Image © Adobe Stock

GBP/NZD set for a pullback, but it's too soon to expect a meaningful decline.

The New Zealand dollar starts the new week in strong fashion and is a leader in the G10 currency bloc on reports Strait of Hormuz will be reopened this week, a welcome development for eastern energy importers like New Zealand.

New Zealand sources the lion's share of its energy imports from Asian refiners, who in turn are overwhelmingly reliant on Middle East crude, underscoring why the blockade of the Strait was particularly troublesome.

It is reported that the Strait will be reopened immediately once a Memorandum of Understanding on a new peace framework is signed later in the week.

The Kiwi's high beta to the positive headlines sets the pound-to-New Zealand dollar exchange rate on a softer course on a near-term timeframe, with a pullback from 2.2984 to 2.2838 being our expectation for the coming week.

Short-term Pullback Possible

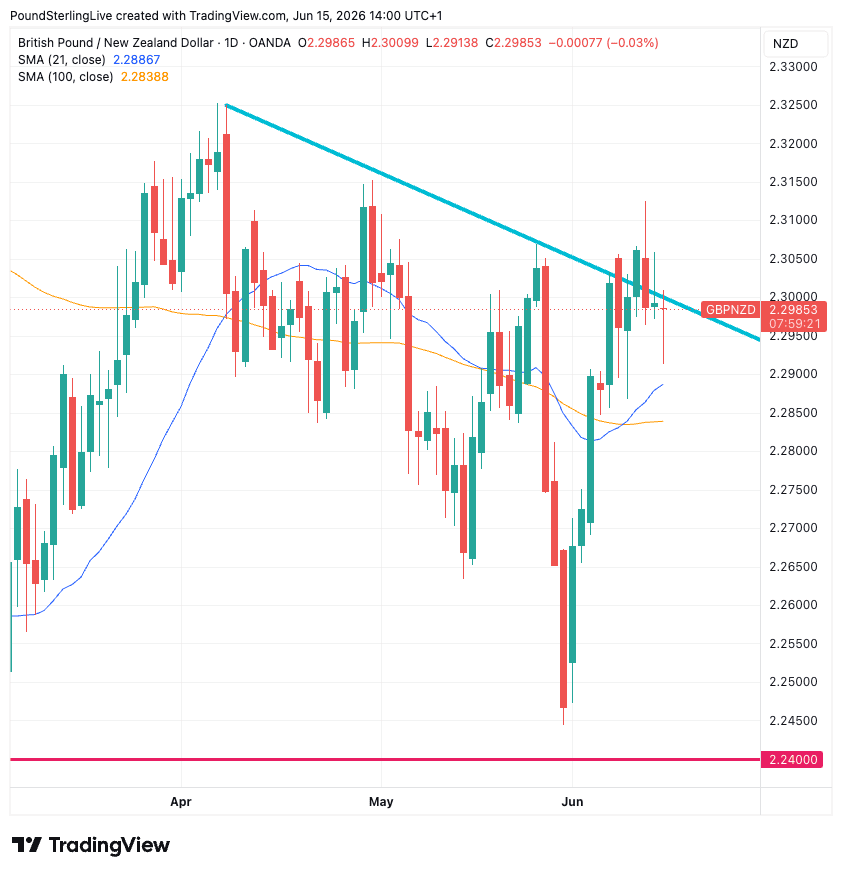

As the chart shows, GBP/NZD had recovered strongly from the sharp rejection of the 2.2400 support zone earlier this month, reclaiming both its 21-day and 100-day moving averages and restoring a more constructive short-term outlook.

The recovery has been sufficiently strong to reverse much of the May decline, suggesting buyers remain willing to accumulate sterling on weakness.

However, the key feature of the chart is the descending trendline, which is currently passing through the 2.2950-2.3000 region.

The pair is now trading directly against that barrier and has already encountered selling pressure on multiple occasions nearby.

This makes the trendline the defining level for the week ahead: a convincing break above it would signal the corrective downtrend from April is ending and would likely trigger a move towards the April highs around 2.3200-2.3250.

However, a failure here would encourage our view that a pullback is liable over the coming days.

But Still Constructive Multi-week

The 21-day moving average has crossed above the 100-day moving average, and while both are flattening out, the price is holding above them. This suggests momentum has shifted back in favour of sterling, although the market still requires a trendline breakout to fully confirm the bullish turn.

Tactically, the pullback we expect this week could extend to 2.2838, the 100-day moving average. While above here, GBP remains supported and the recovery can continue, but should a break eventually occur, then the coming months could see GBP/NZD target the year's lows at 2.24.

GDP Can Underpin Hawkish Rate Expectations

The headline calendar event for the coming week is New Zealand's GDP release, due Thursday, where it is expected to be revealed that the economy grew a healthy 1.0% in the first quarter.

Sure, the data is dated, but given it's the only major data release ahead of the RBNZ's policy review on 8 July, any surprises could impact interest rate expectations and the currency.

"Interest rate markets are already 90% priced for an OCR hike in July, the risks around the GDP release may be skewed to the downside – a weaker than expected result could cast some doubt on whether the RBNZ would move that soon, rather than waiting for the flood of inflation-related data that will come between the July and September reviews," says Michael Gordon, Senior Economist at Westpac.

There was more timely data out Monday as it was revealed New Zealand's retail spending rebounded in May, rising by 1.7%, more than reversing last month’s fall.

Helping to support May’s lift in spending was the 4% fall in fuel prices over the month, with spending up in all other categories, indicating the supportive dynamics the Iran-U.S. peace deal offers to NZ activity.

Consumer resilience can underpin the odds of a July rate hike, which will in turn underpin the Kiwi dollar.