Image © Pound Sterling Live

Pound Sterling's rate story is a bit of a win-win suggests new Bank of New York analysis.

The British pound is outperforming; it's the second-best performer for the past month, and interest rates are certainly playing a significant part in helping.

The UK's relative rate story is supportive, with higher yields relative to elsewhere attracting international investor funds and creating a supportive currency flow.

On this basis, what's the biggest risk to sterling outperformance? That those flows fade as investors look to a Bank of England that is less inclined to raise rates, or even start cutting rates.

But what if that mechanism doesn't play out, and what if fading rate hike bets actually play positively for sterling?

That's something we should consider, says a new analysis from Bank of New York (BNY).

"Conventional relationships between monetary policy and currency performance are breaking down, especially in Europe," says Geoff Yu, Senior EMEA Market Strategist at BNY.

The Pound, Euro and Bad Rate Hikes

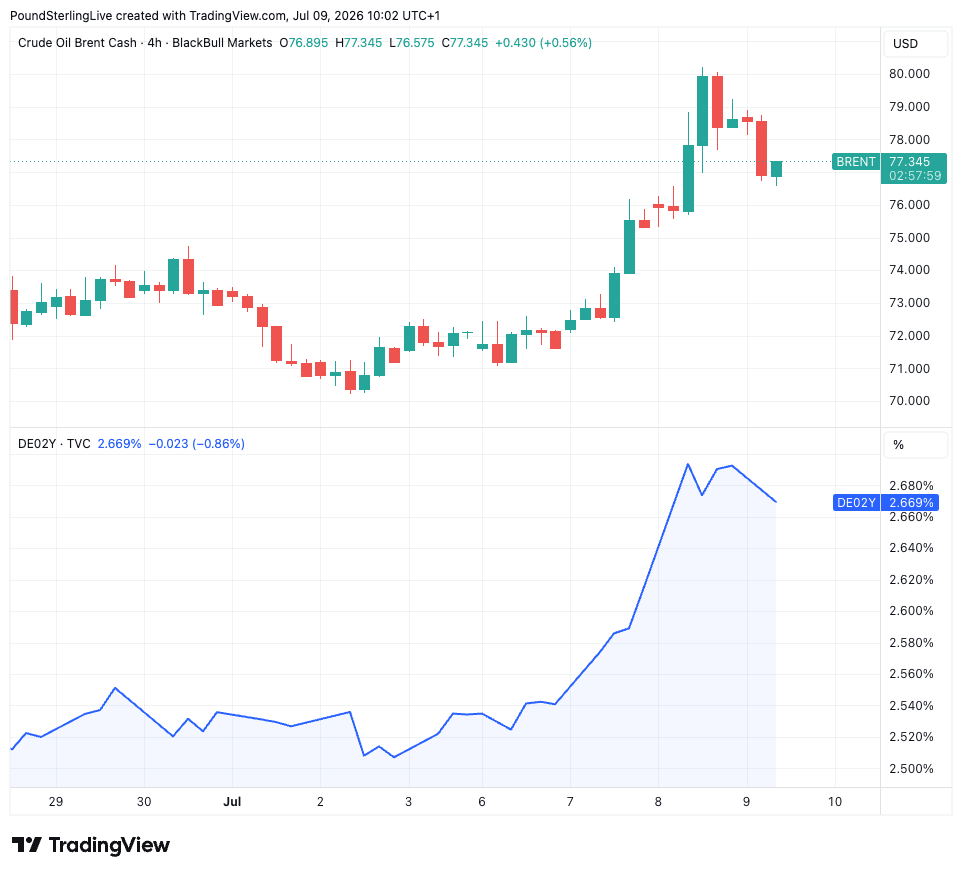

Bets for rate hikes in the Eurozone have risen again since the U.S. and Iran started trading blows again in the Middle East and the reclosure of the Strait of Hormuz sends oil and gas prices higher.

That's a reflection of a market reckoning the European Central Bank (ECB) will raise rates in response to the resultant inflation.

Indeed, as of now, the market is back to pricing in two 25bp hikes by year-end. "Hawkish European Central Bank (ECB) members are sending clear policy warnings around the fragility of the U.S.–Iran ceasefire and supply risks through the Strait of Hormuz," says Yu.

Above: Rising oil prices pull German bond yields higher via the ECB rates expectation channel.

Such a repricing would typically benefit the euro. Yet, that's proving not to be the case.

"What is notable about recent price action is that the euro is struggling even as European bond yields rise. German yields recorded their largest increase since March amid the latest Middle East flare-up and associated rise in oil prices. Under normal circumstances, higher yields might offer some support to the currency," says George Vessey, Lead FX and Macro Strategist at Convera.

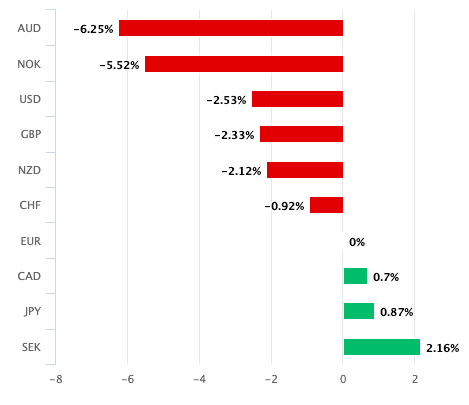

The euro-dollar is flat on the week and is capped by the 1.1450 level. Euro weakness is more apparent elsewhere: the pound-to-euro rate has risen to its highest level in more than a year as a trend of appreciation in place since last November accelerates.

Above: EUR performance in 2026.

The Euro's Problem: These are 'Bad' Hikes

Euro weakness is certainly an important contributor to GBP/EUR upside, and the view from BNY is that it's vulnerable to worries that the ECB will deliver the wrong type of rate hikes.

The thinking is this: a good rate hike is one that responds to a strong economy that generates its own inflation.

A bad rate hike is one that responds to an economy experiencing high inflation but low growth.

The view at BNY is that the ECB could be at risk of delivering the latter, one that penalises economic growth.

Indeed, the euro clearly has not benefited much from the ECB's June rate hike, particularly against currencies belonging to central banks that have opted to do nothing (BoE included).

The Pound's Positive Two-way Rates Story

On the other hand we have the pound which has benefited through the course of 2026 from the UK's high relative rates story, with outperformance becoming more pronounced following the onset of the Middle East war.

But looking ahead, there is a near-consensus expectation in the institutional analyst community that outperformance will fade as that rates advantage eventually declines.

The standard view of an institutional FX analyst might look something like this: the market expects the Bank to hike, but we don't think they will hike. Therefore, rate hike expectations will fall and take the pound with it.

That's textbook FX.

"Counter to market expectations for a rate hike, it is RaboResearch’s view that steady BoE rates will prevail through to the end of the year, which should undermine GBP," says Jane Foley, Senior FX Strategist at Rabobank.

But the BNY good vs. bad rate cut is a challenge to the view: What if raising interest rates is bad for an economy and bad for a currency?

The Bank of England's Steady Hand Helps

The Bank has decided to play it cool on signalling what will happen to interest rates, unlike the ECB, where there are a number of outriders advocating for rate hikes (see Nagel's recent comments).

By limiting its guidance, the Bank of England gives itself the flexibility to avoid growth-squashing rate hikes and even consider rate cuts in later months.

BNY thinks that in a world of cuts = good for growth, pricing out rate hikes is a potential positive for the currency.

"Compared with the ECB, we believe the BOE’s flexibility around its price stability mandate is a deliberate choice that isn’t currently damaging the currency," says Yu. "The Monetary Policy Committee can’t fix the U.K.’s structural issues, but it can avoid making them worse."