Image © Adobe Images

The euro manages to hold above $1.14 as oil marches on towards $80/b on US/Iran escalation.

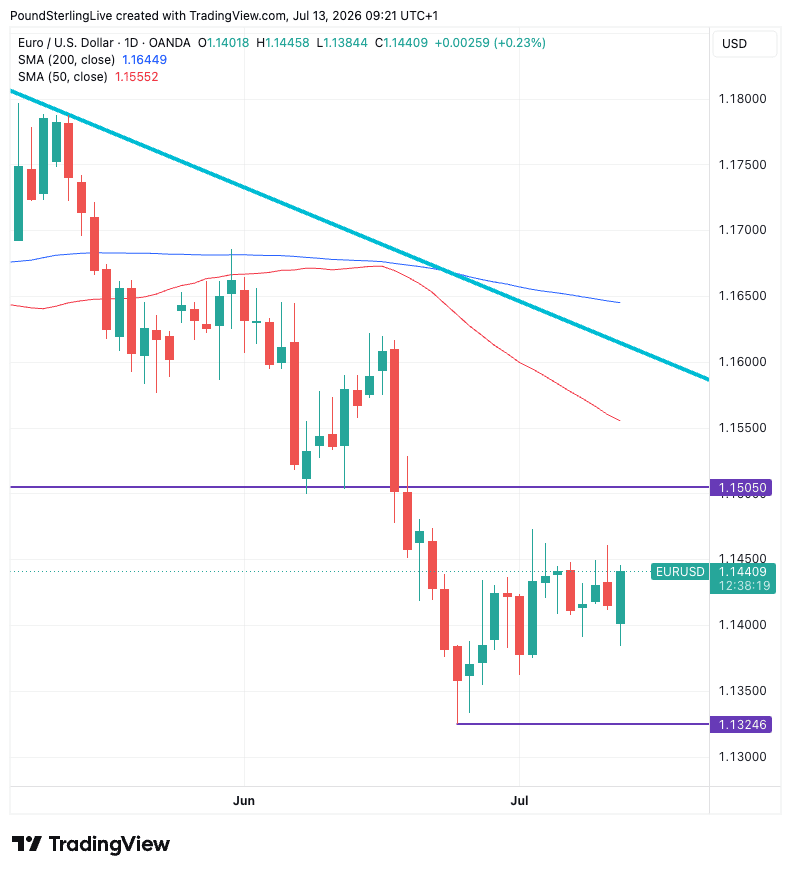

The euro-to-dollar exchange rate holds above the key 1.14 level at the start of the new week, but the recovery will remain merely corrective unless the pair can reclaim some key resistance points.

That's because the broader technical picture remains bearish: the pair continues to trade below the 50-day moving average (1.1555), the 200-day moving average (1.1645) and the long-term descending trendline from the January highs.

The alignment of the moving averages and trendline reinforces the bearish medium-term outlook, even as the recent price action suggests downside momentum has eased.

June saw a notable sell-off in the euro-dollar before the pace of the decline moderated, suggesting there's now a defence line at 1.1325.

The pair appears to be entering a consolidation phase after that sharp sell-off, which leaves scope for further near-term recovery.

However, any rebound is likely to encounter increasingly strong resistance, first at 1.1505, then at the falling 50-day moving average, before reaching the much more significant confluence of the 200-day moving average and the long-term descending trendline.

That resistance cluster is likely to define the medium-term outlook: unless EUR/USD can break above it, rallies should continue to be viewed as corrective within a broader downtrend.

A move back below 1.1400 would shift the focus back to 1.1325, with a break there signalling a resumption of the primary bearish trend.

Looking to the week ahead, the primary scheduled calendar risk is the midweek release of U.S. inflation numbers.

Here, consensus looks for a reading of -0.1% month-on-month for June, a decline that would reflect the paring of energy price gains that followed the initial stages of the Middle East conflict.

Core CPI - arguably more important for policymakers and financial markets, is nevertheless seen staying at an uncomfortably high 0.3% m/m, up from 0.2%.

Should the data undershoot expectations the dollar could fall as it would ease bets for a Fed rate hike later this year, but if it beats expectations, the dollar can rise.

"The takeaway from the last Fed meeting and the more recent comments from chair Warsh is that if they think core CPI is settling at 3% for the rest of the year then they will act quickly. The market is not ready for a rate hike this month and one following at the September meeting, which I view as increasingly likely," says Neil Wilson, a strategist at Saxo Bank.

For now, the market looks for one hike this year, with a second hike priced as a 50/50 possibility. There is scope for that to materially shift higher if inflation data over the coming weeks proves uncomfortably high.

"There is a scenario confirmation that more restrictive policy is required could lead to outsized FX moves if policy diverges even more than currently discounted by markets," says a new strategy note from Goldman Sachs.

Goldmans last week announced it has lowered its forecast profile for the euro-dollar.

U.S.-Iran Tensions Underpin USD

Image © Adobe Images

The dollar was in retreat in early July as traders looked to pare some of June's strong gains, but that mean-reversion looks to have been stalled by the noticeable deterioration in the Persian Gulf.

Here, the U.S. and Iran are back to trading blows and Iran has claimed it's closed the Strait of Hormuz once again.

The subsequent oil rally has coincided with a firmer dollar, as is typically the case during such episodes.

U.S. Central Command said American forces carried out a new round of attacks to degrade Iran’s ability to threaten shipping in the narrow waterway, hitting dozens of targets including Iranian air-defence systems and missile capabilities.

Tehran retaliated with attacks on US allies in the Persian Gulf and beyond, targeting U.S. bases in Kuwait, Bahrain and Jordan, and oil prices rose on fears that renewed clashes could further disrupt flows through Hormuz.

Despite the blows, the market response is relatively contained, which tells us that traders think Trump will ultimately look to keep the conflict contained.

The risk for this line of thought is that Trump realises that the U.S. needs to reestablish the 'deterrence effect', i.e. ensure Iran and its allies understand U.S. power and resolve.

For that to happen, an outsized response to Iranian attacks is required.

If that happens, the dollar would find itself well bid.

"It is important to note that the U.S. strategy, with the ceasefire having been declared "over," is shifting to a priority of re-establishing deterrence," says Peter Tchir at Academy Securities.

Neil Wiley, former Principal Executive in the Office of the Director of National Intelligence, explains "Iran will calculate that they can strike when it suits, confident that they can comfortably endure whatever comes back at them. In this circumstance, there is fundamentally no deterrence. I am concerned that this is now where we find ourselves. Establishing or re-establishing deterrence requires, ironically, a very disproportionate response."