Image © Adobe Images

The pound is enjoying a purple patch, helped by elevated UK yields, defferred political risk and tentative signs the labour market is steadying.

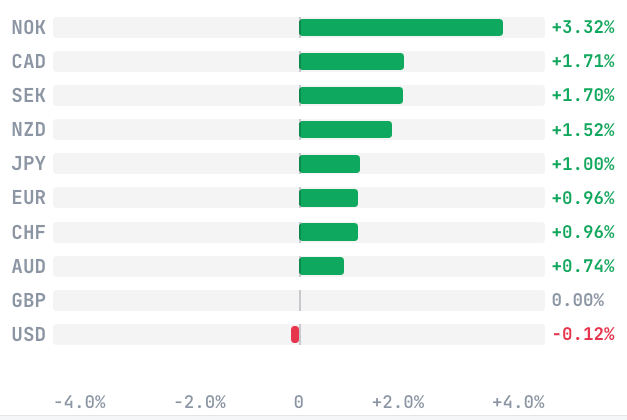

The British pound is now the second-best performing G10 currency over the past month, behind only the U.S. dollar.

"There was no particular catalyst, but probably the slightly softer euro and the proximity to big support levels triggered some unwinding of stale sterling short positions," says Chris Turner, head analyst at ING Bank.

"Here, asset managers in particular have been running some large sterling short positions," he adds.

Those short positions matter because they can become a source of support when the currency refuses to fall. Investors betting against sterling are forced to buy it back, helping extend the recovery.

Jobs Report Offers Fundamental Support

It's not just structural adjustments in the underlying market supporting the pound.

Although it's a quiet week for front-line data out of the UK, today's jobs report survey is definitely worth taking note of as it provides further evidence against the likelihood of rate cuts at the Bank of England.

The REC survey on jobs showed the labour market is steadying and wage increases are still elevated, which should ensure the Bank of England holds interest rates at current levels for an extended period. On balance, that can support the pound against currencies where interest rate expectations are declining.

Looking at the headlines of the REC survey, the permanent staff placements index rose to 49.1 in June, from 44.1 in May.

The permanent staff salaries index rose to 53.1 in June, from 52.2 in May.

"Easing policy uncertainty and a drop in energy prices boosted hiring sentiment in June according to the REC, with the permanent staff placements rising to just shy of the 39-month high it hit back in February and March," says a response note from Pantheon Macroeconomics.

"All told, the relatively quick recovery in the REC's permanent staff placements balance suggests any hit to hiring from the war in Iran looks to have been short-lived," it adds.

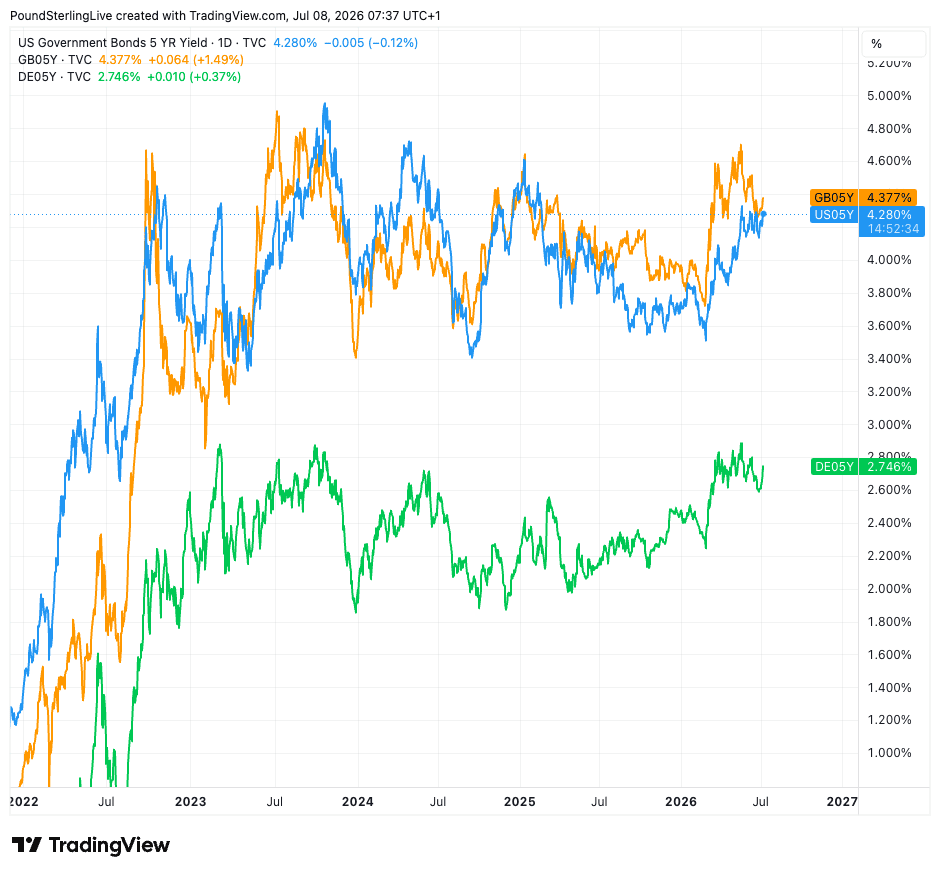

Bond Yields Offer GBP A Carry Advantage

Robust economic data means the central bank rate profile stays steady, and that in turn underpins short-term bond yields.

It's those yields that attract foreign money flows that ultimately underpin the pound.

What we're seeing across the FX analyst community is the 'carry' trade is carrying the day: investors are borrowing in low interest rate currencies and investing where rates are higher.

Low external volatility and positive investor sentiment - as signified by stock market gains - tend to make carry more attractive.

For the pound, that means relatively elevated bond yields are proving supportive.

"The Gilt market constraint is already quite tight and carry support should be in place for a while given the MPC's reluctance to ease policy further any time soon, notwithstanding some additional loss of data momentum lately," says a weekly FX market update from Barclays.

Above: 5-year bond yields: UK, U.S. and Germany.

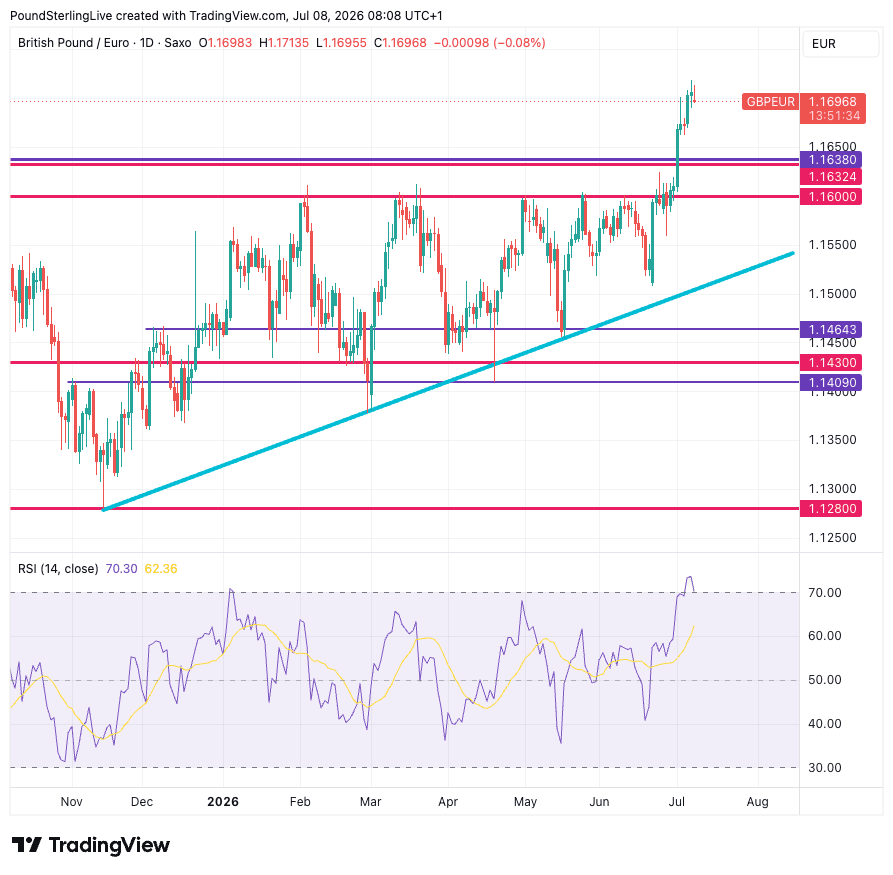

Can the Pound Continue to Rise?

All signs are pointing to the pound entering a more settled period following a strong run of gains, suggesting the recent rise is set to fade.

Notably, there have been some interesting moves in the GBP strip of late: the pound-to-euro and the pound-to-Canadian dollar have both broken out of long-running multi-month ranges.

That means the tide across GBP is rising. It also means that when those breakouts settle, broader momentum fades.

Above: A strong run, but the move should run out of steam.

We're watching GBP/EUR's ability to move above 1.17 in this regard, as we suspect a pullback from here can calm the pound more broadly and allow for some consolidation.

Technicals on the GBP/EUR daily chart argued in favour of a pullback as the move from 1.16 to 1.17 took the exchange rate into overbought territory according to a RSI reading that breached 70 (see chart).

That is usually a harbinger of a pullback and consolidation, which is likely to ensue in the short term.

Autumn Headwinds on Longer-term Fiscal Concerns

For the pound, politics is surely worth watching over the coming weeks, and we suspect by the time of the Autumn budget, they will present a noticeable headwind.

A number of financial pundits have looked at the strengthening pound and UK bond markets and said this is a vote of confidence in incoming Prime Minister Andy Burnham.

We're cautious: Burnham has said nothing about policy, which means these claims don't carry water.

We suspect that towards the end of the month, he will start fleshing out his policies.

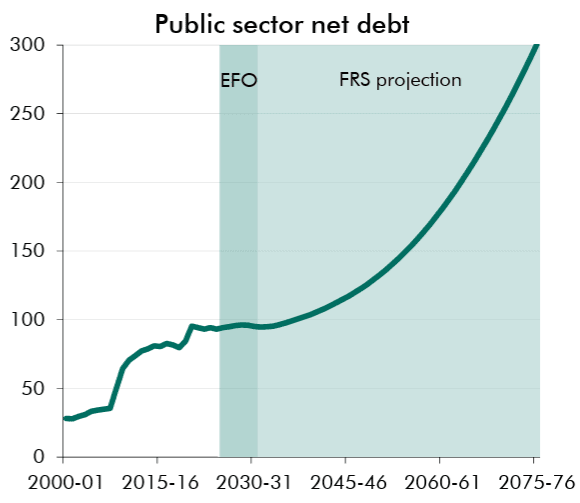

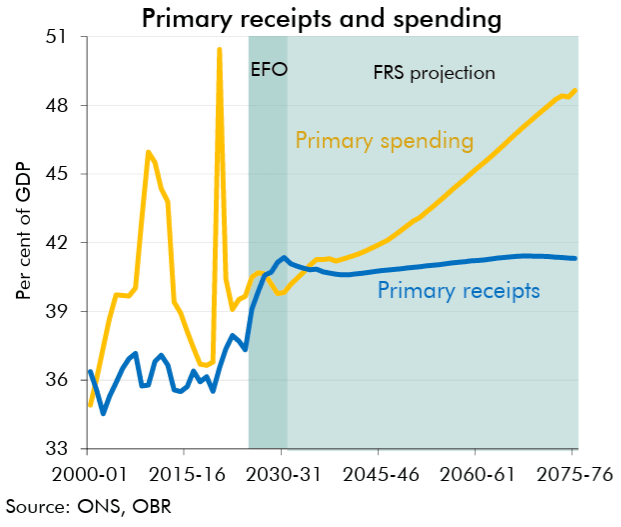

Unfortunately for Burnham, the fiscal picture is treacherous: the budget watchdog (Office for Budget Responsibility) said Tuesday that UK public finances are heading towards an unsustainable long-term path.

It said the UK’s debt trajectory would move on to "an unsustainable and ever-rising path" in almost all scenarios.

Stabilising debt at 95% of GDP (current OBR baseline) from the end of the forecast horizon (2030-2031) onwards would require spending cuts or tax increases equivalent to more than >£100bn a year.

Fiscal sustainability concerns will return as a market-relevant theme. For the pound, that's a risk on the horizon.