September brings with it two important pieces of UK economic data releases which could trigger a break-out in Pound Sterling with one analyst telling us the move will likely be lower.

GBP retains a positive bid against its G10 competitors ensuring the strong second-half to August is cemented.

With UK economic data having provided a windfall to Sterling of late, there will be nerves that this uptrend in GBP could be rudely undermined on Thursday when we receive the first hard data releases of the new month.

Manufacturing PMI is released on Thursday the 1st with markets anticipating a reading of 49.0 while on Friday Construction PMI is forecast at 46.1.

Expectations are low following the August releases so any beat of the forecast figures could well see GBP extend recent gains.

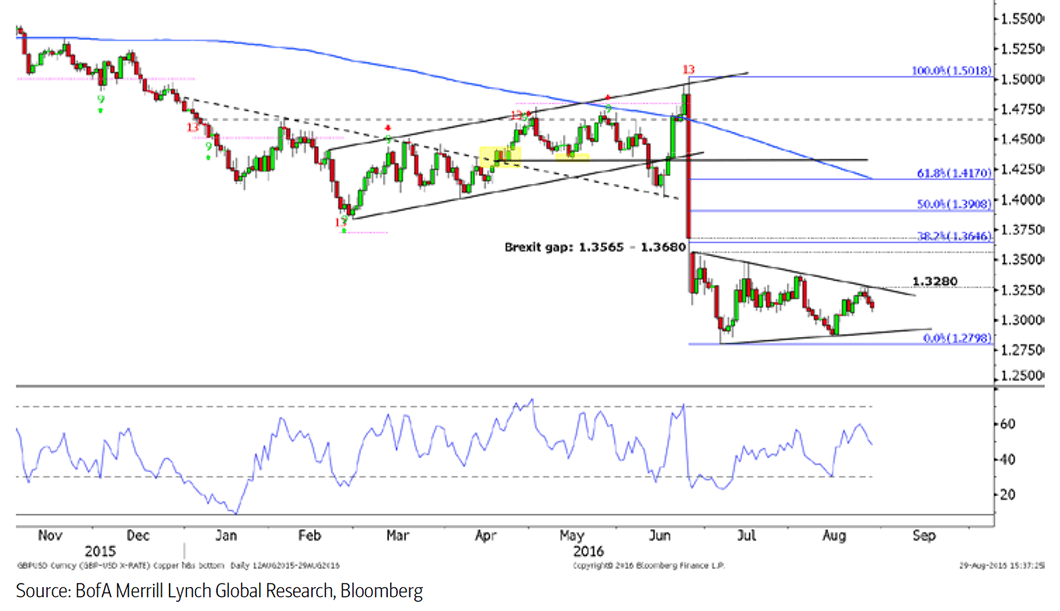

Beware the Winding Spring

If the data disappoints be warned that the UK currency could suffer some notable declines.

GBP/EUR and GBP/USD have been trading in increasingly narrow ranges with some likening the tightening to that of a winding spring.

Paul Ciana, a technical analyst with Bank of America Merrill Lynch Global Research reckons the spring will ultimately be triggered, and it could be to the downside:

"The post brexit trading range is consolidating tighter and tighter and a breakout could be looming. If cable were to close through 1.3280 it would provide a technical signal that the brexit gap may finally be filled.

"We remain trend bearish with our longer term view and would prefer to sell such a rally. In fact a break below the lower support line of about 1.29 would suggest a continuation of the downtrend.

Others are in agreement.

Shaun Osborne at Scotiabank says despite the relatively steady performance in spot, there is really little to cheer about on the charts for the GBP.

"At beast, the GBP is consolidating within a well-defined triangular pattern (see bottom chart); these are typically continuation patterns (bearish, in this case). We see strong resistance at 1.3250 still overall and would not get too excited about upside GBP prospects unless or until the market moved well above 1.35 at this point. We think the underlying risks continue to tilt lower," says Osborne.

Latest Pound/Euro Exchange Rates

| Live: 1.1699▼ -0.03%12 Month Best:1.1719 |

*Your Bank's Retail Rate

| 1.1301 - 1.1348 |

**Independent Specialist | 1.1535 - 1.1582 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

UK Data Remains Resillient

The final day of August saw the release of Nationwide housing price data that showed prices rose 5.6% on an annualised basis in August - well ahead of what ecnomists had forecast.

This suggests that markets and economists remain wrong-footed by the strong performance of the post-Brexit vote economy, naturally providing some uplift for Sterling.

Nevertheless, there are some contradictory readings on the matter as it was shown on the 30th August that mortgage approvals had hit an 18 month year low while all other major lending data from the Bank of England came in lower than forecast.

Mortgage approvals hit 60.91K in July, down from a previous 64.15K.

"Mortgage approval rates have dropped to an all-time low for two reasons: our unstable economy and people are scared of getting a mortgage," says Daniel Hegarty, CEO at Habito.

Interestingly, Hegarty believes we need to stop blaming Brexit for our housing crisis and "start looking at the archaic mortgage application process that’s preventing hard-working Britons from getting onto the property ladder."

Meanwhile lending to consumers read at 1.181B, well below the forecast 1.7B.

"July’s household borrowing figures highlighted that the housing market continued to cool following the EU referendum and there were signs that consumers’ appetite for debt took a bit of a hit as well. What’s more, with the economic outlook having deteriorated since the vote, we expect household borrowing to slow further over the coming quarters," says Scott Bowman at Capital Economics.

Euro Shrugs Off Employment and Eurozone Inflation Data Miss

Inflation in the Eurozone rose by only 0.2% mom and 0.8% yoy in August; disappointing analysts who had expected a 0.3% rise and 0.9% rise respectively.

Unemployment also remained unchanged in August defying the consensus of economists who had forecast it falling another basis point to 10.0%.

The results could make it marginally more likely that the ECB will opt to increase its already substantial package of stimulus measures at its September meeting.

When central banks raise stimulus it is generally seen as negative for the currency due to the increase in supply of money, as well the temporary downwards pressure put on rates.

The EUR/GBP exchange rate remained just below 1.1800 after the release, whilst the EUR/USD rate actually - counter-intuitively - rose five-hundredths of a cent following publication of the data.

Foreign Exchange advisors Foenix Partners’ senior sales trader, Alex Lydall, said the figures showed growth in the bloc was “stagnant.”

Although it was, “a little early to call for further action,” he argues Mario Draghi would be “taking a deep breath” to calm his nerves after the release and the worse than expected result would put the ECB’s policy outlook back on centre-stage after the recent hyper focus on the Fed.

German Unemployment Remains Unchanged

Also out from the euro-area was unemployment data from Germany in August, which came out at 6.1% in August, from 6.1% in July and the same expected.

The data shows no signs yet of damage from Brexit due to falling orders to the UK which is a key destination for German manufactured goods.

It indicates less of a short-term impact on Germany from Brexit than had been expected, and lowers the probability of the ECB pulling the trigger in September – a positive for the euro.

However, the single currency failed to react following the data as traders kept their ammunition for the more important inflation data released on shortly after.

Euro Under Pressure as Consumer Confidence Data Underwhelms

The Euro is under pressure against both the US Dollar and British Pound following the release of some pretty poor consumer confidence statistics out of the Eurozone.

Eurozone Consumer Confidence statistics for August showed a reading of -9, worse than the previous month’s -7.9 read.

“Although UK consumer confidence data surprised many by hitting a three-year high last week, the second post-Brexit figures for the eurozone indicate a strong sense of pessimism is still reverberating around the continent,” says Dennis de Jong, an analyst with UFX.com.

It was not just consumer confidence that took a knock as Economic Sentiment in the Business and Consumer Survey’s read at 103.5, down from 104.5 previously and below the 104.1 forecast.

This was the lowest reading since October 2013.

“ECB president Mario Draghi certainly has his hands full trying to inject growth into the eurozone and the picture is far from clear at present, with inflation remaining stubborn,” says de Jong.

The global uncertainty has been well and truly felt by consumers in Europe who may now be tempted to put plans for spending on hold until the situation improves.

“Draghi will be hopeful of just that in the weeks and months to come,” says de Jong.

Scotiabank, BNP Paribas Forecasting a Notably Weaker GBP/USD

On the institutional analysis front, analysts at Scotiabank have confirmed that they do not believe the British Pound’s period of weakness are over.

“We have revised down our forecast for the pound (GBP) in the wake of UK’s vote on EU membership (Brexit) to USD1.25 for year end,” says Scotiabank’s Shaun Osborne in a monthly foreign exchange strategy note to clients.

The GBP has stabilised following the initial downdraft in the exchange rate.

However, “additional BoE accommodation in response to the negative growth shock that appears to be manifesting itself in the UK economy and the heightened uncertainty regarding the broader UK economic outlook will depress the GBP further,” say forecasters.

Osborne cites previous patterns of trade following significant shocks (in 1992/93 after the GBP was ejected from the Exchange Rate Mechanism and 2008 as the UK entered a prolonged recession) as suggestive of a strong risk of a downside overshoot in the next few months.

“We think modest GBPUSD gains are an opportunity for sellers,” says Osborne.

Indeed, "short GBP/USD is my staple diet at the moment, but otherwise EUR/USD is just range-drifting, I haven’t had the fall in USD/JPY to buy so I’m just frustrated, and it will be the employment data on Friday that determine whether we can get broader G10 trends underway into Autumn, or just stay with the yield-hunt," says Kit Juckes at Societe Generale in a strategy brief to clients.

Meanwhile, a similar view is maintained at BNP Paribas who hold a similar year-end GBP/USD forecast.

BNP Paribas note UK data has surprised on the upside in recent weeks, failing to show the sharp slowing in activity many expected to see in the immediate aftermath of the June referendum.

However, PMI reports for July were consistently weak, suggesting trouble ahead, and we expect a similar message from this week’s August PMI reports, with the manufacturing PMI expected to hold below 50.0

"We remain broadly bearish on the GBP, anticipating further BOE easing in the months ahead and anticipating that direct investment and portfolio flows will be insufficient to easily fund the UK current account deficit in the near term," says FX strategy note from BNP.

Analysts continue to target Cable reaching 1.24.