The Pound to New Zealand dollar exchange rate is likely to lose ground according to BNZ who have told clients they are upgrading their NZD targets.

Analysts at BNZ have upgraded their forecasts for the NZ Dollar, telling clients they see a "stronger-for-longer" profile.

Much of the revision reflects a weaker USD and GBP, with the later being hit by expectations for more aggressive easing by the Bank of England and the possibility of a delayed process to exit the EU adding to the downside potential for Sterling.

The soft USD and further central bank easing have increased global risk appetite and boosted commodity prices.

"This dynamic has increased the near-term attraction of the NZD. Signs of a robust domestic economy and the RBNZ maintaining a cash rate at a significant premium to offshore policy rates are added NZD-positive dynamics," says BNZ's Jason Wong.

BNZ's forecasts reflect a strongerfor-longer NZD profile than previously thought.

The GBP/NZD is forecast to trade at 1.7857 in December where it will remain through to June 2017.

1.69 is forecast for December 2017.

With regards to the NZD/USD exchange rate, BNZ see 0.70 by December 2016, 0.68 by June and 0.67 by December 2017.

The NZD/AUD rate is forecast at 0.93 in December 2016, 0.94 in June 2017 and 0.96 in December 2017.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3528▲ 0%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.2728 - 2.2822 |

**Independent Specialist | 2.3199 - 2.3293 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Flourishing New Zealand Export Basket to Keep NZD Well Bid

The strong growth in alternative commodity exports over the course of 2016 is seen as a positive sign for the New Zealand Dollar going forward and indicates continued robust flows generated by the export side of the economy.

New Zealand lamb is famed the world over, but its supremacy in the New Zealand export basket is being challenged by the growth in exports of kiwifruit, wine and apples, according to recent analysis by BNZ bank’s Doug Steel.

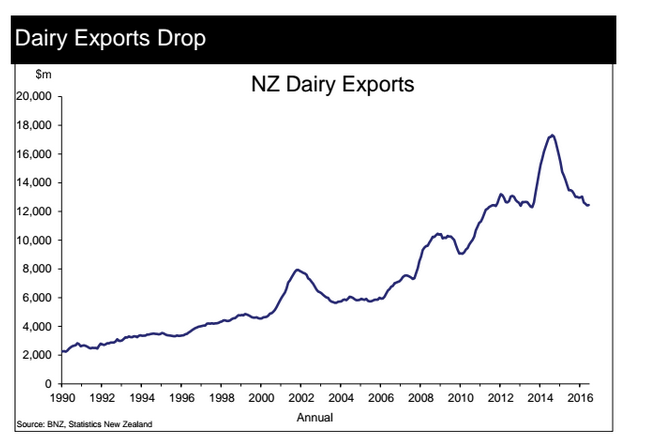

This new breed of soft commodity exports has seen volumes surge over recent years, even as more traditional mainstays such as dairy and meat volumes have lost ground or flat lined.

“Horticulture has been a standout performer with exports surging higher over recent years. Annual horticulture exports are now nudging $5b. They account for 10% of NZ’s total merchandise exports. The sector is now well on its way to achieving its target, set back in 2010, of $10b exports by 2020,” says Steel.

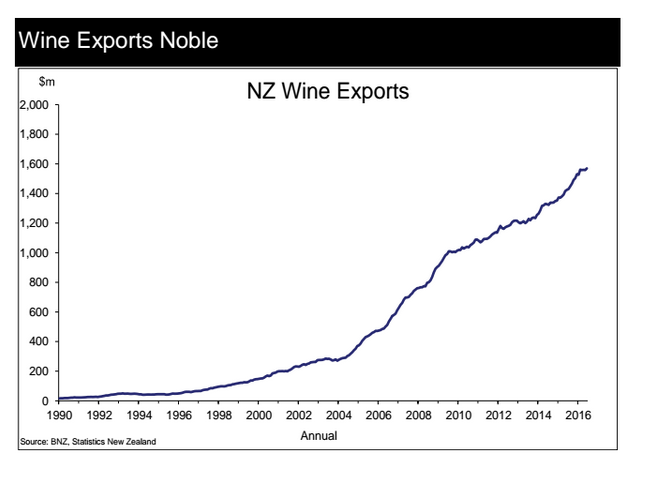

Wine exports were 10% higher in year-to-June 2016 as a result of tighter more competitive pricing and increased supply.

New Zealand wine is very popular in the UK with over half of Sauvignon Blanc wine consumed coming from New Zealand.

About a quarter of New Zealand wine exports go to the UK which is the third largest destination for kiwi wine.

The UK market is expected to shrink, however, since the pound’s loss of value post-Brexit.

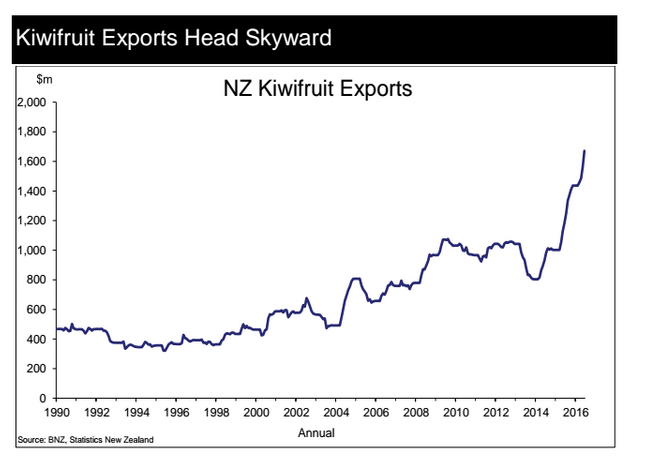

Kiwifruit has seen an exceptional increase in export volume in recent years.

Export volumes have doubled since 2013, including a 41% increase in the year to June 2016 alone.

Rises are expected to continue as a premium priced new variety called Sungold (G3) comes online.

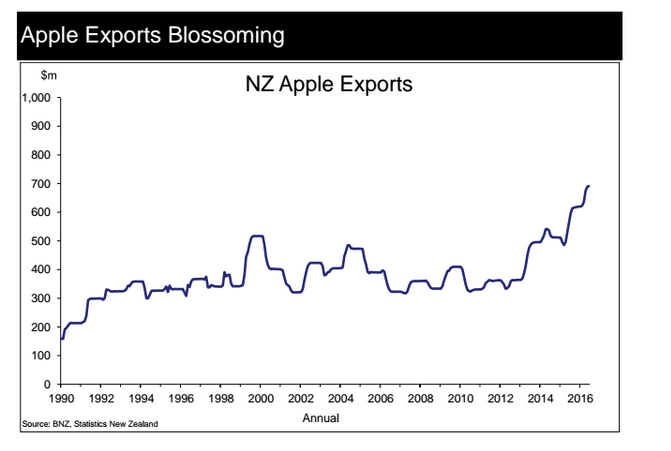

Apple exports have ‘blossomed’ by 23% from a year earlier in June 2016, as a result of more trees being planted and more premium priced varieties.

Seafood is another new soft commodity export which has contributed to the recent growth of New Zealand’s unorthodox commodity cornucopia, after showing a 13% rise in June 2013 from a year ago.

Meanwhile more traditional commodities such as Dairy exports and Wool have fallen, by 8% and 5% respectively and Sheepmeat’s have flat-lined.

Technical Analysis of GBP to NZD Exchange Rate

The pair is showing signs that the down-trend is tired despite the positive outlook from the fundamental arguments already expanded on above.

There is a wide bullish convergence between the MACD momentum indicator and price which made a new low in August a few points below the July trough but failed to generate anyway near the same level of downside momentum - a sign there may be a strong bounce from this trough at the very least – possible even a form of broader reversal.

There have been three up days in a row since the August 11 lows, another strong indicator of reversal, but it is a pity they were not, longer green candles, as I would hesitate to label such diminutive plus days as a ‘Three White Soldiers’ Japanese candlestick reversal pattern, even if they fulfil some of the criteria and come at the end of a down-trend. Nevertheless, they are yet another warning sign of exhaustion and reversal.

The move down from the May highs contains some of the hallmarks of a complete Elliot Wave sequence, a further sign the pair may be basing and ready for correction.

The surest sign a reversal was occurring would be to see the exchange rate break above the trend-line for the move down (turquoise line) situated at around 1.8250/1.8300.

Such a break, confirmed by a break above 1.8310 would probably lead to a breakout to at least 1.8450, if not 1.8500.