The EUR/USD exchange rate has been rising steadily on combination of the improving economic outlook for the Eurozone and a reigning back of rampant interest rate expectations in the US.

The US Dollar has seen some weakness over recent days and the Dollar index - a measure of overall Dollar performance - has fallen to its lowest level since the 9th February.

The EUR/USD pair has now risen to reach a key level at the current range highs, at just shy of 1.0800, as markets see little chance of the US Federal Reserve raising rates more than three times in 2017.

At the time of writing EUR/USD is quoted at 1.0762.

My studies suggest that over the next few days, the exchange is likely to test the trendline capping the range highs and could attempt to break above.

For confirmation of such a break higher, we would want to first see a move above the 1.0810 level - so set an alert for this level.

This would signify a break higher and the continuation of the uptrend to a target at 1.0900 close to where the 200-day moving average is situated.

The MACD momentum indicator has just moved above its zero-line indicating a change in the short-term trend from down to up and supporting the possibility of a breakout higher.

"For now, the long-term trend continues to favour the dollar, but we are seeing weakness in the short-term. The dollar also fell against the Euro, which may be set to move higher to test strong resistance at 1.09," says analyst Phil Seaton at LS Trader - a firm that speclialises in observing and profiting on trends in the foreign exchange market.

Data, Events to Watch for the Euro this Week

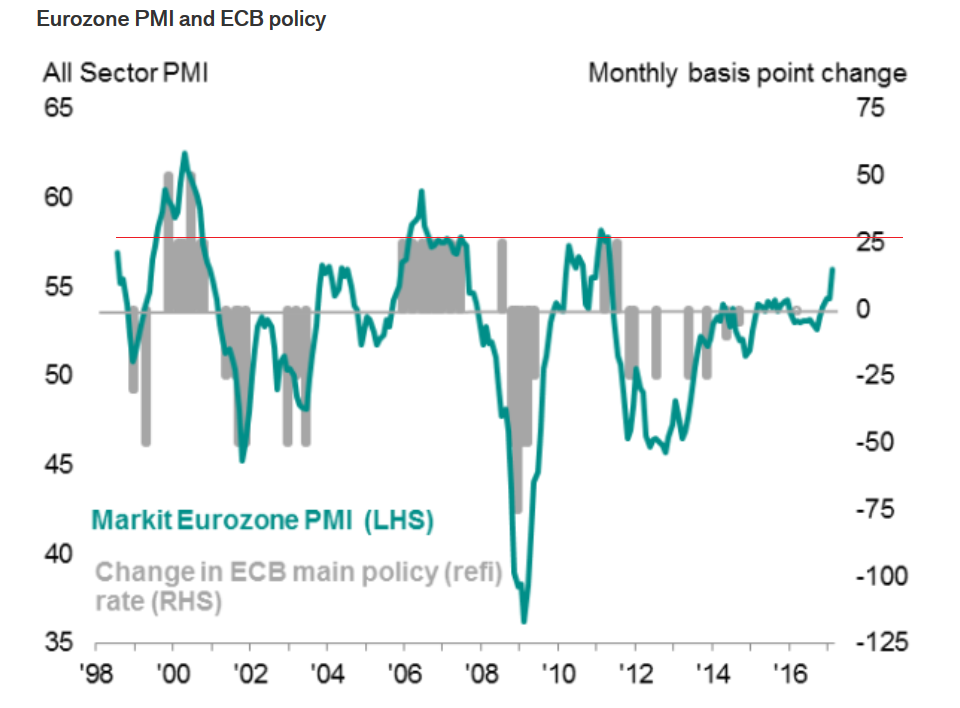

The week ahead for the Euro will be dominated by survey data, including Manufacturing and Services purchasing manager surveys or PMIs as they are known, which will be released at 9.00 GMT on Friday, March 24.

Recent surveys have shown such a marked improvement in responses that the indices are now almost at a level where historically the ECB tightened monetary policy by either raising interest rates or winding down direct stimulus efforts via quantitative easing, according to survey managers Markit.

A tightening of monetary policy would be an all-out positive for the Euro as it implies a restriction of supply of the currency into the global economy.

This explains the comments from the head of the Austrian central bank Ewald Nowotny last week in which he suggested the ECB’s deposit rate should be raised.

Market professionals should keep an eye out for other ECB officials’ comments this week as they may move markets if they too call for a rise in rates.

More Cheap Lending to Keep Rates Low

Data showing pick-up of the European Central Bank’s Targeted Long-term Refinancing Operations (TLTRO’s), which provide discounted 4-year loans to banks could impact on the Euro in the week ahead. Especially if they show strong demand as this may have a, “dampening effect on the Euro area’s interest rate landscape,” according to Raiffeisen Research’s Veronika Lammer.

Real yields – some would say a more accurate predictor of currencies - are already very low in the Euro-area, so a dampening of rates from excess bank liquidity is not going to help.

Allotment results will be published at 10.30 GMT on Thursday, March 23.

French Election Risks

Political risk has subsided somewhat since the failure of the anti-euro PVV party to win in the Netherlands but analysts will still be keeping an eye on results from polls for the French Presidential election on Sunday, April 23.

As we reflected here, the Dutch election outcome opens the door to a more assertive outlook for the Euro.

At present centrist candidate Macron is tied with far-right candidate Le Pen for the first-round of voting.

Should they both go to the second round then there is a strong likelihood that Macron will win.

However, as we note here there is still a chance for Le Pen to win - and if this does happen then the Euro will come under immense pressure.

Data, Events to Watch for the Dollar

Durable Goods Orders on Friday, March 24 are the focus of the week for the Dollar, although they are unlikely to cause much volatility according to Raiffeisen Research, who see a rise in orders for aircraft from Boeing being cancelled out by a fall in general capital goods buying.

Raiffeisen Bank’s Veronika Lammer sees Orders rising by 0.5% in February from 2.0% previously versus 1.1% expected.

Housing data, out at 14.00 GMT on Wednesday, March 22, constitutes the other main release this week, with Lammer expecting a slowdown.

“The available indications suggest a noticeable fall of around 5.0% since January (in Existing Home Sales),” says Lammer who adds:

“New Home Sales should also have shown a declining development, we assume a month-on-month minus of 1.0 to 2.0%.”

On the Dollar’s unintuitive reaction to the Fed’s March meeting rate hike, Lammer is sceptical, saying the market got it wrong and the Fed is likely to raise interest rates more not less aggressively in the medium term, thus suggesting Dollar weakness could extend.