Image © Adobe Images

Swiss franc strength is a function of its store of value property in a world fearful of inflation.

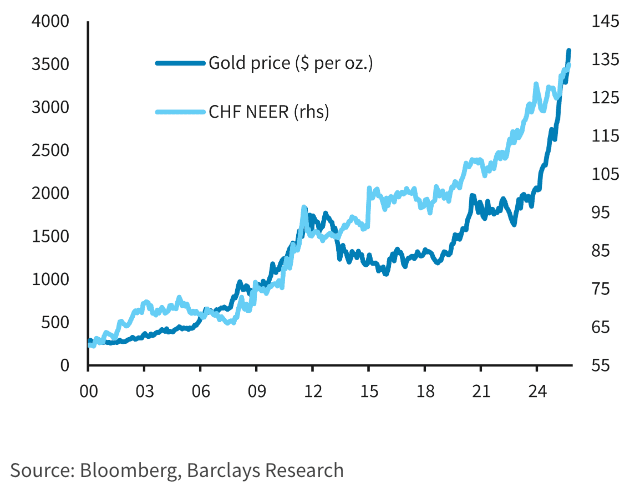

Gold prices surge to new record highs and the Swiss franc outperforms

The Swiss franc continues to be viewed as the foreign exchange market’s answer to gold, with Barclays describing it as “gold’s FX twin” amid ongoing fears of inflation and monetary debasement.

Analysts at the bank argue that both assets play a similar role in investor portfolios. "They yield about the same and are both supported by concerns about currency debasement," Barclays writes in a recent note.

Gold rallied to record highs this week while the Franc is the year's second-best performing G10 currency.

This CHF outperformance looks absurd: its central bank sits on a 0% interest rate while global stock markets print record highs.

FX theory states that higher interest rate currencies should strengthen against low-yielding currencies. It also states that the traditionally safe-haven Franc should struggle at times of market exuberance.

The Yen shares similar characteristics to its Swiss peer, yet it is underperforming massively.

It's gold that offers the answer as to why CHF is doing so well:

"At first glance, the Swiss franc appears to be gold's incarnation in FX space. The CHF is currently yielding about the same as gold, it has also been trending up for a while – and particularly so since the GFC – and is heavily thought of as the place to be if one is worried about currency debasement," says a currency note from Barclays.

Debasement is where a central bank increases the money supply excessively and reduces the purchasing power of the currency it issues.

This is the case for central banks such as the Bank of England and the Federal Reserve, where interest rates are being cut despite inflation rising.

Swiss inflation is contained while the central bank and government oversee credible fiscal and monetary policies, ensuring confidence in the franc as a store of value, akin to gold.

Yet, for all their similarities, Barcalys says there are crucial differences too.

"The main of which being valuations. It is hard to evade the conclusion that the CHF is currently c.10% overvalued, even if this mismatch is likely to stick with us for a while. This makes the CHF a second-best as an inflationary hedge versus gold," says the research note.

The franc's overvaluation is a consistent feature across models and frameworks.

Barclays' BEER model has EURCHF fair value at parity, some 8% above current levels. Its FEER model says the franc is about 10% overvalued, depending on the current account metric one uses as a benchmark.

The trade-weighted franc remains c.10% higher than where it should be in order to neutralise the inflation differential between Switzerland and its trading partners, argues Barclays, adding it is around 8% too cheap versus short-end rates in the Eurozone.

Despite being overvalued, Barclays thinks the currency is not at risk of correction:

"That said, we expect this misvaluation to persist given strong safe asset demand and the SNB's reluctance to cut to deeply negative rates territory or engage in aggressive FX intervention."