Image © Adobe Images

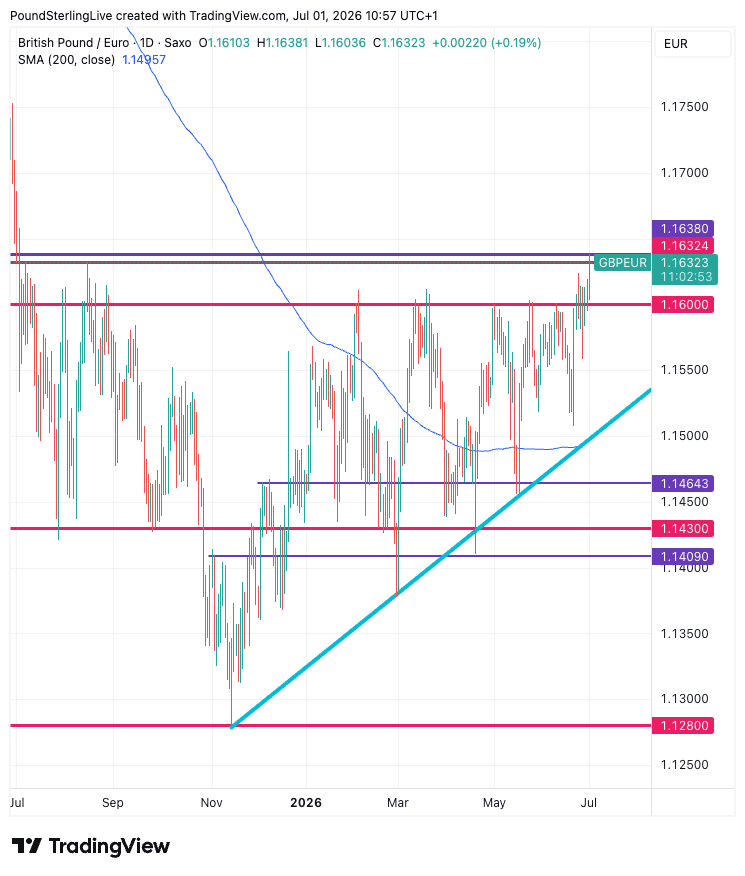

It was this time last year when the pound-to-euro traded at 1.1638.

Pound sterling has reached its highest level against the euro in nearly a year in midweek trade, helped by a soft Eurozone inflation print.

It's nearly a year ago to the day that GBP/EUR was last at 1.1638, and the new high is consistent with a steady, albeit slow, grind higher by the exchange rate since November.

The post-November gains are to a great extent a result of the unwinding anxieties associated with the Autumn budget, and that unwinding risk premium has not been challenged by the change in leadership underway in the UK.

"UK political risk remains persistently over-priced by markets, while the economy’s underlying resilience is consistently under-appreciated. Forward-looking macroeconomic expectations embedding political pessimism tend to understate UK real activity and the 'true' value of sterling," says Dr. Savvas Savouri, economist at QuantMetriks Advisory.

Why is the Pound Higher Against the Euro Today?

Yields and inflation dynamics look to be the short-term trigger for today's rise in the pound against the euro.

This morning's Eurozone inflation data significantly undershot expectations, landing at 2.8% in June from 3.2% in May, whereas the consensus looked for 3.0%.

Core CPI fell from 2.6% to 2.4%, undershooting consensus at 2.5%.

For the European Central Bank, this sends a clear message that fears that the energy price would trigger a new round of strong inflation were misplaced, and last month's rate hike might have been the wrong decision.

Indeed, that's something we flagged when covering Tuesday's French and German inflation numbers, and we could be talking about rate cuts before long.

That is certainly reflected on the fixed income markets where the policy-relevant two-year bond yields are doing the talking.

Because ECB rate cuts could come into the conversation, Eurozone bond yields are falling faster than elsewhere, including the UK.

The spread between the UK and German yields has risen as a result.

GBP/EUR often tracks this yield differential, and it's strong rise on Wednesday offers a likely on-the-day explanation for why the exchange rate is testing one-year highs.

Above: The UK minus German two-year bond yields.

Gilts are Doing the Talking

The pound was an unexpected gainer as the war in the Middle East escalated: rising oil prices raised the spectre of a global inflationary cycle, with the UK expected to be particularly hard hit.

When inflation is expected to rise, the market reacts by pricing in Bank of England rate hikes. That translates into higher UK bond yields (gilt yields) which in turn attract yield-seeking investor capital.

That bolsters the pound.

Analysts say the chasing of higher yields (the carry trade) is particularly strong in the current low-volatility market environment, and for the pound that means an advantage sparked by the war in the Middle East persists into early H2.

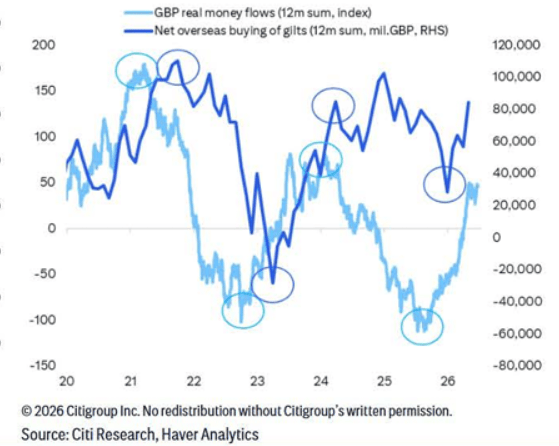

"We attribute this to foreign inflows into gilts amid attractive UK yields," says a new research note from Citi, referring to sterling’s resilience against the euro in recent months.

Citi says the pound still screens attractively on a carry-adjusted basis and that the Bank of England is unlikely to pivot dovishly over the next few meetings (i.e the residual support from gilt yields will remain).

"GBP has been resilient to political developments in recent months partly due to a persistent foreign bid for UK assets, which we expect to continue," says Bank of America in a mid-year currency research update.

GBP Risks Backloaded into the Autumn

For now, the path of least resistance looks to be higher; good news for those looking to buy their summer holiday money.

But headwinds are tipped by numerous analysts we follow to start emerging as the outlines of Andy Burnham's policy agenda become apparent.

"The GBP could also remain a pressure valve for anxious market participants that fret about the negative consequences from the change at the helm of the Labour Party and the UK government," says Valentin Marinov, Head of FX Strategy at Crédit Agricole.

Nick Wood, Chief Trading Officer at MillTech, says investors are concerned about whether a new leadership team would increase borrowing and spending.

Burnham has so far said he would continue to respect the rules that are in place to ensure the government doesn't borrow too much, but history shows these rules are usually altered to allow the administration in power at the time scope to borrow more.

Burnham has an ambitious list of policies, all of which require money. That's why the run-up into this year's Autumn budget could be another pain point for the pound.

"This autumn’s Budget will be the next landmark," says a recent note from Oxford Economics. "We think many market participants are instinctively wary of Burnham given his previous comments. This means any missteps could see sentiment move against the new government."