Image © Adobe Images

The Swiss franc has scaled a new 18-month high against the Euro and remains in a short-term of appreciation against the Pound which could extend over coming days, but ultimately the gains are reaching their limits says a major investment bank.

The gains in the franc have surprised observers of late, given: 1) the global investor backdrop is positive, which is typically when the Franc tends to decline, 2) there has been little indication from the Swiss National Bank that it will even consider raising interest rates in coming months.

Central bank policy divergence and global investor sentiment remain the two key drivers of the Franc, yet they are not delivering the weakness that would be expected.

"CHF has strengthened hard and fast over recent weeks despite higher global yields and an improving macro backdrop, leaving a lot of investors pondering what has really been driving the currency," says John Kalamaras, analyst at Morgan Stanley.

Image courtesy of Morgan Stanley.

- GBP/CHF reference rates at publication:

Spot: 1.2347 - High street bank rates (indicative band): 1.1915-1.2000

- Payment specialist rates (indicative band): 1.2236-1.2285

- Find out about specialist rates, here

- Or, set up an exchange rate alert, here

Analysis from the investment bank finds a combination of "unwinds" in speculative short Franc positioning, broad-based Euro weakness, and – most recently – a widening of eurozone peripheral spreads are the reasons for the outsized move higher in Franc.

"Short CHF positioning among short-term speculative investors has reduced significantly following the recent CHF strength, while the Swiss National Bank has also been progressively gearing up its FX interventions as EUR/CHF has been getting closer to its previous "line in the sand" of 1.05," says Kalamaras.

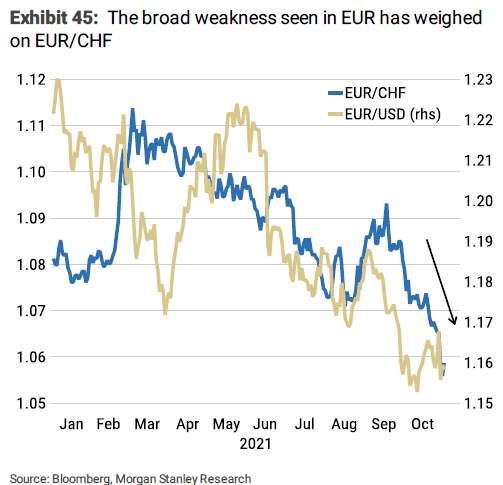

The Euro to Franc exchange rate has fallen to 18-month lows at 1.0536, suggesting the frequency of speculation over a Swiss National Bank (SNB) response will increase markedly over coming days.

The Pound to Franc exchange rate is meanwhile at 1.2350, extending a trend lower that started after it fell out of a multi-week range in mid-October.

A strengthening Swiss franc lowers the cost of Swiss imports and pushes up the cost of Swiss exports; the SNB finds these to be deflationary forces that pose economic headwinds.

The central bank is one of the most active globally in fighting the strength of its currency and this tempo of intervention against gains by the Franc could be expected on further appreciation.

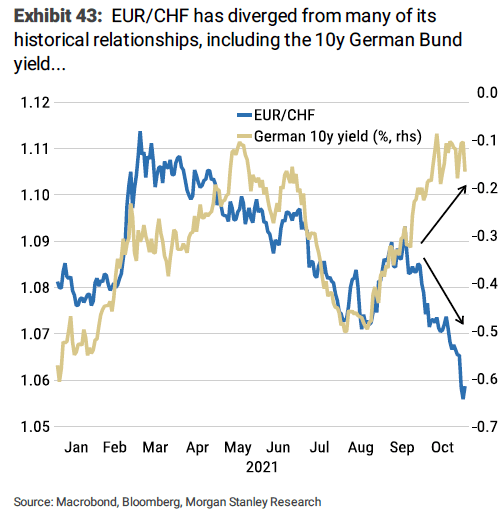

Morgan Stanley finds a key driver of the Franc's gains are recent developments regarding Eurozone sovereign bonds: "the sharp widening of periphery spreads in the eurozone appears to have also been a key driver of the CHF strength," says Kalamaras.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

A divergence in the yield paid on Italian bonds (up) and German government bonds is a key indicator of how investors are once more shifting their approach to various Eurozone nations.

When bond yields diverge in this manner it indicates investors are demanding a greater premium to hold Italian and other so-called peripheral Eurozone country bonds.

This phenomenon was most notable during the Eurozone debt crisis that started in 2009 when the yield paid on Greek, Italian and Spanish bonds rocketed as investors feared for their unsustainable debt positions.

The crisis was ultimately bought under control by a combination of debt reform, external assistance and, importantly, generous European Central Bank policy that saw them buy up peripheral bonds to keep their yields low.

Eimear Daly, an analyst with Barclays, says the recent strengthening in the Franc is related to the divergence between Italian bonds (BTPs) and those of Germany's Bunds, and this should keep the SNB "vigilant".

Image courtesy of Morgan Stanley.

But yield divergence in 2021 is largely symptomatic of an expectation that the ECB will quicken the pace it reduces its quantitative easing programmes and considers raising interest rates owing to rising inflation.

Investors are concerned this will leave some of the Eurozone's weaker nations exposed to hardship.

Hence, a weaker Euro against the 'safe haven' Franc.

But Morgan Stanely expects the Franc's strong run to come to an end.

"Any additional abrupt widening in eurozone peripheral spreads is unlikely, as the ECB will be ready to act against any disproportionate tightening of financing conditions," says Kalamaras.

Morgan Stanley economists expect the ECB to double the pace of its APP to €40 billion/month following the conclusion of PEPP in March 2022, thereby keeping financing conditions accommodative.

Furthermore, the support offered by a repositioning amongst investors is likely to fade.

"Data from the options market also suggest that speculative investors have pared back the majority of their short CHF positions on the back of the recent rally," says Kalamaras.

Image courtesy of Morgan Stanley.

Options markets have moved from being extreme short Franc against Euro and Dollar in recent months to back to neutral levels.

"We see little scope for positioning to stand in the way of CHF weakness should US real yields move higher in line with our expectation," says Kalamaras.

On the all-important question of the SNB, Morgan Stanley expect a more aggressive response to the ongoing strength.

"Following months of inactivity, SNB total sight deposits data – a proxy for the SNB's FX interventions – are suggesting that the central bank has returned to the FX market over the past three weeks," says Kalamaras.

Morgan Stanley expects the central bank to step up its FX interventions "meaningfully" should EUR/CHF move below its previous "line in the sand" of 1.05.

"SNB official’s recent comment on higher CHF curbing inflation suggests the bank's comfort with some modest CHF strength. But we retain the view that EURCHF 1.05 is the line in the sand for SNB interventions, with markets likely respecting this, leaving the pair to stabilise around this level," says Barclays' Daly.

"Despite no signs of intervention from deposits data, we believe the Bank’s vigilance remains, given the recent move lower in EURCHF post a less-dovish ECB/widening of BTP-Bund spreads," he adds.

Morgan Stanley advocate a 'long' USD/CHF in anticipation of future weakness in the Franc, but they say it is too soon to bet on a recovery by the Euro.

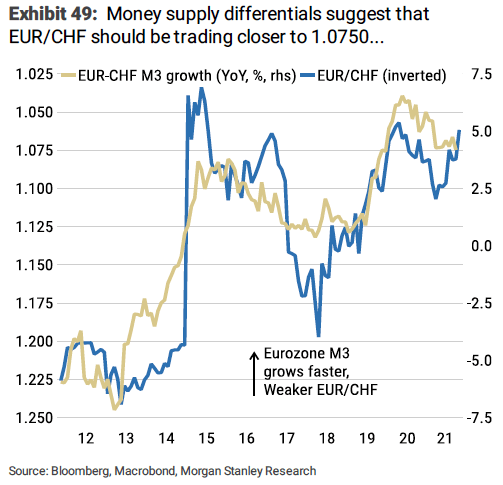

"While we see limited further downside in EUR/CHF from here and think that EUR/CHF should be trading closer to 1.0750 given current conditions, we do not suggest that investors engage in long EUR/CHF positions yet," says Kalamaras.

They expect EUR/USD to keep moving lower heading into the end of the year which, combined with some weakness in 10y Bund yields should offset part of the upside pressure on EUR/CHF coming from higher US yields, "resulting in only a protracted rise in the pair".

However, Barclays see a "tactical" opportunity in backing further gains by the Franc, given Switerland's low inflation keeps domestic real yield erosion contained.

"Concerns of rising inflation and lower activity post last week's US CPI and consumer sentiment should also keep CHF's bid given its safe haven status," says Daly.