Image © Adobe Images

Sterling can find support as policymakers delivered a relatively guarded assessment of the economy and inflation outlook.

What Happened: The Bank's decision-making committee (the MPC) voted by a majority of 7-2 to maintain Bank Rate at 3.75% while the minutes are consistent with Bank Rate on hold for an extended period.

What This Means for FX: That 7-2 vote is expected. Had it been 7-1 or 7-0 in favour of a hold, the market would have rapidly repriced towards the next move being a cut.

Reading the statement, the Bank could also have chosen to express relief that oil prices have fallen dramatically over recent days, but they didn't, hinting there's still an element of caution on the MPC. "The impact of the energy shock on the UK economy remains uncertain," read the statement.

Had they expressed a greater sense of relief, the read across to markets would be that it's clear the Bank thinks it can lower its guard against inflation and open the door to discussions about rate cuts in the coming meetings.

That would have been a 'dovish' outcome and one that would have weighed on the pound.

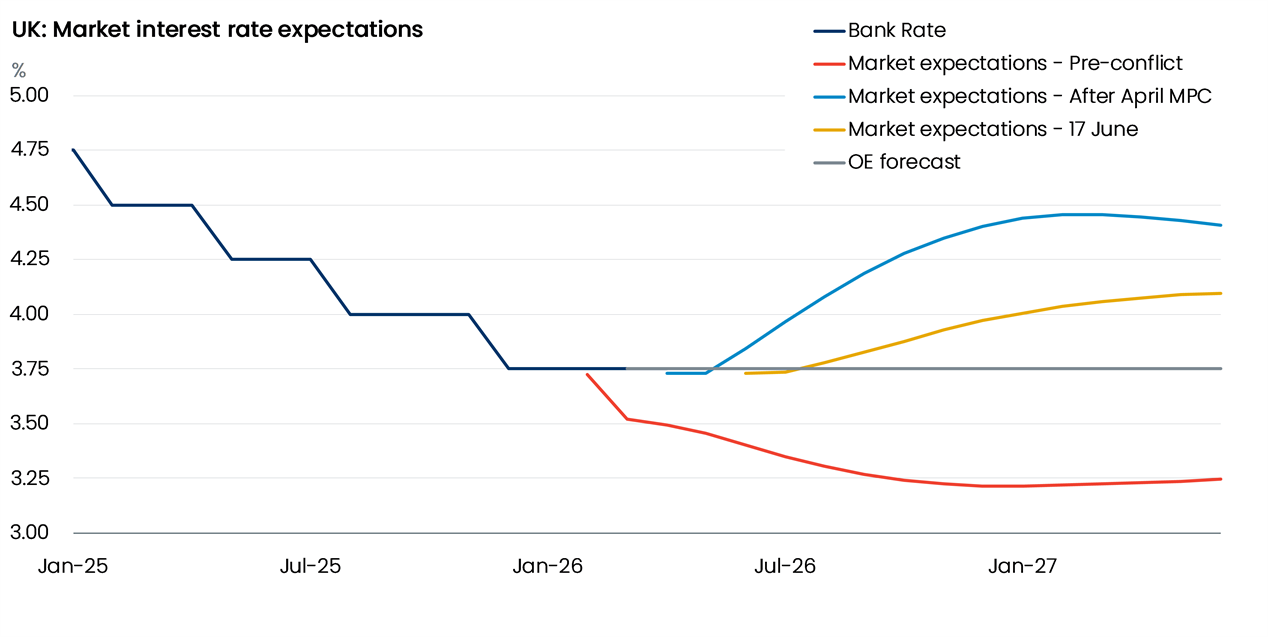

Image courtesy of Oxford Economics.

Instead, this is still a central bank that is cautious about inflation: "The Committee stands ready to act as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term," it said.

"Looking ahead, we continue expect the MPC to remain on hold this year given a restrictive policy stance, tighter financial conditions, and a weak cyclical backdrop that should limit the extent of second-round effects," says Goldman Sachs.

Bottom line: This was no 'dovish' hold. For the pound, that should offer some degree of support and limit downside.

"We thought the BOE would have a dovish hold today, we were wrong," says Kathleen Brooks, an analyst at XTB. "BOE stayed on hold, but it was much more hawkish than we expected. 7-2 vote split and the BOE kept its guidance that it’s ready to act to stem inflation."

Still Under Pressure

Nevertheless, the pound has been under pressure of late as falling oil prices weigh on UK bond yields, which in turn pressure the pound lower.

On the day, there was a definite GBP selloff triggered on the announcement, but that will certainly be an algo-driven reaction to the text of the minutes.

The pound-to-euro trades at 1.1534; the interim intraday floor is forming at 1.1530. The pound-to-dollar trades at 1.3217, and looks to be under some sustained selling pressure. For this pair, the USD remains dominant and the post-Federal Reserve reaction will prove far more instructive going forward.

Primed for the Doves

Markets were prepared for a dovish tilt today: traders got ahead of the risks posed by the Bank by selling sterling early on; the GBP/EUR rate traded at its lowest level since May 29 in the hours leading to the decision.

Expectations for a dovish tilt were encouraged by Wednesday's inflation undershoot, where the headline only managed to reach 2.8% y/y and not the 3.0% expected. Core inflation was also softer than anticipated.

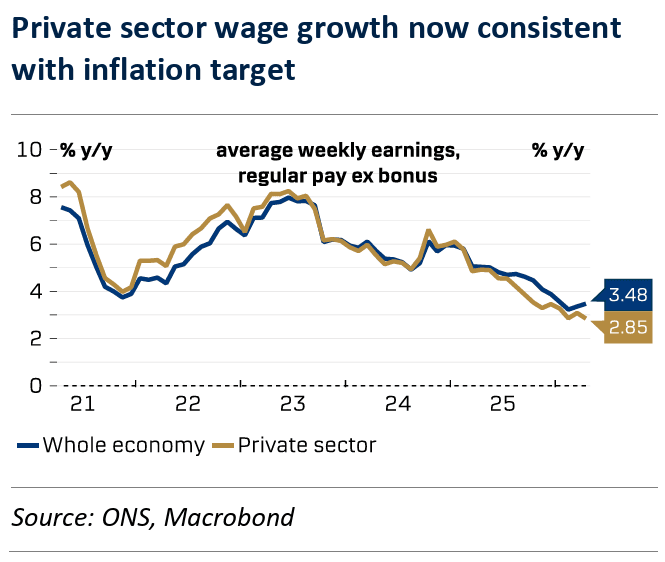

Thursday's labour market data added to the sense that there's no need to raise rates; the risk of a wage-price inflationary spiral is now vanishingly small: wage growth was unchanged in the 3-months to April at 3.4%, the lowest level since 2020.

Image courtesy of Danske Bank.

That's important for the Bank of England: rising wages boost demand in the economy, which can lead to higher inflation. It also prompts employers to raise their own prices, further contributing to inflation.

By raising interest rates, the Bank squeezes the ability of firms to pay higher wages, thereby dampening inflationary risks.

With the data now consistently showing the wage-price trend is slowing, the Bank will feel less inclined to raise interest rates.

Oil Prices and Inflation Risks Fall

The market drastically raised expectations that the Bank would need to raise interest rates in the coming months following the start of the conflict in the Middle East, which threatened to boost inflation.

That uplift was reflected by a strengthening pound which rose against the euro, dollar and other currencies through April. In fact, during the April-May period, characterised by elevated oil prices, the pound was the third-best performing currency.

With a Middle East peace deal in the offing and a potential return of Iranian oil to the market, inflation expectations are falling sharply, and the pound is reversing its war gains as it becomes clear there's likely scant chance of a rate hike on the forseeable horizone.

But ECB and Fed Decisions to Constrain BoE Dovishness

Bear in mind that the Bank will also be aware that the ECB raised rates last week and the Federal Reserve struck a 'hawkish' tone overnight: it can't stand out as being a 'dovish' outlier, as it knows this will penalise sterling, and that would be unhelpful if it pushes up the cost of imports (i.e. a weaker pound is inflationary).

"Weaker Sterling, on the perception of the BoE lagging peer central banks’ response to the energy shock, could end up leading to forecasts for higher imported inflation for the UK and be the factor that forces a belated BoE rate hike," says Sam Hill, Head of Market Insights at Lloyds Bank.

Sterling Outlook

Thursday's decision wasn't the bearish blow for the pound that it might have been, and a near-term post-decision recovery wouldn't be surprising.

However, any gains should prove relatively limited going forward, as the pendulum is swinging back towards a more benign inflationary outlook, and that should diminish sterling's interest rate advantage over the medium term.