central bank intends to raise interest rates again in the near future.

Yellen in her initial testimony takes a balanced position. She has acknowledged that recent economic data has been mixed and that recent market turmoil might impede economic growth.

However, while recognising the potential downside risks to economic growth she has also restated a belief that the most likely outcome is that US economic conditions continue to improve and that interest rates rise gradually.

She doesn’t give any timeframe for any further interest rates moves the but implication seems to be that while a March interest rate hike now looks highly unlikely rises from the June meeting onward remain possible.