Image © Adobe Images

The week ahead forecast finds the balance of probabilities favours further gains towards 1.1750, but overbought conditions suggest the recent rally has overextended.

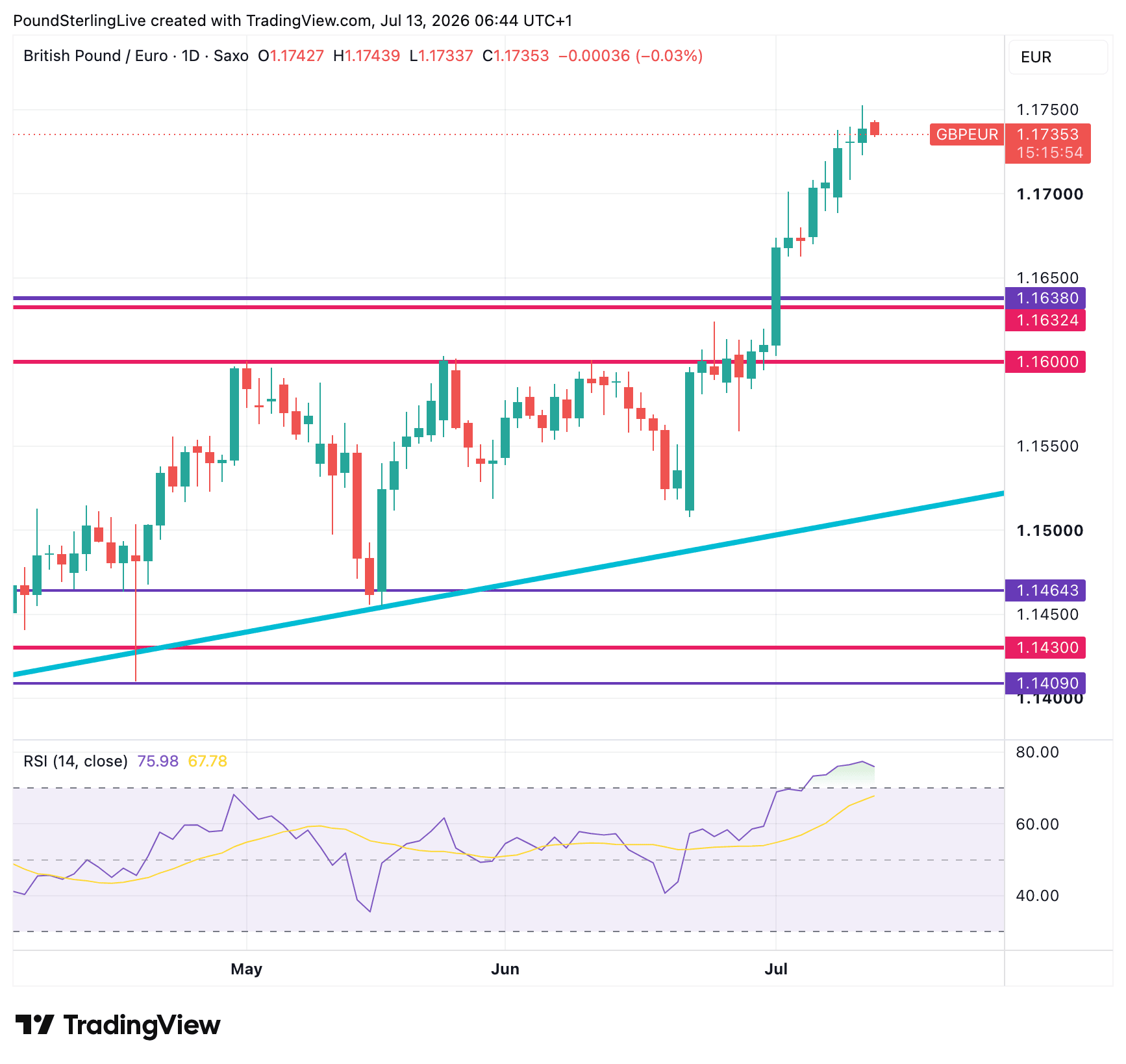

Following a solid run of gains, the pound-to-euro exchange rate reached its highest level since June 2025 on Friday when it hit 1.1752, and it trades close to that peak at 1.1736 at the time of writing Monday.

On the whole, the short-term technical outlook remains firmly bullish following the decisive breakout through 1.1600 and 1.1632/1.1638, which has been accompanied by strong upside momentum.

As a result the week ahead forecast finds the balance of probabilities favours further gains towards 1.1750 and potentially 1.1800, provided the pair can hold above its recent breakout levels.

The principal risk to the bullish outlook is not a reversal in trend but the increasingly overbought RSI, which suggests the rally may be due a pause or shallow pullback.

Any retreat that finds support around 1.1632-1.1638 would be consistent with a healthy consolidation and would strengthen the case for a subsequent move higher:

Only a sustained move back below 1.1600 would begin to cast doubt on the current bullish technical structure.

The rally has become increasingly stretched, with RSI approaching 76, placing the pair firmly in overbought territory and raising the prospect of a period of consolidation before the next leg higher.

For an RSI to mean-revert and correct from overbought it must track lower and dip below 70, which can happen if the spot exchange rate simply moves higher, or pulls lower.

The key question for the week ahead is whether GBP/EUR can consolidate above former resistance. Holding above the 1.1632-1.1638 breakout zone would confirm that resistance has transitioned into support and keep the broader uptrend intact.

While momentum remains positive, the overbought RSI suggests fresh buying may become more selective in the near term.

What Matters for the Pound This Week?

The only serious domestic data event for the pound in the coming week is the release of monthly GDP numbers on Thursday.

UK GDP is likely to have rebounded modestly in May, with output forecast to rise by 0.1%

m/m following April's 0.1% drop.

The recovery is expected to be driven by services output, supported by stronger consumer-facing activity after April’s weakness.

Economists say the unusually warm and dry conditions in May likely provided a boost to retail, leisure and hospitality activity.

Industrial and manufacturing output are expected to have fallen on a combination of falling mining output and weaker demand.

The pound is unlikely to be too bothered by the data, although a sizeable beat or undershoot against expectations could be felt on the day if it impacts Bank of England pricing.

Middle East Tensions Providing Additional Support

The domestic calendar is relatively light this week, suggesting the pound-euro pair will likely take its guidance from global sentiment.

Currency markets are currently highly attuned to interest rate differentials, meaning those currencies with higher rates (bond yields) tend to outperform.

The pound enjoys one of the highest real yields in the developed market space, and that looks to be underpinning its recent run of strength against all ex-USD opponents.

The resumption of tensions in the Middle East underpins this: oil prices have risen in response and traders are betting that will delay any future rate cuts at the Bank of England. That in turn underpins the pound's existing yield advantage.

The pound rose sharply when the conflict erupted in March and oil prices rose. With the U.S. and Iran engaged in ongoing military reprisals, and the Strait of Hormuz allegedly closed to traffic, the conflict could be set to underpin the pound's recent gains against the euro.