Pound Sterling rallied to a three week best against the Euro and a one week best against the US Dollar after the release of surprisingly strong manfuacturing data from the UK economy which many analysts attribute to the recent declines in GBP exchange rates.

- Manufacturing PMI data in strongest gain in 25 years

- RBS confirm they retain a forecast for a lower GBP going forward

- Pound to Euro exchange rate today: 1.1896

- Euro to Pound Sterling exchange rate today: 0.8418

- Pound to Dollar exchange rate today: 1.3252

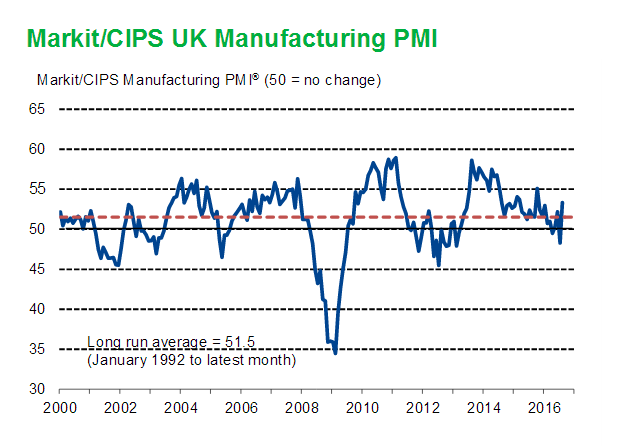

GBP surged higher against its major competitors following the release of some exceptonally strong manufacturing PMI data released by IHS Markit and the CIPS.

The reading rose to a seasonally adjusted 53.3 last month from a reading of 48.2 in July.

This is a 10-month high and the month-on-month increase in the level of the headline PMI (5.0 points) was the joint-greatest in the near 25-year survey history.

Analysts had expected the index to rise to only 49.0 in August.

It appears that the surge has been driven by a weaker Sterling, confirming previous surveys that hinted that the sector had been kicked into life by the fall in the exchange rate.

The report notes:

"Improved sales volumes to markets such as the USA, Europe, China, South-East Asia, the MiddleEast and Norway led to a further increase in new export business during August. Moreover, the rate of growth accelerated to a 26-month high.

"The depreciation of the sterling currency was by far the main factor manufacturers cited as supporting the upswing in new export work."

We believe that this is the trigger to that breakout we have been expecting having reported that Sterling markets had started to resemble a 'coiled' spring.

Some analysts are however warning against getting too excited about the data.

"Of course, we should treat August’s PMI reading with a pinch of salt, as it could well be an overreaction the other way," says Paul Hollingsworth at Capital Economics.

Hollingsworth does however note it was encouraging that the employment balance picked up above the 50.0 “no-change” level for the first time since December last year, and there were solid rises in both the overall new orders and export orders indices, suggesting that domestic demand has recovered somewhat while the lower pound has started to help exporters.

"Overall, then, the latest survey evidence supports our view that the economy is set for a period of slower growth, rather than a full-blown recession in the near term," says Collingsworth.

With regards to GBP's outlook, "Sterling had this week given no ground away despite Teresa May beginning to follow through on the referendum result and today’s PMI reading will see a continuation of buying as the Pound gets an infusion of confidence", says Richard de Meo, Managing Director of Foenix Partners.

Boris Schlossberg at BK Asset Management notes that GBP 'shorts' - ie bets against the currency - "are being squeezed mercilessly today with GBP/USD likely to test the 1.3300 level as the day proceeds."

Sean Lee at ForexTell notes that this strong move in GBP over the last 12 hours has been derived from a bonfire of the massive short positions held against Sterling, particularly in the real money community.

"Surely feeling some stress ahead of the NFP data. Nobody ever went broke booking profits and I suspect that we are seeing some positional adjustment in all of the GBP crosses," says Lee.

GBP/JPY has been the leader in this bounce, just as it was on the way down.

"Momentum is starting to pick up and another leg higher towards a previous congestion area around 140 would not surprise. With USD/JPY starting to run into heavy corporate offers, I expect most of the gains from here to come via GBP/USD," says Lee.

Latest Pound/Euro Exchange Rates

| Live: 1.1708▲ + 0.04%12 Month Best:1.1719 |

*Your Bank's Retail Rate

| 1.131 - 1.1357 |

**Independent Specialist | 1.1544 - 1.1591 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Crowing Commentators Continue to Under-Estimate UK Economic Resillience

Despite the strong showing, and Sterling's response, we note that a good portion of financial commentators continue to rubbish the data and push the line that this is a 'phony war' and a 'calm before the storm' that will hit... at some point.

Some suggest that when article 50 is actually triggered by the UK government will their eagerly-anticipated apocalypse arrive.

Ahead of the June 23rd referendum these commentators garnered much media attention with their warnings of a dire economic environment were the UK to vote for Brexit.

Their reputations were therefore staked on pre-referendum warnings of recessesion and UK economic decline.

Note that I am not referring to economists who typically maintain a sober response to incoming data and adjust accordingly, but rather the chattering classes at many of the City's financial publications and retail brokerages.

Their predictions and authoritative stances on the economy are hardly ever backed up by their own research or a balanced assessment of the wealth of professional economic research at their disposal.

The point is that this crowing may have aided markets it turning overly negative on Sterling based on personal opinion and now that these assumptions are being questioned by hard data, the currency is correcting higher.

RBS Maintain a Negative Forecast Profile for Sterling

While Sterling looks to grind higher it must be noted that many institutional analysts maintain the stance that this is just a bounce within a longer-term move lower.

We believe readers holding out for better exchange rates should be aware of this view.

Interestingly, strategists at RBS have confirmed they remain negative on Sterling’s prospects going forward, partly based on observations over the weakness in UK housing.

The call comes despite the strong showing by the Nationwide house price index at the end of August, as per our comment further down in this article.

In a recent note to clients RBS say mortgage approvals for house purchases were weaker in August and there are reports of reduced asking prices and weak activity.

“The sector is also slowing following a front loading of purchases ahead of changes to buy-to-let and stamp-duty,” say RBS.

RBS believe that the impact of the Brexit vote will be a slow-burn as a combination of weaker investment and real incomes growth on higher inflation is gradually felt.

Political noise may rise on Parliament’s return on September 5th. We may get more on the timing of Article 50 and priorities for fiscal policy at the Autumn Statement.

“We maintain our negative bias while spot is below 1.35 and expect resistance at 1.3372,” say RBS.

Barclays Forecast Update

Barclays meanwhile say they see scope for further modest GBP gains versus the EUR, amid better-than-expected UK economic data recently and stretched short GBP positioning.

However, “GBPUSD looks vulnerable to a correction lower should a strong US employment report solidify the prospects of a near-term Fed rate hike,” say strategists at the bank.

UK House Prices in Shock Rise

Sterling ended August on a positive footing after Nationwide reported their house price index rose 5.6% on an annualised basis in August, a result that stumped their own in-house economists.

This was well ahead of expectations for a rise of 4.8%.

“The pick up in price growth is somewhat at odds with signs that housing market activity has slowed in recent months. New buyer enquiries have softened as a result of the introduction of additional stamp duty on second homes in April and the uncertainty surrounding the EU referendum,” says Robert Gardner, Chief Economist at Nationwide.

Indeed, data from the Bank of England, released 24 hours earlier, shows the number of mortgages approved for house purchase fell to an eighteen-month low in July.

Gardner says the continued rise in house prices could well be due to a weakness in supply of new properties onto the market with the stock of properties for sale close to thirty-year lows.

Regardless, for Sterling traders, this is another case of gloomy Brexit expectations being trumped by more positive data.

Gfk Consumer Confidence data for August showed British shoppers in a posiitve mood regardless of their political predicament, after it came out at a better than expected -7, when analysts had expected -8 and the metric had shown -12 previously.

Sentiment toward the UK economy has certainly improved through the course of August, helped by a range of anecdotal and high frequency data that suggest the near-term hit to the UK economy may have been less than many feared.

These have centred on retail spending, tourism and manufacturing orders.