Andrew Bailey at the ECB conference, Sintra. Image: Claus Dirk/ECC, (c) 2026 European Central Bank

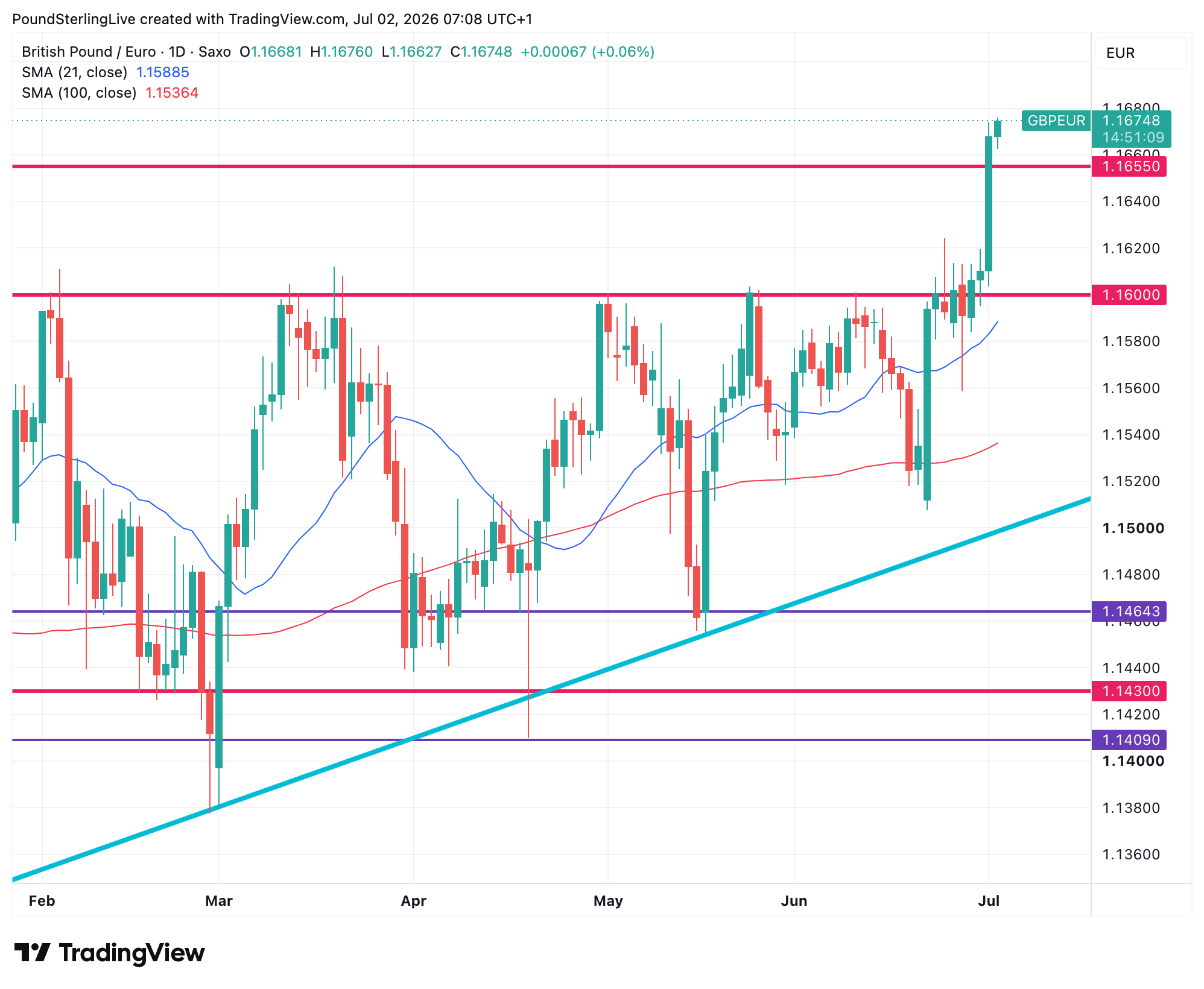

The pound-to-euro has risen to its highest level in a year.

The Bank of England's Governor, Andrew Bailey, has said talks about lowering UK interest rates were "off the table at the moment."

Speaking in Sintra, Portugal, the Governor indicated he remained wary inflationary pressures would build as a "delayed reaction" to the effects of the Middle East conflict.

The comments were read as relatively hawkish by market participants, helping British bond yields hold their daily gains against eurozone counterparts, translating into GBP outperformance on the day.

"The BoE’s Bailey voiced regret over past forward guidance practices and aligned with the broader retreat from detailed predictive signalling," says a morning strategy note from Rabobank.

That rise in UK bond yields relative to those of Germany and other European nations typically boosts the pound, as foreign capital flows to where returns are greater.

The developments helped GBP/EUR close at its highest level in more than a year, placing it well above a major resistance line to confirm the exchange rate had potentially stepped out of the confines of a range that had cocooned it for the past year.

As the Bank of England's Bailey shored up UK rates by pushing back against considerations for a cut, expectations for Eurozone interest rates headed in the opposite direction as a soft inflation reading earlier in the day cast doubt on the need for last month's ECB rate hike.

Eurozone inflation data significantly undershot expectations, landing at 2.8% in June from 3.2% in May, whereas the consensus looked for 3.0%. Core CPI fell from 2.6% to 2.4%, undershooting consensus at 2.5%.

For the European Central Bank, this sends a clear message that fears that the energy price would trigger a new round of strong inflation were misplaced, and last month's rate hike might have been the wrong decision.

If so, euro-relevant bond yields can weigh.

Why the Pound is Stronger Against the Euro

The pound has strengthened against the euro for a number of reasons, most important of which is the aforementioned UK bond yield advantage.

It's interesting to note that the Sintra conference was characterised by a bevvy of the world's leading central bankers all talking tough on inflation. The Fed's Kevin Warsh, the ECB's Christine Lagarde and the BoC's Tiff Macklem were in no mood to consider lowering rates owing to the inflation threat.

Warsh reinforced the importance of Federal Reserve independence and indicated anyone expecting tolerance for inflation above 2% "would be disappointed."

Given the moment, the Bank of England's Bailey could hardly diverge on tone, ensuring he was effectively boxed into also striking a 'hawkish' tone; if you were a central banker breaking rank in that room on Wednesday, your currency would have taken a hit.

Resistance Gives

Technicals are an important driver of the move in GBP/EUR: a break above the massive 1.16-1.1630 resistance zone opens up some clear air for further gains and if resistance turns into support, GBP/EUR could settle above the 1.16 level.

"There was no particular catalyst, but probably the slightly softer euro and the proximity to big support levels triggered some unwinding of stale sterling short positions," says Chris Turner, head of analysis at ING Bank.

According to the ING analyst, asset managers in particular have been running some large sterling short positions. "At the same time, it is expensive to be short sterling, where one-week rates are around 3.80%, and with volatility falling we are probably seeing some position liquidation."

Markets Fade Political Concerns

Image: Pound Sterling Live.

The perennial political intrigue that tends to weigh on the pound has faded of late, with markets identifying that the incoming Prime Minister Andy Burnham is wary of triggering a bond market rout by introducing any unfunded spending commitments.

"There is probably also the view that UK politics may not come back to weigh on sterling until the end of this month or in August," says Turner.

Nevertheless, there's a strong consensus amongst the analyst community that political and fiscal problems have been deferred owing to the transition of leadership and the impending summer holidays that will see politicians slink into the sidelines. The consensus does expect the issue to return in prominence when Parliament resumes in September and the Autumn budget approaches.

"The likely next PM has already committed to the fiscal rules, nevertheless we think he will face significant pressure to spend more," says Elliott Jordan-Doak, economist at Pantheon Macroeconomics.

Burnham has hinted at greater spending, saying "while not taking risks with public finances, I will seek to give Britain some breathing space [from rising costs]".

"So, we think the risks are that Mr. Burnham will deliver a taxand-spend Budget in the autumn, and tweak the fiscal rules to allow more room to borrow," says Jordan-Doak.

These risks should ultimately cap the pound's advance.