The GBP to NZD conversion is sharply lower at the start of the new week as the recovery in the pair fails to convince.

Pound Sterling is unlikely to develop notable upside pressures against a robust New Zealand dollar over the course of the coming week, we believe.

The pair trades at 1.8144 at the time of writing - well within the ranges we have become used to since mid-August.

In fact, the problem for GBP/NZD is that both currencies have been outperforming their other G10 peers.

In the week ending 2nd September the Pound was the best performer in G10, followed by the NZ Dollar.

The Pound has rebounded after Brexit concern have so far failed to manifest in recent data, which was by and large positive.

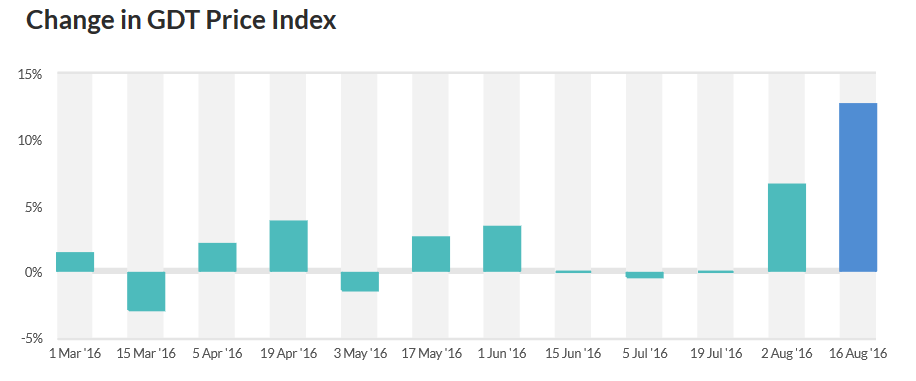

New Zealand data has also excelled, most notably in the case of prices for Dairy exports, which showed an above average 12.7% rise on August 16, and account for the largest proportion of the country’s soft exports:

In the week ahead the main release for New Zealand will be the next result of the Global Dairy Auction on Tuesday September 6, and a further rise in Dairy prices will help the kiwi higher.

Recent data has shown how the ‘new wave’ of New Zealand exports, including Kiwifruit, Wine, Apples and Seafood, have all risen by over 10% in June 2016 over the year, further supporting the economy and the currency.

NZ Business Confidence data which shone in July, jumping to 16, rose by an equally impressive 15.5 in August.

As a result of the strong data BNZ bank have raised their forecast for New Zealand growth in 2016 to 3.2%, and 0.8% in Q2, to reflect the improving outlook.

The kiwi also continues to gain support from the relatively high interest rates in New Zealand which continues to attract flows of capital seeking higher yields.

GBP/NZD is showing a marked lack of strength in the pound’s rebound from its early August lows:

Further, despite positive UK manufacturing PMI data out on Thursday pushing the pair higher, it has hit tough resistance at the 50-day moving average at 1.8275.

The lack of momentum in the move higher and the fact that the trend in the longer-term is down, leads to expectations that the pair will probably capitulate and resume its longer-term trend lower eventually.

As such, a break below the 1.7691 lows, would lead to a move down to a probable target at 1.7500.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3528▲ 0%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.2728 - 2.2822 |

**Independent Specialist | 2.3199 - 2.3293 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

UK Data to Watch

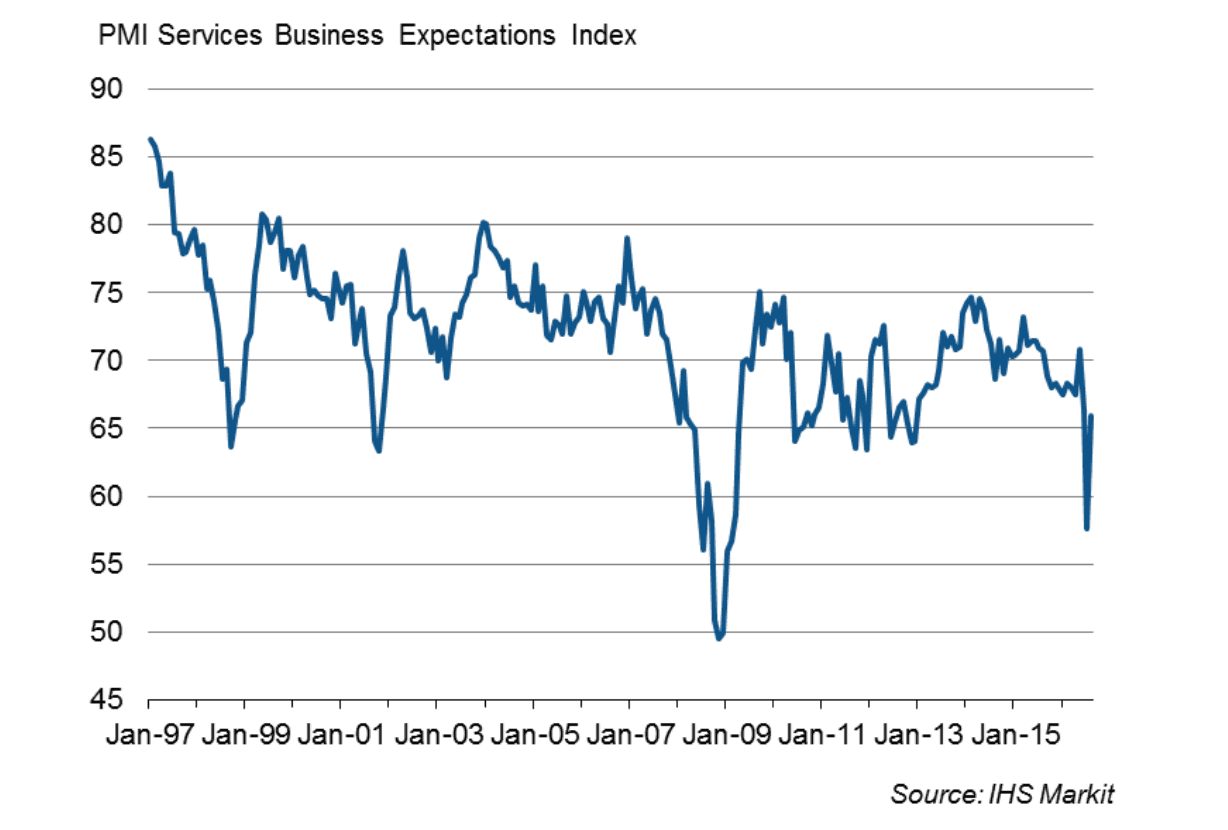

A strong start to the new week was gifted to Sterling after Services PMI data from IHS Markit and the CIPS have confirmed the economy's largest sector expanded in the month of August, putting behind it the slump seen following the UK's vote to leave the European Union.

The data read at 52.9, well ahead of economist forecasts and market positioning that expected a reading of 50 to be delivered.

Business have reported that the uncertainty posed by the EU vote has started to abate with the forward-looking business expectations index recovering most of the ground lost in July:

Of note, it has also been reported that inflationary pressures are rising as a result of the weakened Pound.

Encouragingly, job creation has resumed in August having paused in July.

"Business optimism ricocheted back to pre-Brexit levels, reassured by market stability and clients bringing dormant projects back to life. Whether this steadiness continues will largely depend on the sector’s reaction to the UK Government’s approach to the Brexit negotiations as the sector keeps one eye on business as usual and one eye on possible obstacles ahead," says David Noble, Group Chief Executive Officer at the CIPS.

The other main release from the UK this week is Manufacturing Production – with analysts estimating a fall of -0.4% mom in Jul, from -0.3% in June.

The recent rebound in Manufacturing PMI suggests, however, that the consensus estimates may be overly pessimistic.