Image © Adobe Images

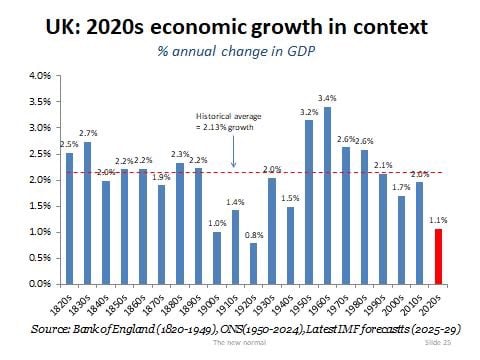

The latest GDP figures underline the fragility of the UK economy, reinforcing concerns that the current decade is shaping up to be the weakest for growth in a century.

The economy grew by just 1.3% in 2025 as a whole after putting on 0.1% q/q in Q4, and there is little in the latest growth breakdown to suggest a decisive turning point is imminent.

"The economy grew by just 1.3pc in 2025 as a whole, with the 2020s on course for the worst UK growth performance since the 1920s - the most dismal decade for growth in 100 years!" - Andrew Sentance, economist and former Bank of England rate setter.

Quarterly expenditure breakdowns show government spending remains the main contributor to growth in Q4, confirming that the government's massive borrow-and-spend programme is proving the difference between recession and stagnation.

Image courtesy of Andrew Sentance.

That's not inspiring, as secular economic growth stories that generate better living standards rely on private sector ingenuity and investment.

"Subdued growth is a function of slower than expected private sector consumption and or a moderation in the pace of government spending. However, the drag from business investment likely reflects the extended period of pre-Budget uncertainty and could be temporary," says Jeremy Stretch, International Strategist at CIBC Capital Markets.

Indeed, survey data suggests the UK economy is ticking again up in 2026: services output rose 0.1% in November and 0.3% in December and the UK services PMI survey picked up from 51.4 in December to 54.0 in January.

"There are hopes that the upswing in this area has continued into 2026," says Nikesh Sawjani, Senior UK Economist at Lloyds Bank.

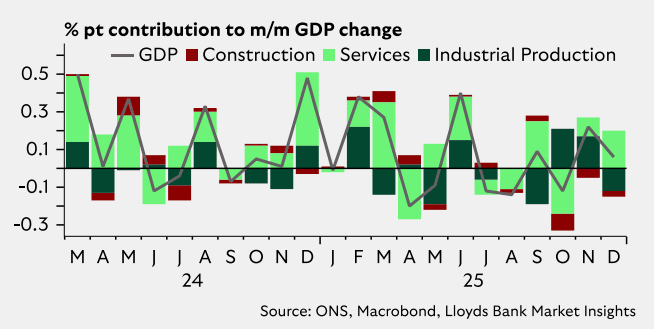

Above: Peaks and troughs around the zero line spell a stagnant economy.

Expectations for lower inflation and another Bank of England interest rate cut add some momentum to the post-budget relief uptick.

But this type of recovery mustn't be confused with the start of a genuine secular growth trend as any upswing that is based on relief-style bounces and 'less bad' vibes is not sustaining and is very different to a genuine secular upshift.

In fact, the incoming Q1 growth would be entirely in keeping with the now-familiar pattern of recent months: peaks and troughs that oscillate around the zero line.

Nothing we are seeing is consistent with a genuine recovery led by the private sector and productivity gains.