European data is in focus on Tuesday. Image © Adobe Images.

The euro can extend its recent recovery, although upside barriers are significant.

The euro to dollar exchange rate faces a busy week with attention centred on a series of important U.S. data releases, while eurozone inflation numbers should sharpen the debate around European Central Bank (ECB) interest rate rises.

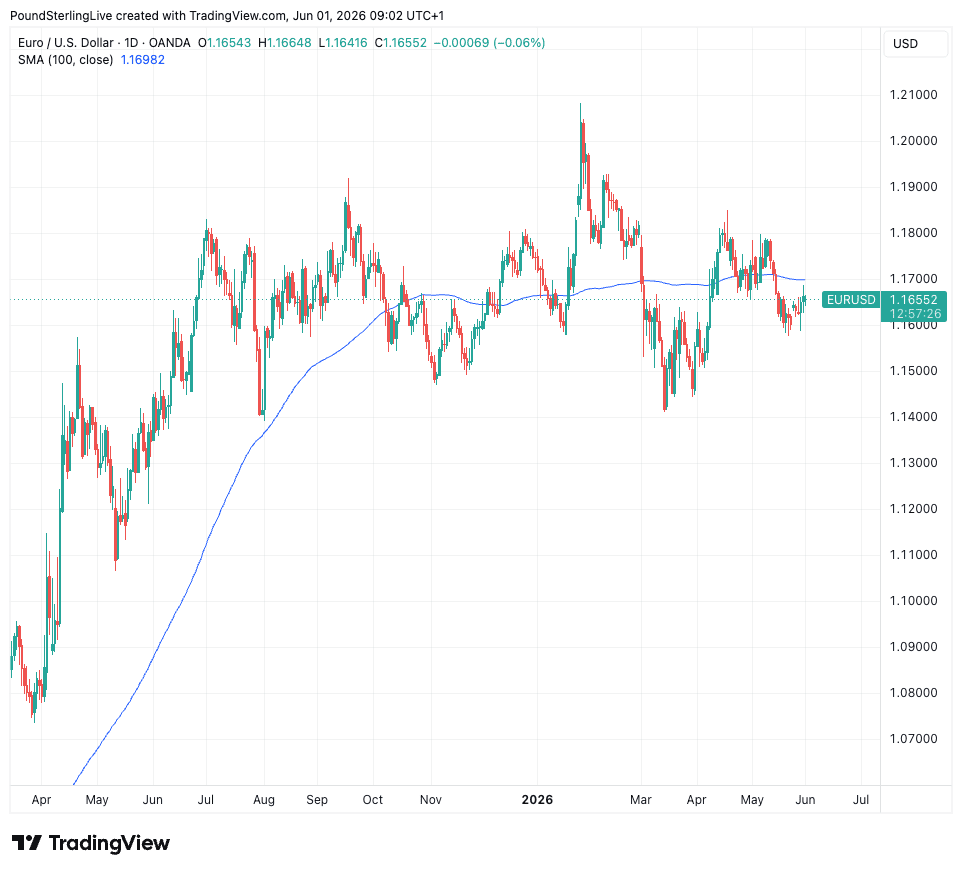

The data will hopefully inject some directionality into an exchange rate that is presently caught between opposing forces that keep it in touch with its 100-day moving average, currently at 1.1690.

A recent recovery from May’s lows suggests downside risks are diminishing, but the pair remains capped beneath important resistance and lacks the momentum required for an immediate breakout.

Expect trading to remain centred on the 1.16–1.18 range, with a slight bias toward further recovery provided support around 1.1600 continues to hold.

The technical studies show sideways directionality is in charge, which means those with impending payments should be reactive to any notable responses to this week's data.

The U.S. leg of the trade will remain the dominant one and we'll be watching: ISM manufacturing (Mon), JOLTS (Tue), ADP, factory orders and ISM services followed by the Beige Book on (Wed), then Challenger job cuts (Thu).

But it's Friday's non-farm payrolls that is the highlight, as it's the key input into the Federal Reserve's mandate to optimise the labour market. The consensus looks for 93k jobs to have been created in May.

The unemployment rate is expected to remain unchanged at 4.3%, but the risks look lower if the payroll gains show up on the household side.

The market will be looking for all of this week's data to offer fresh signals as to whether or not the Federal Reserve has scope to lower interest rates this year. The rule of thumb being that undershoots lessen the odds of a rate hike, which is bearish for the dollar. The opposite is true for stronger-than-forecast data.

The dollar has firmed over recent weeks as solid data and rising inflation rates indicate there's limited opportunity to lower interest rates.

U.S. bond yields firm as rate cut bets fade and rate hikes come into play, which is on balance supportive of the dollar.

The euro is meanwhile underpinned by market expectations for a series of European Central Bank (ECB) rate rises this year as the central bank seeks to get on top of inflation.

Eurozone inflation numbers are due out Tuesday and should bring the issue into sharper focus; the consensus looks for a rise to around 3.4% in May, driven by energy prices, while core inflation should move up to 2.3%.

These data should be enough to maintain market expectations for at least two ECB interest rate rises this year.

"A June rate hike thus still looks probable and a follow-up in September to keep everything on track would look to be the central scenario," says a morning market note from Lloyds Bank.

Some members of the ECB Governing Council suggested last week that even a quick reopening of the Straits of Hormuz is unlikely to be sufficient to negate the price pressures the war has already generated, and that rate rises must be considered.

"We expect the ECB to raise rates by 25bp at the next meeting in June, and again at the July meeting in response to the Iran war, having changed our view after the ECB’s April meeting. In our opinion, these rate hikes should be seen as a signalling exercise i.e., that the ECB will not allow inflation expectations to de-anchor and will not allow inflation to meaningfully deviate from target over the medium term," says Josie Anderson, an economist at Nomura.