Image: Still courtesy of LBC, edit: Pound Sterling Live.

But Burnham Tax Threat a Headwind.

The British pound looks set to end the week on a high against a host of G10 peers, but we can't help but note the negative press headlines landing this morning.

The next Prime Minister has set the scene for a series of tax rises to fund increased spending, which is expected to weigh on sentiment and economic activity during the summer.

Andy Burnham has said that there is room in Labour’s manifesto for "movement on tax" as he draws up plans to increase public spending on council housing, infrastructure and defence.

The headlines will raise concerns that Britain faces a summer of paralysis as businesses and households withdraw in anticipation of higher taxes.

Such a retrenchment in activity would echo the slowdown of 2024 that followed Labour's election win, as the government primed the country for tax rises at its first budget with warnings of a massive black hole that needed filling. At the time, we called it "Starmer's shower of gloom."

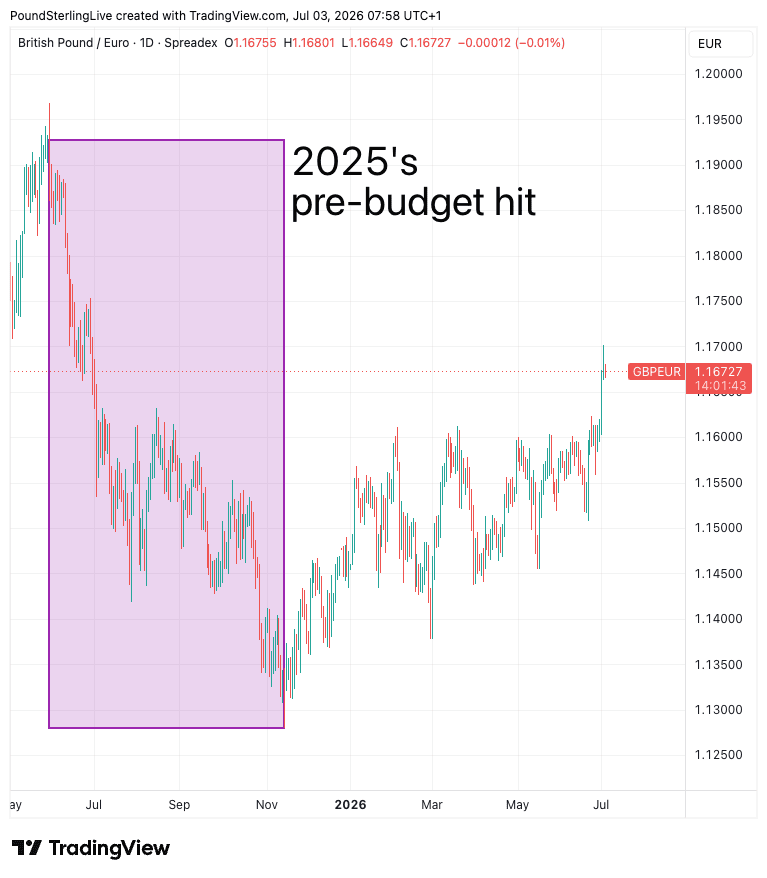

There was a similar period of angst running into 2025's budget, when Rachel Reeves had to find further funds to meet the fiscal rules. As the chart shows, the pound fell steadily into last year's budget, and it was only after it passed in November that the pound-to-euro exchange rate started to recover:

News outlets we follow report Burnham is looking at Capital Gains Taxes and business rates, as well as property tax changes designed to fall particularly heavily on the South East.

"We think many market participants are instinctively wary of Burnham given his previous comments. This means any missteps could see sentiment move against the new government," says Jeremy Stretch, Chief Global Strategist at CIBC Capital Markets.

For Now, the Pound is in Fine Fettle

The tax and policy headlines will be stored in the 'future problems' file as the market looks pretty content with the lack of any real substance flowing from Burnham.

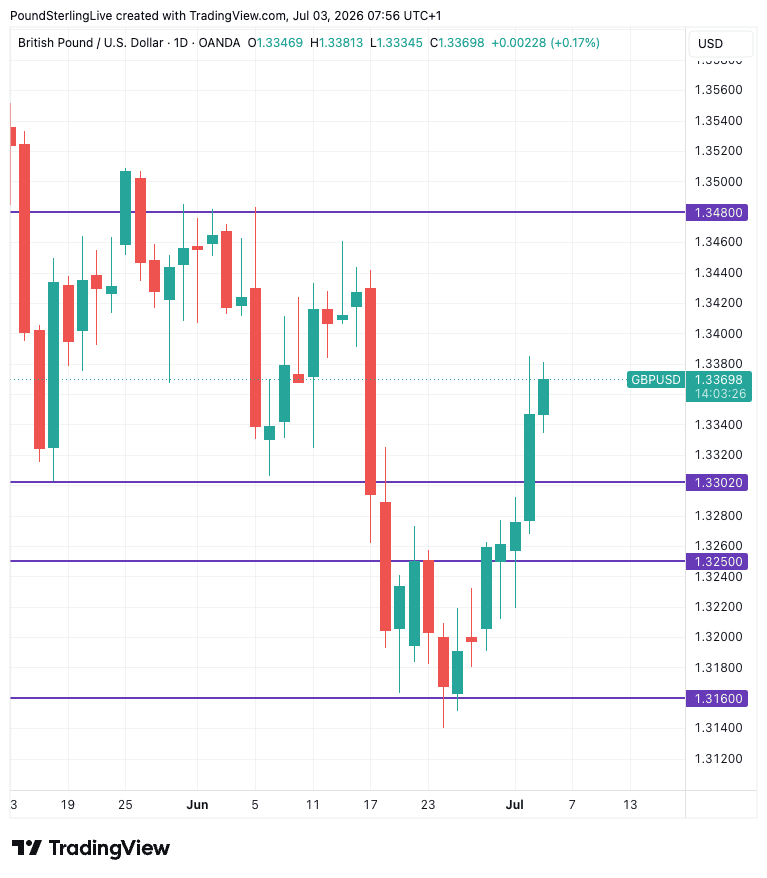

The GBP/USD rises to a two-week best at 1.3380, and the GBP/EUR had a stonking week, reaching its highest level in a year at 1.17.

That dearth of tradeable information on the Burnham front leaves it free to watch economic data, global drivers and interest rate differentials.

All are onside: the economy has been ticking over, the global backdrop is constructive with stocks riding high and the Middle East crisis fading.

But it's bond yields that are particularly supportive: the UK's real rate advantage over the eurozone and other G10 currencies remains notable, and that's driving demand for sterling.

To be sure, that advantage has faded against the U.S. dollar of late as the market looks for a prospective Federal Reserve rate hike this year. That's helped GBP/USD recover from lows at 1.3160 to 1.3378, a two-week high.

"The standout flow this week has been buying of sterling on crosses," says Goldman Sachs, having observed around 2BN in demand from a mix of hedge funds and real money, "mostly EURGBP but also other non USD pairs."

Goldman Sachs says "the trigger" for GBP demand has been a seemingly smooth handover to Burnham PM and his commitment again to fiscal rules.

Analysts at the Wall Street bank say they have "seen a few fresh long GBP recommendations based around this narrative."

However, the central theme across the analyst community remains that although there is near-term scope for outperformance, the medium-term picture remains difficult:

"We would disagree with thesis that GBP is a good fundamental long, whilst admitting that perhaps some of the tougher fiscal questions will only be addressed in November budget," says Goldman Sachs.

"Closer to the Autumn budget we expect fiscal risk premium to build," says Meera Chandan, FX strategist at JP Morgan in a recent GBP overview.

JP Morgan holds a near-term GBP/EUR forecast target of 1.1235 for when "fiscal risks being more fully priced in."