Image © European Commission Audiovisual Services

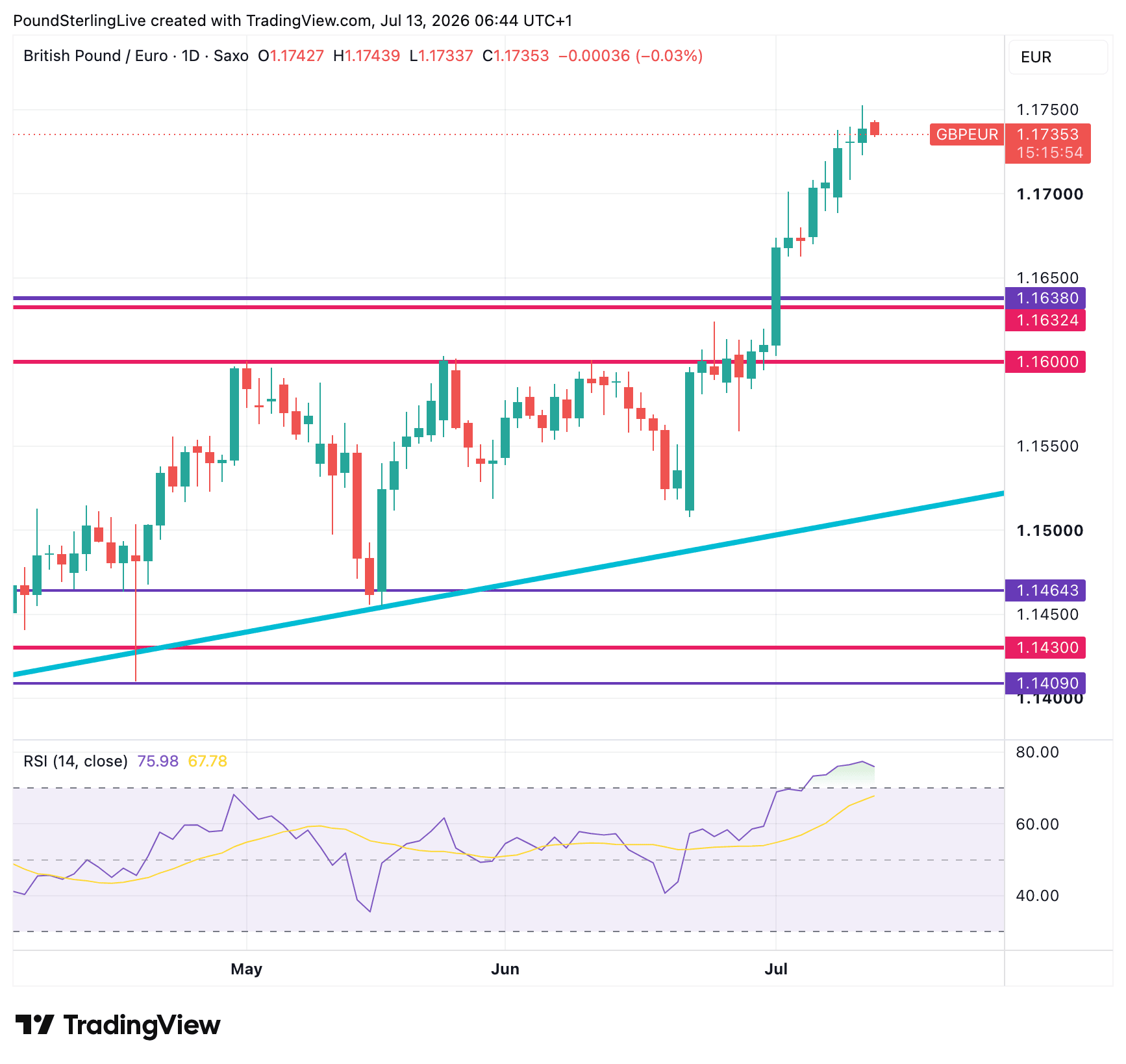

Pound sterling is currently buying more euros than the institutional consensus expects it to over the coming quarters.

New quarterly forecasts compiled by Worldwide Currencies, drawing on projections from eleven banking institutions including Barclays, JP Morgan, Citigroup and Crédit Agricole, place the middle ground of pound-to-euro expectations below the current spot rate.

The pair is expected to remain broadly range-bound through to early 2027, but the centre of gravity across the forecast horizon sits beneath prevailing market levels, currently at 1.1730.

For readers with upcoming euro payment requirements, the implication is straightforward: the rate on offer today is better than the rate most institutions expect to be available later in the year.

The spread of views is nevertheless wide, with some banks seeing Sterling holding near the top of its recent range against the single currency, while at least one forecaster anticipates a decline running to several cents.

The precise quarter-by-quarter projections, covering Q3 2026, Q4 2026 and Q1 2027 across six major currency pairs, are contained in the full report: readers can request a copy of the quarterly forecast report here.

Political Risk: Overpriced or Underpriced?

The forecast round lands at a delicate moment for Sterling, with the UK's political transition still working its way through market pricing.

"The GBP could also remain a pressure valve for anxious market participants that fret about the negative consequences from the change at the helm of the Labour Party and the UK government," says Valentin Marinov, Head of FX Strategy at Crédit Agricole.

Marinov adds the currency could prove vulnerable if persistent stagflation risks fuel concerns about the UK economic and fiscal outlook.

A Strong Rally

Despite perennial concerns about Britain's political landscape, GBP/EUR has steadily advanced since November last year.

A breakout through the important 1.16 resistance zone on July 01 triggered a move to the highest levels in a year, suggesting politics has faded as a concern.

"UK political risk remains persistently over-priced by markets, while the economy's underlying resilience is consistently under-appreciated," says Savvas Savouri at QuantMetriks.

Forward-looking macroeconomic expectations that embed political pessimism tend to understate UK real activity and the "true" value of Sterling, according to Savouri.

The Bad News May Already Be in the Price

Crédit Agricole's Marinov reckons much of the pessimism is already reflected in the exchange rate, particularly against the euro.

"We believe however, that some negatives are already priced into the GBP especially vs the EUR, given that the Eurozone would have to deal with the consequences from the negative oil supply shock in the wake of the Iran war as well," he says.

What Decides It From Here

Despite recent constructive price action, headwinds remain.

The Burnham era will be characterised by significant spending commitments running into severely constrained finances.

The report's compilers note that central bank policy, inflation and geopolitical developments are also expected to remain the principal drivers of currency markets throughout the forecast period.

With institutional expectations sitting below the market, the sense is that the recent rally will be pared before year-end.