Image © European Central Bank.

Strategists at Nordea Bank say euro-dollar will cross 1.20 next year.

The big talking point for FX markets is the powerful dollar upswing that has swept aside major technical barriers and injected unforeseen volatility that extends well beyond the main dollar pairs.

The breaking of technical barriers, particularly in euro-dollar, will have surprised those thinking the low-volatility FX environment was here to stay, while creating anxiety amongst market participants who are trying to gauge whether there's more to come.

Indeed, whether or not the dollar can continue this strength, or whether it retreats, will have multi-dollar implications for hedgers and those looking to make payments in the coming weeks. (We've covered the USD turnaround topic extensively over the past two days, see: Dollar's Warsh Boost Nears its Limits: Crédit Agricole and Pound-to-Dollar Recovery Nears.)

The headline from Nordea is that the move is fully justified owing to its strong fundamental underpinnings. However, the USD rally will soon reach its limits.

Why the Dollar has Strengthened.

Analysts say the dollar has strengthened because of a shift in interest rates on either side of the Atlantic in favour of the dollar.

To be more precise, the interest rates we are talking about here are the yields offered by bonds issued by governments in the U.S. and the Eurozone.

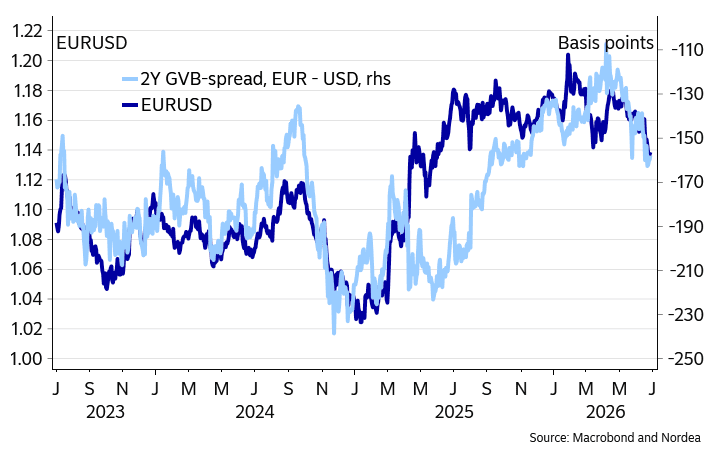

"The dollar has strengthened and the narrative appears to have shifted with rate differentials back in the driving seat for FX market development," says Nordea Bank.

The rule of thumb is that international investors borrow where lending costs are lower and invest in higher-yielding financial assets, like bonds. The supply and demand equation favours the recipient currency.

The argument is that this trade has increasingly favoured the USD of late.

"The two-year government bond yield has risen by around 5bp since the Fed’s meeting on 17 June. Meanwhile, the corresponding instrument in Germany has declined by around 4bp. The interest rate differential between the regions has thus increased roughly 10bp to around 160bp, which is the highest spread year-to-date," says Nordea.

"During the same period, the EUR/USD has gradually declined from around 1.16 to 1.138," adds the bank in a note out Friday.

Euro-dollar reached a low at 1.1324 on Wednesday before recovering to 1.14038 by the time of writing Friday.

That small recovery inevitably brings in the question of whether or not that's the end of the selloff and whether it is worth positioning for a recovery.

Before betting against the trend, the warning from Nordea is that "the obvious candidate for further dollar support is yield differentials, which could increase if the US continues to deliver stronger-than-expected economic data, forcing markets to keep revising up their expectations for Fed hikes this year."

So July's U.S. data round will be crucial.

But, risks are less two-way heading into the next data cycle, i.e. it will take increasingly sizeable upside beats in the data to deliver further USD gains. At the same time, even small undershoots against expectation can drive bigger downside reactions.

That opens the door to euro-dollar gains on soft data.

At these levels, positioning and value are also increasingly in favour of a euro-dollar recovery.

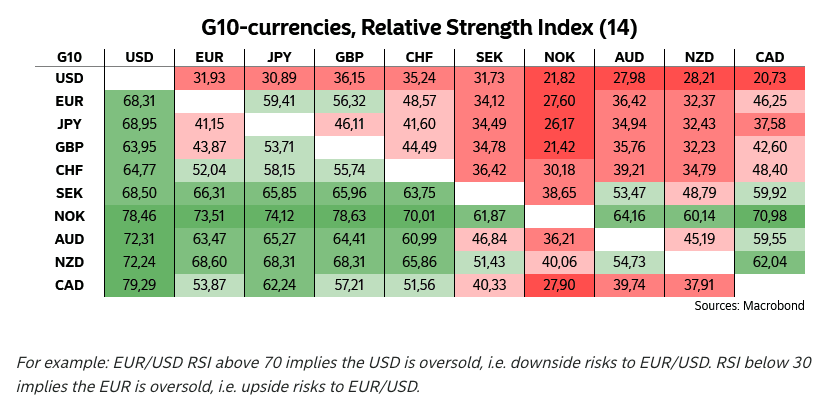

Nordea says relative strength indicators (see the chart above) suggest that the USD could be considered overbought against all G10 currencies.

"In the near-term, this leaves markets exposed to a potential recoil leading to the dollar weakening," says Nordea.

The bank forecasts EUR/USD at 1.16 towards year-end and 1.21 next year.