Image © Adobe Images

U.S. dollar falls as traders caught wrong-footed heading into the June jobs report.

The dollar fell noticeably in the wake of U.S. nonfarm payroll numbers that landed at 57K, almost half the 110K figure the market was watching.

The unemployment rate fell slightly to 4.2% from 4.3% previously, while hourly earnings were relatively steady at 3.5%, up from 3.4% last month.

Foreign exchange markets were primed for a strong print following June's run of above-consensus data prints that pointed to an improving economic backdrop.

"The fundamental strength of the US economy has underpinned a level of market performance in the second quarter not seen since the post-pandemic rebound," says Lindsay James, investment strategist at Quilter.

The prevailing narrative of an improving economy meant the market was sitting on the wrong side of the dollar trade when the undershoot came, confirming that risks leant heavily to the downside heading into the release.

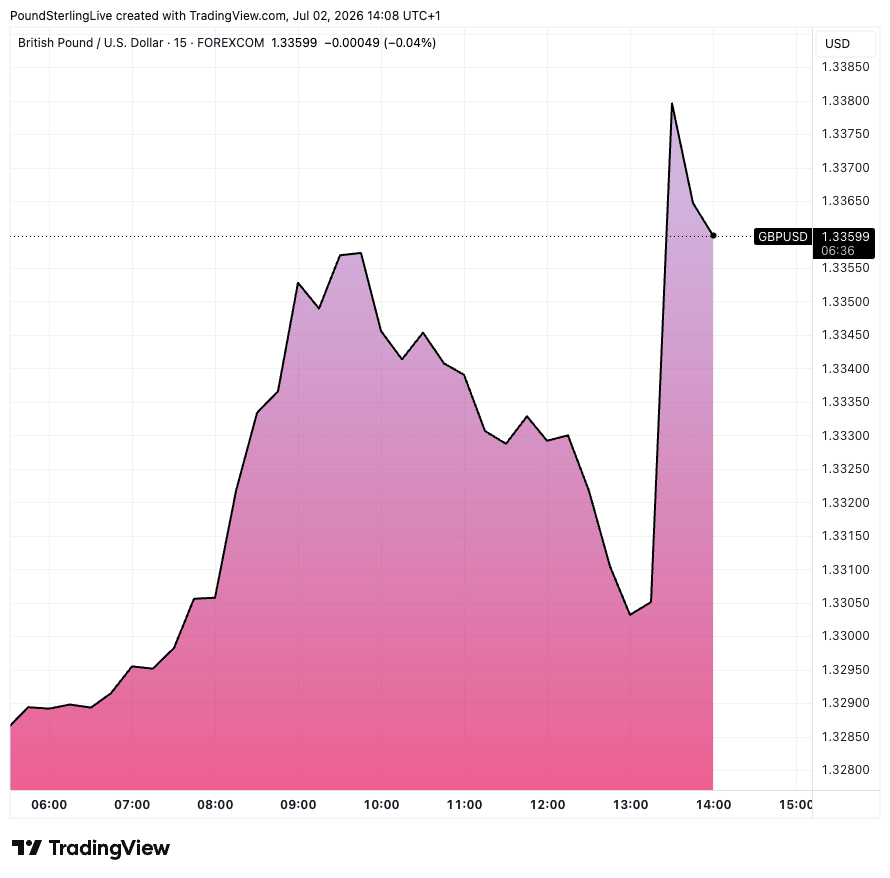

Following the release, the pound-to-dollar rate rose to 1.3380, the highest in two weeks. If the current 0.67% daily gain can be held into the close, the pair will be looking to record its biggest daily advance since mid-May.

The price action also suggests that a floor at 1.3160 underpins near-term trade and verifies the warnings of those analysts who had been warning for some time that the dollar was due to turn around following its strong June.

The long-dollar trade is crowded; positioning data shows a net-long position that's reached its highest level in 16 months. The pound is also crowded, but to the downside.

That creates prime conditions for a mean-reverting bounce-back, which is now well underway.

"Speculators are heavily short sterling, close to levels seen shortly after the Brexit vote ten years ago," says Georgette Boele, Senior FX Strategist at ABN AMRO. "The market is net long the US dollar and slightly long the euro, according to the latest data. This matters."

The dollar strengthened through June as investors reacted to a run of strong data and Fed Chair Kevin Warsh's commitment to fighting data, which implied he would raise rates if necessary.

The market has swung from expecting a series of rate cuts at the start of the year to now expecting a hike, a swing that has driven USD demand.

"We think that the current market Fed rate hike expectations are already looking too aggressive and worry that the USD could suffer if the FOMC disappoints the hawkish bets," says Valentin Marinov, chief strategist at Crédit Agricole.

Next Fed Move Will be to Cut

Post-jobs analysis from Pantheon Macroeconomics, the independent research house, finds the upturn in labour demand witnessed in recent months "now looks much weaker.

Cited are downward revisions to payrolls in April and May, followed by a muted increase in June, a sharp fall in the hiring intentions index of the NFIB survey and the weakening of the hiring intentions components of the regional Fed surveys.

Add to that a further drop in the Indeed and LinkUp measures of job openings.

Pantheon predicts payrolls will average 75K in the second half of this year, probably consistent with near-zero growth after revisions.

"All told, the labour market remains weak enough for the FOMC to relax about the risk of the energy price shock having broad effects on inflation. We continue to think the Committee will keep the funds rate unchanged in the second half of this year, and then will ease by 75bp next spring in order to shore up labour demand," says Samuel Tombs, Chief U.S. Economist at Pantheon Macroeconomics.