Image © Adobe Images

Our euro-dollar week ahead forecast looks for strength to remain nothing more than corrective in nature.

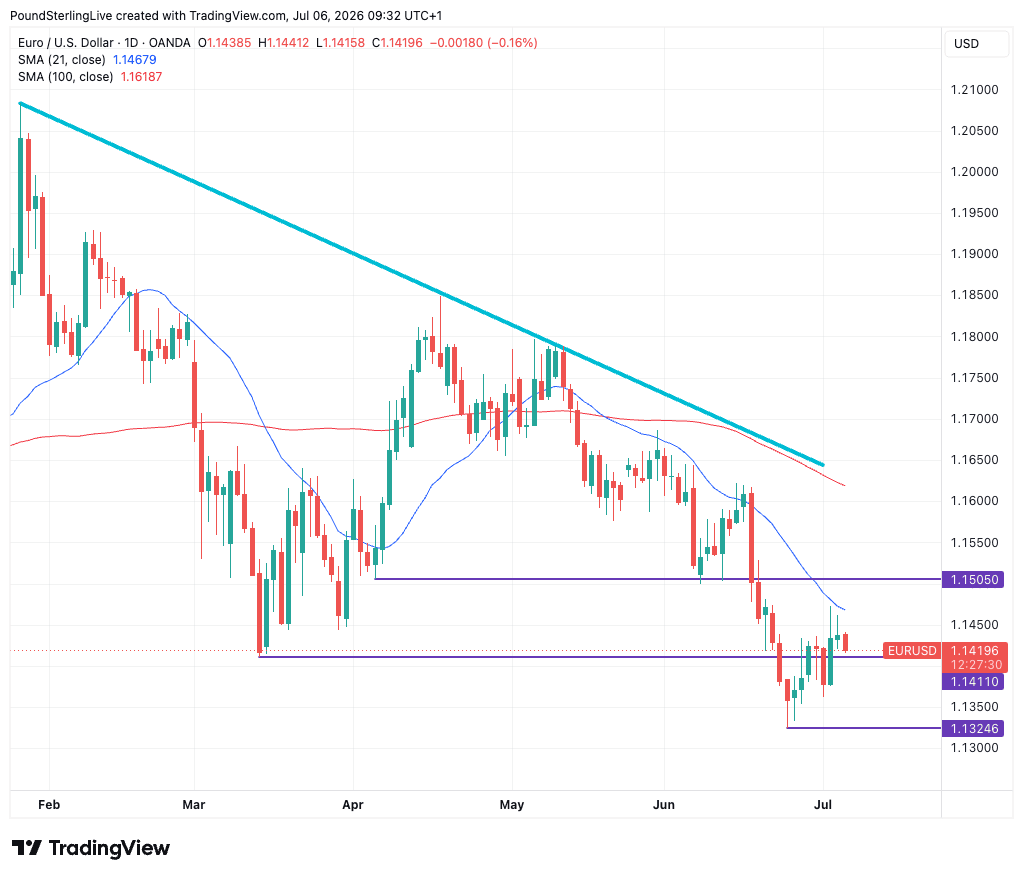

Big picture, the euro-to-dollar exchange rate remains in a well-defined downtrend, but the immediate term is defined by a stabilisation above the 1.1325 June low.

The question for the coming week is whether that overarching selloff resumes or the near-term recovery can build a bit of confidence.

The pair opened Monday at 1.1438 and trades and has softened by the time of writing to 1.1418, which is probably not something the euro bulls would have hoped for.

In fact, a look at the daily chart hints that maybe they saw the 21-day moving average just above and sold some exposure.

The chart certainly does hint at the 21-day being a significant source of resistance going back to mid-May.

That confirms the sellers remain in charge; while below the 21-day further softness is likely, and a retest of the June low at 1.1324 is the obvious prospective target for July.

The longer-term descending trendline from the January highs remains firmly intact, and although the sharp sell-off has eased in intensity, there is still little technical evidence that a more durable recovery is underway.

The key question for the week ahead is whether EUR/USD can build on its recent base above 1.1411.

A recovery through the 21-day moving average would be the first indication that bearish momentum is fading, but the broader trend remains negative while price stays below the 100-day moving average and the long-term trendline.

Until then, rallies are likely to be viewed as corrective rather than the beginning of a sustained reversal.

Some Early Good News from the Eurozone

Looking at the calendar, there's some constructive data out of the Eurozone this morning. Eurozone investor confidence improved sharply in July, with the Sentix Investor Confidence Index rising from -13.4 to -3.1.

That makes for a third consecutive monthly gain, and what's more, the improvement was broad-based, with the Current Situation Index climbing from -20.0 to -14.8.

The Expectations Index jumped from -6.5 to 9.3, returning to positive territory as optimism over the region’s economic outlook continued to build.

That's constructive, but is probably not enough to turn Eurozone bond yields (the interest rates governments pay on their debt) to rise meaningfully.

That's because the market appears to have made up its mind that there's a shrinking chance of another rate cut at the ECB during the remainder of 2026.

ECB Rate Hike Bets Fade

Eurozone bond yields have slid lately after a series of below-expectation data releases, including last week's Eurozone inflation data, which suggested the ECB might have been too pessimistic in its inflation predictions.

The inflationary shock caused by the Iran war looks set to be less severe than thought and June's precautionary rate hike, in response to those fears, might prove to be a one-off as a result.

As markets price out an additional hike, short-dated bond yields fall. When they fall faster in the Eurozone than elsewhere, the euro would be expected to underperform.

The Coming Week for the Dollar

The dollar is likely to be the main driver of euro-dollar performance once more.

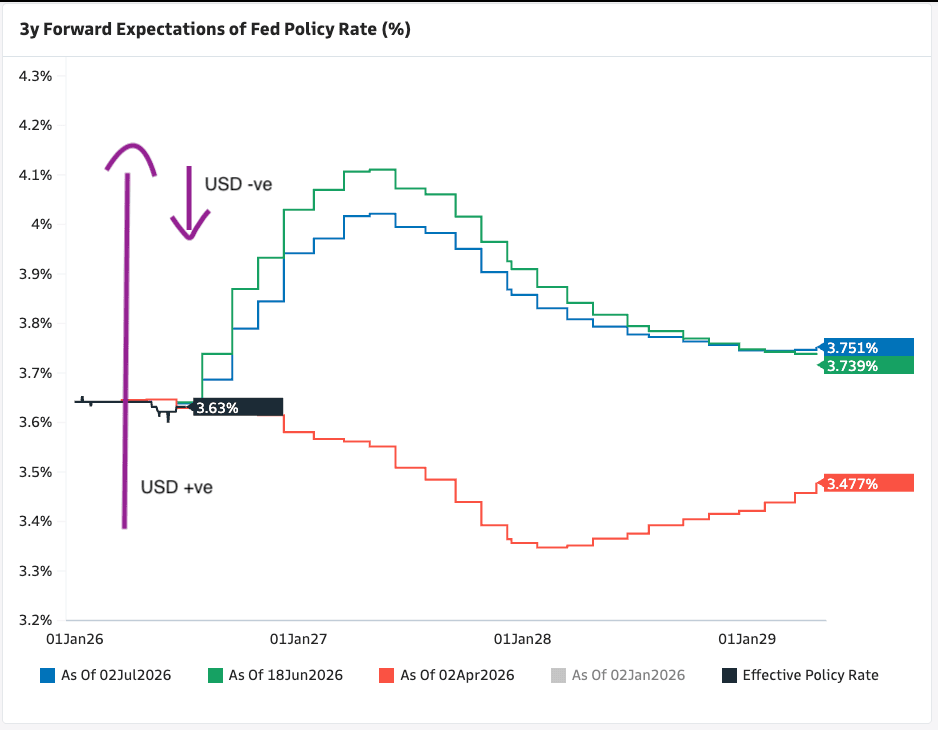

Last week's U.S. jobs report proved an important moment for USD, as it punctured a growing U.S. exceptionalism trade: after a run of above-consensus data prints, here was an undershoot that signalled the Fed might not have reason to raise interest rates this year.

"We think that the current market Fed rate hike expectations are already looking too aggressive and worry that the USD could suffer if the FOMC disappoints the hawkish bets," says Valentin Marinov, chief strategist at Crédit Agricole.

This week, the theme continues with ISM services due for release on Monday, which will give a timely snapshot of activity in this important sector. An above-consensus reading can help USD steady, an undershoot and the dollar could give more ground back.

Beyond Monday, the remaining numbers are second-tier and unlikely to shift the needle for the dollar.

"The more important focus will be on the Fed minutes (Wed), which should offer more colour on the first Warsh-led FOMC debate," says a daily market note from Lloyds Bank.

"The market will be interested in how pared back that document might be given the heavily trimmed statement and the general reticence of the new chair to say anything but the obvious, or just respond with a reference to the appropriate 'taskforce', as part of his journey to reduce Fed guidance," adds Lloyds.

The Fed held rates steady in June and reaffirmed its focus on price stability, while it published a dot plot showing 9 of 18 governors favouring hikes this year alongside raised inflation projections.

Should the minutes reaffirm a more 'hawkish' Fed stance is evolving, the dollar can recover. If not, and the minutes reflect a Fed that still sees a pathway to lowering rates, the currency can come under pressure.