Pound Sterling enjoys positive momentum against the Euro with our studies of the GBP/EUR's charts advocating for further gains but the ascent faces some key data events from both the Eurozone and UK in the coming week which could either accelerate, or stall, the fledgling rally.

- The Pound to Euro exchange rate is currently trading at 1.1746, 24 hour best: 1.1755

- The Pound to Dollar is trading at 1.3098, 24 hour best: 24 hour best: 1.3117

- The Euro to Pound Sterling exchange rate is at 0.8514, 24 hour best: 0.8527

In the immediate-term - the GBP/EUR remains on course for further upside according to our studies of the pair's charts.

This technical study will be confirmed, or invalidated as the week progresses and Eurozone and UK data releases impact on trade.

Nevertheless, we see the pair is in a short-term up-trend, and although it is pulling back today, the overall impetus remains to the upside.

The move lower visible on the four-hour chart below appears to be completing an a-b-c correction from off the August 24 highs, and is still commensurate with our forecast that the pair will extend its short-term up-trend - once the correction is complete, that is.

As a result, we now see the pair poised to move higher, with a break above the 1.1783 Aug 24 highs confirming more upside to a target at 1.1845 where the monthly pivot is situated and likely to prove a tough obstacle to further gains.

Monthly pivots are levels of support and resistence where the exchange rate can stall or reverse direction; they are used by professional traders to gauge the trend and launch counter-trend trading positions.

Euro Faces a Busy Day of Data Releases

There remains a steady flow of data on tap for the Euro this week.

The shared currency could take a cue from German employment data and Eurozone CPI data on Wednesday the 30th of August.

German unemloyment is released at 08:55 BST and is forecast to have fallen by a further 5K souls, a deceleration from the previous month's 7K.

As can be seen by our discussion on consumer confidence below, the German economy will need a good showing this month if the ECB are to be convinced no further monerary policy moves are required.

Then the big data release of the week comes at 10:00 BST in the form of Eurozone inflation.

Draghi and his team at the ECB are desperate to see some price growth which would confirm their policies are having an impact on the Eurozone.

Economists are forecasting a reading of 0.3%, up from last month's 0.2%. Anything less is likely to keep the Euro under pressure.

Latest Pound/Euro Exchange Rates

| Live: 1.1702▼ -0.01%12 Month Best:1.1719 |

*Your Bank's Retail Rate

| 1.1304 - 1.1351 |

**Independent Specialist | 1.1538 - 1.1585 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

UK Data Could Prompt Notable Moves in Sterling

After two weeks of technically-inspired trading, data is back in focus over the course of the coming week.

Traders will get a good idea as to whether the better-than-forecast run of economic releases seen through August will continue to allow the Pound to extend the relief-rally that has seen it rise from a low of 1.1461 in early-August to the previous week's best at 1.1784.

The release of Manufacturing PMI data for August on Thursday, and Construction PMI on Friday, will be in focus.

We could well see investors selling Sterling as they adopt a more cautious stance ahead of the releases ensuring the currency retains a soft bias over coming days.

The equivalen July PMI data showed a steep decline into contraction territory for both sectors which sparked fears about the severity of the impact of Brexit, and the data for August is expected by many to continue the trend.

"The August Manufacturing PMI will show whether activity deteriorated further or recovered after the slump in July, which followed the Brexit vote in June. We expect the PMI to rise to 49.0 from July’s 48.2, which was the lowest since the financial crisis in early 2009," says Nordea Bank’s Bo Jackobsen.

On Friday, Construction PMI’s are released with markets looking for further contraction in the sector with a reading of 46.1 expected.

Next week on Monday Services PMI will be released and this will be a big number to watch as the services sector accounts for over 80% of UK activity.

"Of late, the first UK hard eco data from the post-Brexit area were not too bad. At the same time, Sterling already discounte some quite negative news. We keep a cautious bias on Sterling longer-term. Short term, the decline of sterling is taking a breather. Even if a further technical rebound is possible short term," says Piet Lammens, an analyst with KBC Markets in Brussels.

British Pound's Short Squeeze Higher Could Extend Further

Can that technical rebound, mentioned by Lammens, extend?

While data will certainly pose a risk to Sterling over coming days, we are aware that the market remains highly sensitive to investor positioning.

One of the reasons the currency's slump has stalled is because markets are all too heavily invested in betting on GBP negativity.

In such scenarios the required fresh entrants into the market, needed to keep pushing the price lower, dry up.

In fact, any counter move can be a quite notable in that large numbers are forced out of the markets by such a move, in turn buying Sterling to close their positions.

This technical phenomenon is known as a short squeeze.

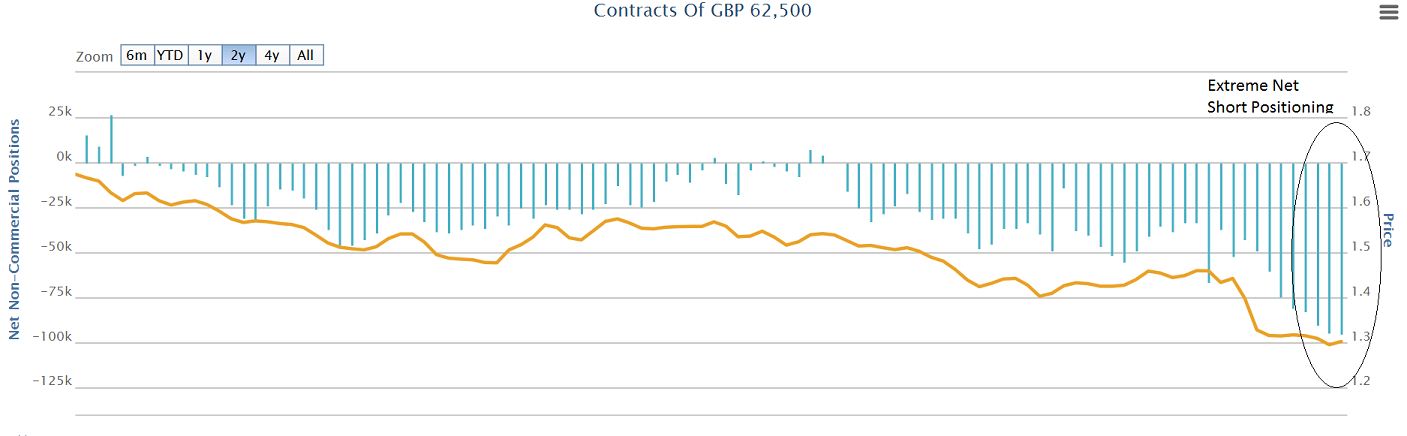

The commitment of trader’s report (COT) shows how large speculators such as hedge funds are positioned, is showing an extreme glut of short positions on Sterling – short positions are those which make money if the asset loses value.

Many analysts will note that the extreme downside positioning is actually a sign the pair could be overextended and due a correction higher (see picture below).

Nevertheless, it is difficult to time these things, and the extreme short positioning may persist for a while longer still.

US Dollar in Demand

The US Dollar recovery remains the main point of focus for foreign exchange markets at present as the Greenback successfully extends its Jackson Hole-inspired gains against most competitors as markets become alive to the fact that an interest rate rise could be delivered as early as September.

Sparking the rally was Fed Vice Chairman Fischer's comments that a September rate rise was possible.

However we are told to expect some of this USD strength to be pared back.

"Investors are not taking Fed Vice Chair Stanley Fischer's comments about a September rate hike seriously as we can see through the decline in Treasury yields and rise in stocks today. If investors believed in the serious risk of two rate hikes this year, yields would be up and stocks would be down," says Kathy Lien at BK Asset Management.

Fed fund futures are now pricing a 36% chance of a September hike and a 61% chance of the next rate hike coming in December.

Lien believes that while Janet Yellen and Stanley Fischer may have made their hawkish bias very clear at Jackson Hole but market participants are waiting for evidence that a rate hike is warranted.