Image © Adobe Images

Our Week Ahead Forecast looks for an extension of GBP/AUD upside.

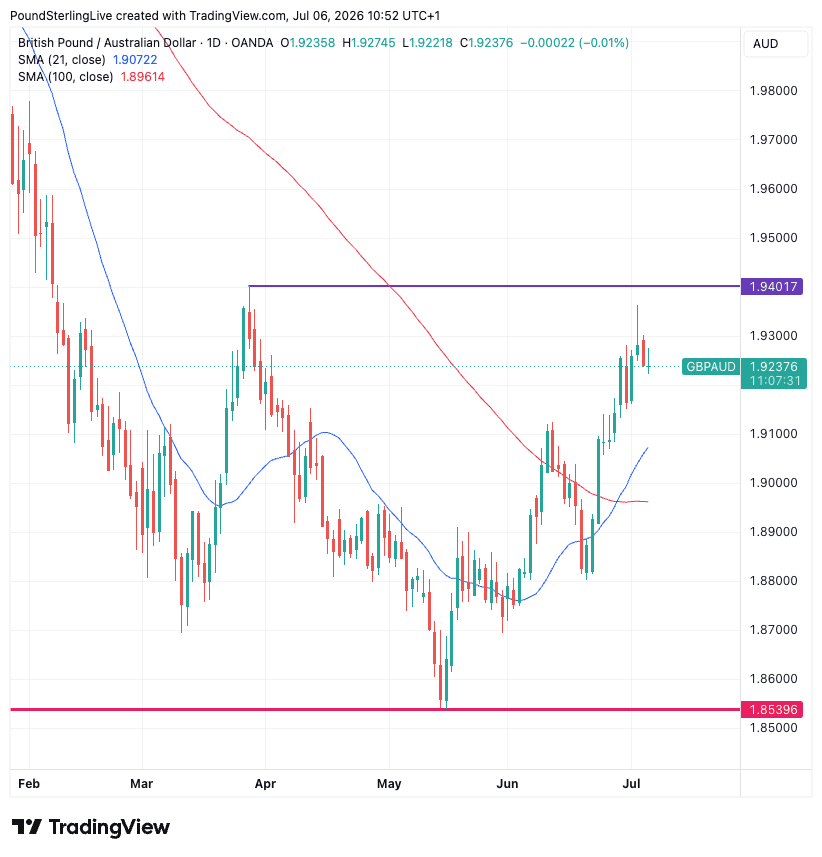

The balance of probabilities continues to favour further gains after the pound-to-Australian dollar reclaimed key moving averages and registered a bullish crossover of the 21-day above the 100-day moving average.

This is therefore a setup that's constructive and the path of least resistance is higher, until at least the descending 200-day moving average is encountered; it's presently at 1.95.

So there's scope for near-term gains yet:

The balance of probabilities favours GBP/AUD upside after the pair reclaimed both key moving averages and registered a bullish crossover of the 21-day above the 100-day moving average.

That crossover suggests buying momentum is strengthening and increases the likelihood that dips will find support.

The immediate objective is a break above 1.9402, which would clear the way for a test of the 200-day moving average at 1.9530.

That level represents the key technical hurdle for the medium term: a sustained move above it would signal that the broader downtrend has likely ended and strengthen the case for a more durable advance.

Failure to overcome resistance may trigger consolidation, but the technical outlook remains constructive while GBP/AUD holds above the rising 21-day moving average.

What Will Influence the GBP/AUD This Week?

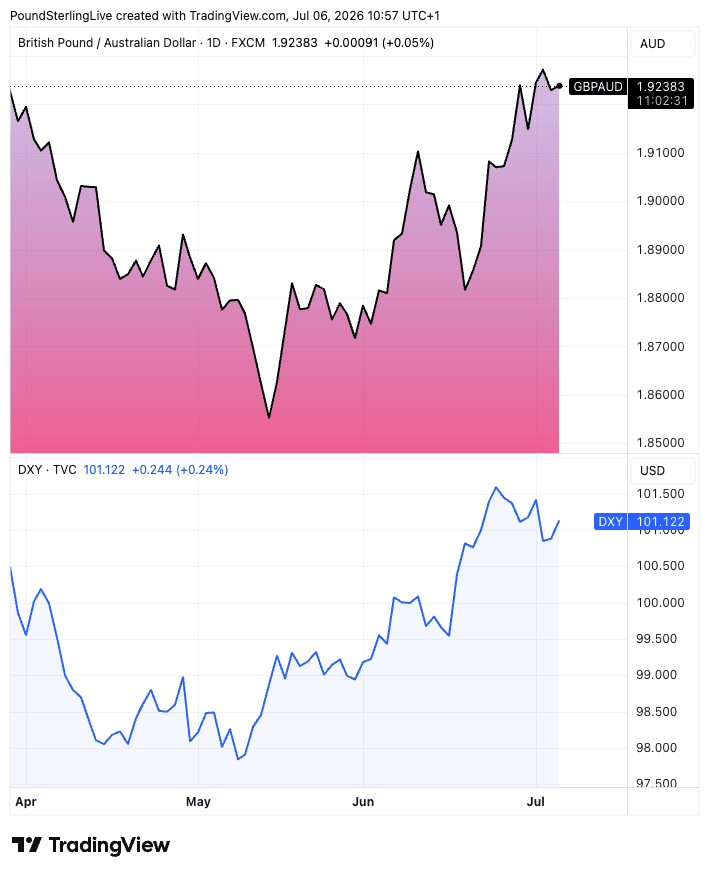

The pound-to-Australian dollar exchange rate remains dependent on what the bigger dollar is doing.

That's because a key feature of AUD trade over the past two months or so has been the overriding importance of the dollar recovery: it's proven a massive headwind to AUD's ability to appreciate in value:

Above: The performance of the dollar has been instructive of GBP/AUD performance lately.

Unpacking the AUD's vulnerability to the dollar's recent advance rests with its high-beta, pro-cyclical, commodity-linked status.

But we need to dig a littler deeper and understand why the dollar is rising: it's rising because interest rate expectations are also rising, and that's because market participants no longer see interest rate cuts from the Fed.

In fact, they think there's a chance rates will rise in the future.

That's a world of higher interest rates, regardless if you are an American or not, for the simple fact that dollar funding is the bedrock of global finance.

And rising dollar funding costs are a headwind to growth that blows in the face of those currencies that do well when the growth cycle is on the up, namely the Aussie dollar.

So the coming week for GBP/AUD could well be determined by how the USD performs.

On this count, we note that USD suffered a setback on Thursday when U.S. jobs data undershot estimates and cooled Fed rate hike bets somewhat. That stemmed GBP/AUD losses.

Looking ahead, if the USD pares recent gains, so too will GBP/AUD.

With that in mind, it's all eyes on U.S. data this week:

Monday 7 July

Two services readings land back to back: the S&P Global final services PMI for June at 9:45am (14:45 BST) and, more importantly, the ISM Services PMI for June at 10am (15:00 BST). ISM services registered 54.5 in May, the 23rd consecutive month in expansion.

The market is looking for continued mid-50s expansion, though prediction-market pricing is unusually split on the June print.

The internals are where the signal is: services employment has now contracted for three straight months on hiring freezes, while the prices-paid index hit its highest since August 2022, so a hot prices component would cut against the softening-inflation narrative.

Tuesday 7 July

May trade balance at 8:30am (13:30 BST). A tariff-era release worth watching for how import and export flows are adjusting under the Section 122 measures, but rarely a market-mover in isolation.

Wednesday 7 July

The week's main event: FOMC minutes from the June meeting at 2pm (19:00 BST), alongside final May wholesale inventories at 10am and May consumer credit at 3pm.

June was a pause, with Warsh framing persistently high inflation as a burden and stripping out the traditional forward guidance.

Because Warsh chose not to participate in the dot plot, the minutes are the primary window into the internal debate, specifically how close the committee is to a hike versus an extended hold, and how divided it is.

Note the context shift since the meeting: a soft June payrolls print landed on 3 July and has already cooled near-term hike bets, so the minutes will be read against a slightly dovish repricing.

Thursday 9 July

Weekly jobless claims for the week ending 5 July at 8:30am (13:30 BST), plus June existing home sales at 10am.

Claims are the timeliest labour read on the docket and carry more weight than usual given the employment softening now showing up in the survey data.