![]()

Image © Adobe Images

Analysts are warning today that a new phase of U.S. Dollar outperformance could be unfolding.

The dollar could be on the cusp of another meaningful period of strength as inflationary pressures build in response to ongoing escalation in the Middle East and rising prospects for Federal Reserve rate increases.

"Short-term momentum is swinging back in favour of the dollar as the FX market is finally starting to take the Gulf re-escalation more seriously," says Francesco Pesole, FX Strategist at ING Bank.

The dollar firmed across the board through Monday and into Tuesday as markets responded to news U.S. President Donald Trump is considering tolling maritime traffic through the Strait of Hormuz.

The signalling here is important: it says the President is potentially more committed to re-establishing America's deterrence doctrine, and that there's potentially no near-term relief.

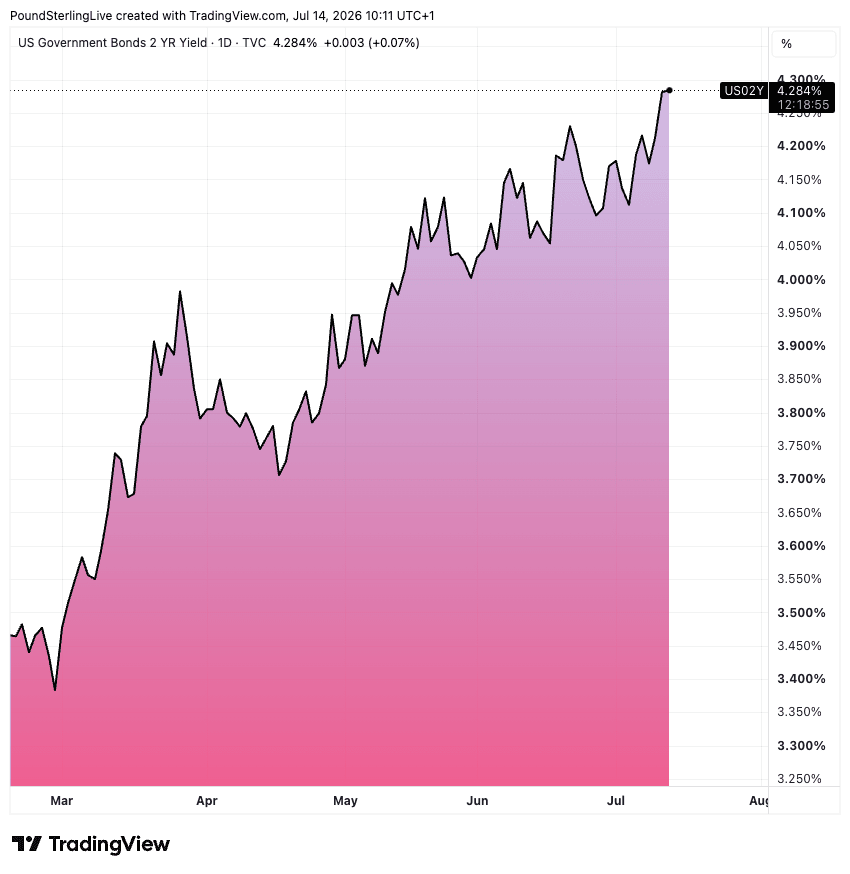

Global bond yields have risen in response - led by a rise in U.S. Treasury bond yields - and market sentiment has soured: classic conditions for a strengthening dollar.

The pound-to-dollar pair dropped 0.45% on Monday to 1.3342, and holds most of the loss at the time of writing Tuesday.

Why the Dollar Could Strengthen Further

The dollar is rising primarily because the market thinks the Federal Reserve will be required to raise interest rates again, potentially as early as this month.

The market-implied chance of a quarter-point hike later this month has climbed to about 50% from less than 10% at the end of last week.

Helping spice up hike expectations was Fed Governor Christopher Waller, who warned Monday, "if we get another hot reading on core inflation this week, then the FOMC will need to consider tightening monetary policy in the near term."

The market is now fully priced for a Fed rate increase by year-end and a second one by mid-2027.

Some analysts think that's still too conservative and think we will see up to five rate hikes in the current cycle, and that's more to do with domestic economic strength than recent developments in the Middle East.

"We move to a positive stance on the dollar as US hiring seems to be at an inflexion point," says Daniel Von Ahlen at TS Lombard.

The independent research house expects the first increase in September, followed by four more next year, taking the total to five hikes.

Above: US 2-year bond yields.

The Middle East Trigger

The market might be falling in line with the previously out-of-consensus view that a genuine rate hiking cycle awaits, a realisation that looks to have been triggered by recent developments in the Middle East.

The reason bond yields and the dollar are rising is a renewed fear that inflationary trends are going to head in the wrong direction following the latest re-escalation in tensions in the Middle East.

Oil and gas prices are higher again, but unlike previous episodes, the market now has to contend with a more 'hawkish' Fed reaction function.

"This positive but contained USD reaction does seem a déjà vu of this spring. But conditions are different now. Reduced Fed guidance after a hawkish shift in June means allowing markets to speculate more aggressively on Fed tightening," says ING's Pesole.

Last month saw Kevin Warsh debut as Fed Chair, and he surprised markets with a forthright commitment to ensure the Fed dominates inflation.

That ultimately signals he will back moves to raise rates if need be, something that was not fully appreciated ahead of his first appearance.

In short, the market will more readily price in rate hikes than was the case pre-June.

For the dollar, that's bullish.

"We see scope for further USD gains in the next couple of months. Sticky US inflation and a resilient labor market will keep Fed pricing hawkish, while US economic outperformance is poised to keep rate differentials supportive of USD," says Elias Haddad, Global Head of Markets Strategy at Brown Brothers Harriman.

Free Report · Worldwide Currencies

Where Next for the Pound? Get the Quarterly Forecast Report

Consensus exchange rate projections from eleven global banking partners, including Barclays, JP Morgan and Citigroup: point forecasts, highs and lows for each quarter through to early 2027.

Delivered by email. Produced by Worldwide Currencies; for information purposes only and not investment or financial advice.