- Bank of England leaves interest rates unchanged

- All nine MPC members back decision

- Sees stronger-than-expected pay growth developing

- Pound Sterling advances on Dollar, defends gains against Euro

© lazyllama, Adobe Stock

The Bank of England left interest rates unchanged at 0.75% at their September policy meeting while communicating that third-quarter consumption and pay growth might have been stronger than originally envisioned.

This suggests the economy is performing consistent with the need for further interest rate rises in the future.

This headline takeaway proves positive for the British Pound which traded higher against the US Dollar following the announcement, breaking the 1.31 barrier in the process.

Against the Euro, Sterling holds its September advances, despite the European Central Bank giving the single-currency its own boost mere minutes after the Bank of England decision.

According to the Bank's statement:

"Annual earnings growth including bonuses had been just over 2½%. Less volatile regular pay measures had grown by around 3% on a year earlier, a little stronger than had been expected in the August Report. Evidence from pay settlements and surveys was consistent with some further rise in earnings growth."

As such, the Bank believes the need for an ongoing tightening of monetary policy is needed.

For Sterling, an acceleration in the process of tightening policy - i.e. raising rates - is seen as positive.

The decision to hold rates unchanged is an uncontroversial outcome given the bank raised interest rates for only the second time since the financial crisis on August 02 and needs more time to assess incoming data and Brexit developments before moving again.

The vote for keeping policy steady was 9-0, as expected.

With regards to Brexit, the Bank sees greater uncertainty since August; an observation that might be taking some of the shine off the views concerning pay growth, and this should keep Sterling in check.

"Mixed BoE policy statement here, greater Brexit uncertainty versus 3Q GDP growth upgrade. Also reiteration that future rate hikes will be gradual. We shouldn't see any major independent GBP moves today," says foreign exchange strategist Viraj Patel with ING Bank N.V.

The Bank also notes greater global risks relating to trade and emerging market stresses; something that might convince markets policy makers are in no mood to hurry forward their next interest rate.

Analyst Ruth Gregory with Capital Economics say she thinks the MPC will tread cautiously until Brexit uncertainty has been resolved.

The Capital Economics team hold a baseline assumption that a Brexit deal will be struck at the eleventh hour will probably prevent the MPC from lifting rates again until next year.

"Provided a deal is agreed, though, and the economy holds up well as we expect, then our sense is still that rates will probably rise two times in 2019 and a further two times in 2020, pushing Bank Rate up to 1.75% by the end of 2020. That would be above the market expectation for just two hikes over the next three years – but still consistent with the MPC’s guidance of a “gradual and limited” rise," says Gregory.

Concerning the currency outlook, it is understandable that the Pound has more-or-less shrugged its shoulders at the outcome.

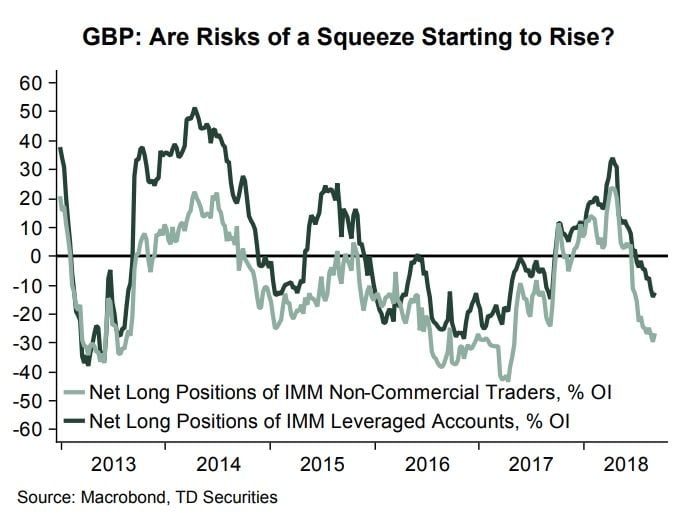

"As expected, the September MPC meeting did not provide a large directional push for the GBP. Political risks remain the main focus and these are building to another near-term peak. This leaves us cautious and reluctant to embrace a bullish view on Sterling, but we note the GBP looks increasingly vulnerable to a short-squeeze," says James Rossiter, Senior Global Strategist with TD Securities.

A 'short squeeze' is a technical phenomenon where a currency reverses trend simply because the trend had become over-subscribed. Bets against Sterling have risen in popularity to the extent there are fewer and fewer new market entrants joining the trade to push the trend.

Any counter-trend news therefore sees traders bail out of the trade which of course requires the buying of Sterling, sending the currency in the opposite direction.

Because a short-squeeze is technical in nature and not based on fundamentals, it ultimately dies allowing the prevailing broader trend to establish itself. Hence, the danger of Sterling turning lower again remains.

Advertisement:

Can the Pound stay at these levels? Lock in the best levels we have seen in weeks and potentially get up to 5% more foreign exchange for international payments than on offer at your bank by using a specialist provider to get closer to the real market rate. Learn more here.

Analyst Predictions Made Ahead of the Decision...

Lee Hardman, currency analyst, MUFG

"The strength of recent economic releases is notable given the intensification of uncertainties surrounding Brexit. For some time now there has been plenty of anecdotal evidence of tightening labour markets in the UK and upward pressures on wages emerging. The ONS jobs data yesterday revealed pretty compelling evidence of this now coming through in the hard data.

"We believe the rates market is under-priced for what looks to be emerging signs of wage inflation. Just over one rate hike is priced for 2019. If a Brexit deal is imminent, the rates and FX move is likely to be considerable."

Bruce Kasman, head of economic research, J.P. Morgan

"After the unanimous decision to raise rates in August we expect unanimity in holding rates unchanged at this meeting. The committee likely will note the recent decline in Sterling as an offset to weaker signs on global growth. There may also be some discussion of how the MPC could respond to various Brexit scenarios."

Advertisement:

Can the Pound stay at these levels? Lock in the best levels we have seen in weeks and potentially get up to 5% more foreign exchange for international payments than on offer at your bank by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

James Rossiter, senior strategist, TD Securities

"We expect a 9-0 MPC vote to keep policy on hold Thursday and retain a cautious tone on the pace of future tightening. Macro data continues to support the August projections. Once political uncertainty has dissipated by March 2019, the BoE should deliver two hikes in 2019.

"Our base case implies modest downward pressure on GBP after a decent run in recent weeks. A largely unchanged outcome suggests sterling will remain contained within recent ranges as investors remain focused on larger concerns elsewhere.

"Building downside risks to growth might get a nod. One-off factors helped to maintain 18Q2 growth at a slightly faster-than-trend rate, but as these effects dissipate, it's not clear where core 18Q3 growth will come from. The political noise and uncertainty in July has raised risks a disorderly Brexit, and households and firms have noticed.

"Sterling's depreciation has been muted, with the effective exchange rate less than 1% lower than assumed in the August forecast. Oil prices are slightly stronger, but on net these two factors don't suggest any major risks to the BoE's forecasts."

Stephen Gallo, European head of strategy, BMO Capital Markets

"On September 4th, Mark Carney told UK lawmakers that “more rate hikes would be needed” if the economy stays on its current trajectory. This is the most reliable and useful guidance that financial markets can expect to receive from the BoE at this stage.

"The MPC is on a gradual tightening path, but the timing of the next rate hike of the cycle is partly dependent on two crucial issues: 1) the outcome of the UK/EU Brexit negotiations and 2) the path of the GBP.

"Our baseline assumption is that discussions on the Withdrawal Agreement will carry over into 2019 (as will the discussions concerning the future UK/EU relationship). Therefore, “cliff edge Brexit” risks will prevent the MPC from lifting rates before May 2019.

"Although a UK/EU Withdrawal Agreement by end-March 2019 is still theoretically possible, we anticipate a further increase in “cliff edge Brexit” risks before that deal comes to fruition. As such, our preference is to continue playing EUR/GBP from the long side for now."

Playing EUR/GBP from the 'long side' is a strategy of buying Euros and selling the Pound on any strength.

Viraj Patel, currency strategist, ING Group

"The Bank of England raised interest rates in August, but we suspect this will be the last such rise for quite some time. Uncertainty surrounding Brexit is ramping up, and talk of the possibility of a 'no deal' scenario increases.

"Admittedly, we think the probability of a 'no deal' is still relatively low. However, it all comes down to a crunch vote in the UK Parliament in early 2019 which means uncertainty is only likely to rise as we head into the winter and could begin to test business and consumer sentiment even further.

"This makes it very unlikely that the Bank will hike again before March 2019, and we think there are three scenarios for what happens after that. Firstly, if the parliamentary process in early 2019 is relatively smooth - in other words, MPs approve the deal with relatively little fuss - then there is a possibility of a rate hike in May next year.

"However, if the process is more fractious and lawmakers demand concessions before approving the withdrawal agreement, this raises the possibility that we won't know for sure if 'no deal' will be averted until the last minute. Even if a solution is eventually found, confidence is likely to take much more of a hit in the first quarter and growth momentum would likely slow. In this case, we suspect the Bank would keep rates on hold for longer.

"In the case of 'no deal', the economic impact would be significant and any tightening plans would be taken off the table, and in fact, we would likely see the probability of a rate cut increase."

Knut Magnussen, economist, DNB Markets

"The macro picture has been relatively stable since the previous meeting in early August. Our macro score, which fell into negative territory in May, recovered during the summer and returned to positive territory in August. The rebound was entirely due to household indicators. Retail sales picked up strongly, and both the housing and the labour marked improved as well."

"In August, the Bank Rate was lifted to 0.75%. The market does not expect another hike until well into next year. Our forecasts indicate a hike at the November meeting in 2019. We anticipate that the present guidance; i.e. that hikes will continue to be at a gradual pace and to a limited extent, will be maintained at this meeting."

Advertisement

Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here