Image © Adobe Images

The U.S. Dollar is not heading for a sustained decline, according to DNB Carnegie, which says the de-dollarisation thesis that dominated currency debate last year has failed the test of the data.

"We remain comfortable with our view that, over the short to medium term, the case for de-dollarisation is simply not strong enough to trigger a sustained weakening of the dollar," says the bank in a new research note.

The finding follows a post-mortem of the fears that stalked the currency through last year: trade barriers, confidence in US institutions, Federal Reserve independence, rising government debt and the prospect of taxes on foreign ownership of US assets.

On each count, DNB Carnegie finds the worst-case scenario has not materialised.

The Fears That Faded

Concerns over political pressure on the Federal Reserve have eased significantly, with regional Fed presidents having their terms extended and the transition to a new Fed Chair proving orderly.

"Political influence over the Fed appears far more difficult than feared a year ago," says DNB Carnegie, noting that Miran stepped aside once Powell remained in place and that Warsh, while wanting reform, has so far played by the rules.

The courts have meanwhile repeatedly ruled against the current administration's policy initiatives, suggesting to the bank that US institutions have proved more resilient to political pressure than many expected.

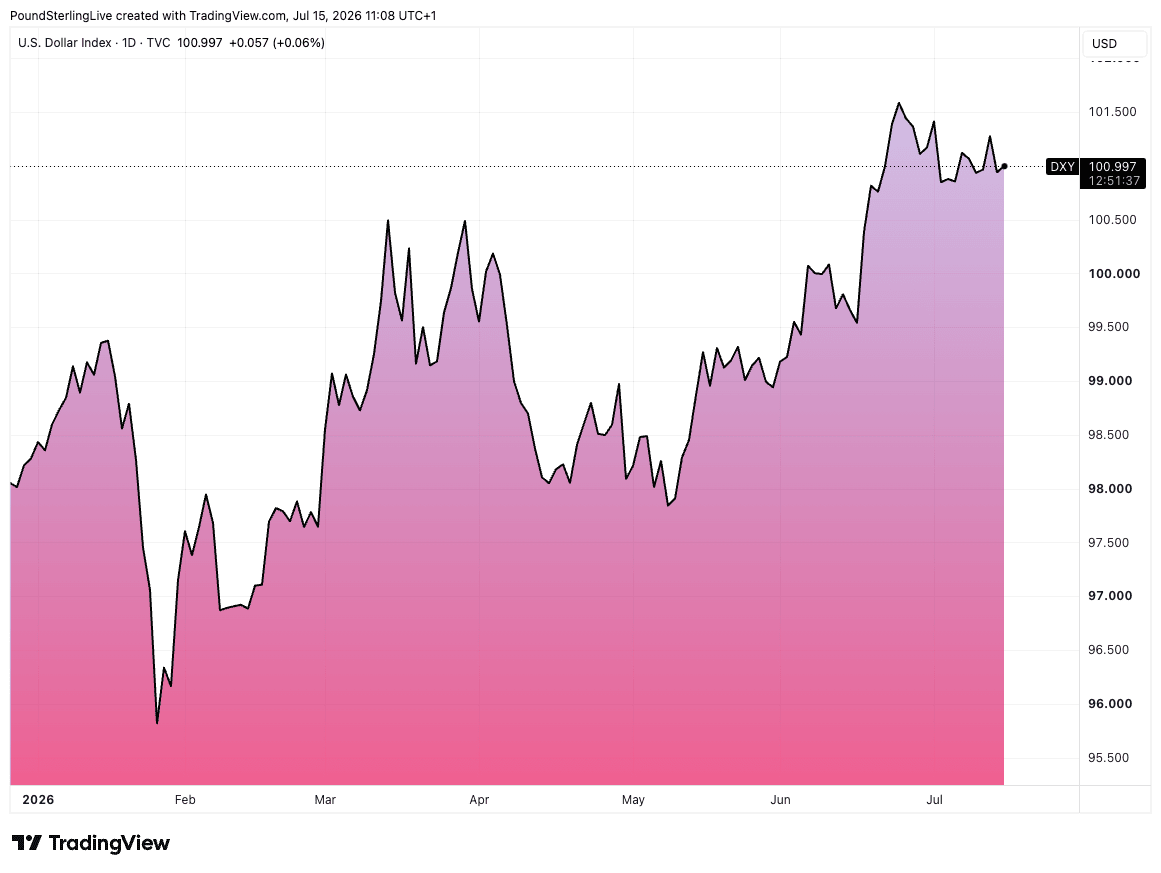

Above: The dollar index.

The Money Never Left

The hard flow data tell the same story.

Foreign official holdings of US Treasuries have declined, but foreign private investors have more than compensated, while overseas money continues to flow into US equities.

April last year, immediately after Liberation Day, remains the only month in which foreigners were net sellers of US securities.

"There is still little evidence of meaningful capital repatriation," says DNB Carnegie.

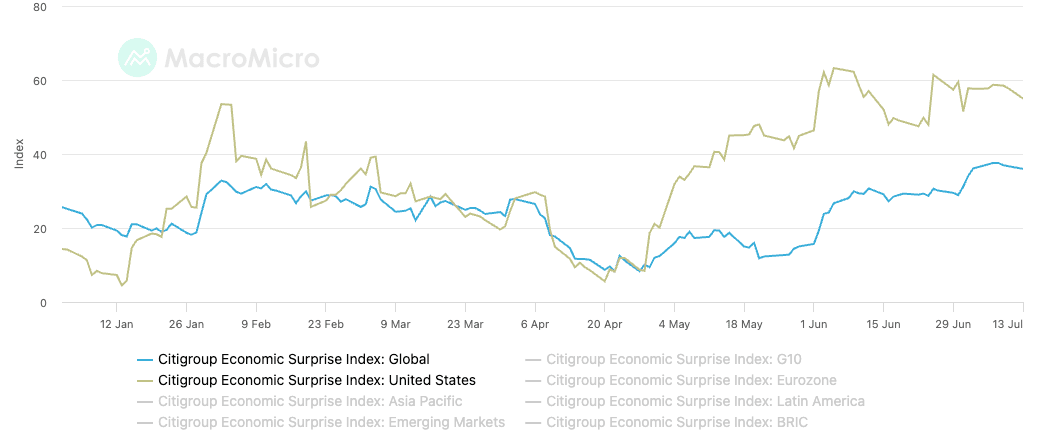

Above: The U.S. economy has started outperforming again. U.S.exceptionalism is back.

The bank identifies three durable supports for the currency: the dominant US weight in global equity and bond indices amid strong demand for passive products, an attractive sector mix with a large technology component, and an economy delivering robust productivity growth.

Nor is there much sign of international investors raising currency hedges on their US holdings, a flow that would mechanically weigh on the Dollar; where hedge ratios have risen, the bank says this largely reflects valuation effects after the post-Liberation Day equity selloff.

The assessment lands on the supportive side of a live debate, joining research arguing the AI boom offers the Dollar a structural bid while others contend low hedge ratios leave the currency exposed to any loss of confidence.

What Could Still Bite

DNB Carnegie concedes the political risk has not been retired.

No serious proposals have emerged to tax foreign ownership of US assets, and the bank reckons such measures would become considerably harder to pass if, as polls suggest, Republicans lose control of at least one chamber of Congress in this autumn's midterm elections.

The Dollar's traditional safe-haven behaviour, strengthening when equities and bonds fall, has also generally reasserted itself after a period of instability.

But the bank is not calling for calm seas.

"We doubt the White House has delivered its last surprise, so periods of volatility and temporary dollar weakness cannot be ruled out," says DNB Carnegie.

Free Report · Worldwide Currencies

Where Next for the Pound? Get the Quarterly Forecast Report

Consensus exchange rate projections from eleven global banking partners, including Barclays, JP Morgan and Citigroup: point forecasts, highs and lows for each quarter through to early 2027.

Delivered by email. Produced by Worldwide Currencies; for information purposes only and not investment or financial advice.