"Conclusion: stay bearish on the Dollar." - Deutsche Bank on the Dollar's outlook.

The US Dollar remains on course for steady and continued decline during 2018, according to strategists at Deutsche Bank, who are doubling down on their “bearish” call after encountering some pushback against it from clients.

Deutsche Bank has held a consistently bearish view on the Dollar during recent times and argued earlier in January that the greenback will be increasingly pressured in 2018.

“We believe the dollar has marked a medium-term peak and should struggle again in 2018,” writes George Saravelos, global co-head of foreign exchange research, in a note on January 9.

Saravelos and the team say inflows of international capital into the US will recede from earlier peaks during the current year and that the current account deficit will also widen, both factors likely to augur a weaker Dollar.

The current account deficit represents a nation’s bank balance with the rest of the world, and covers the trade balance of goods and services as well as movements in international capital flows.

“Currency moves over the medium-term ultimately boil down to one thing: flows. If inflows into an economy pick up the currency strengthens and vice versa,” Saravelos wrote.

Lofty valuations for US stock markets, and assets in general, mean international buyers could become fewer in number in 2018, reducing inflows of foreign capital and a key source of demand for the Dollar.

Meanwhile, President Donald Trump’s tax reforms are seen widening the current account deficit, presumably by stimulating demand for imports given the windfall gains to companies and consumers owing to the reforms.

Saravelos and the Deutsche Bank team posited that, for the Dollar, these factors would outweigh the allure of rising US interest rates this year. They also go hand in hand with what Saravelos says is another source of long term downward pressure for the Dollar.

“Interest rate differentials don't always drive currencies and Fed rate hikes will continue to be of lesser importance for the USD this year. Deteriorating flows will matter more instead,” Saravelos wrote.

Wednesday saw the strategy team citing client “pushback” against its call for a weaker greenback when they shot down “Three myths on the Dollar” currently doing the rounds among commentators.

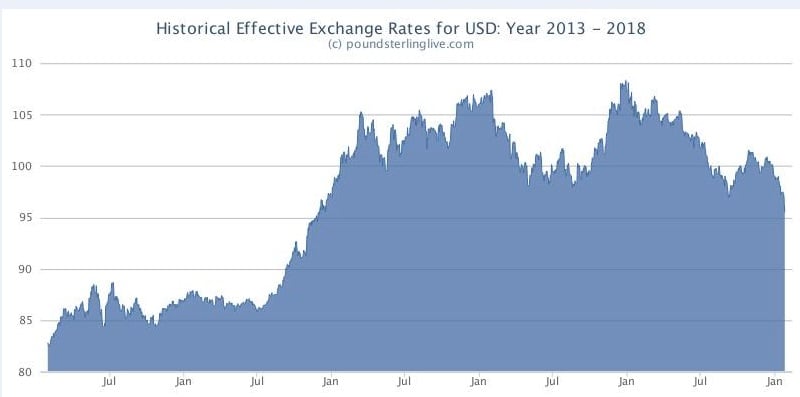

Above: Graph showing US Dollar Effective Exchange Rate Index.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Myth 1: The market is very short dollars and it is consensus

The US Dollar index shed 10% of its value during 2017 and has gone on to lose more than 3% of its value so far in 2018.

This may have been a factor in why some clients said “the market is very short dollars and it is consensus” and had trouble accepting Deutsche Bank’s call that the Dollar can fall further in 2018.

“We disagree. Many cite CFTC positioning as evidence of extremely short dollar positioning but it is important to adjust the data for the growing size of traded volumes over time. Adjusted for open interest, the aggregate dollar short is close to flat,” Saravelos responded Wednesday.

“Our own COFFEE indices which cover around 30% of global option volumes as recorded on the DTCC show dollar selling that is only a third of the size compared to the historical extremes of dollar buying.”

Chicago Futures Trading Commission data showed traders’ bets that the US Dollar will fall reaching a five year high back in 2017, which may have helped bring about the near double digit decline in the US Dollar index.

In the week ending January 23, the total bet against the Dollar rose by $2.8 billion, to a total of $13 billion, although this position was worth nearly $20 billion just back in October.

In other words, even the CFTC data show a reduction in bearish bets against the Dollar during recent weeks - despite the Dollar’s continued falls.

Saravelos also flags that the consensus at the start of the year was for a stronger US Dollar in the first half, particularly against the Euro, and that it is yet to fully abandon this idea.

Myth 2: Rate differentials overwhelmingly favour a stronger dollar

It’s well known that US interest rates are rising and the Federal Reserve is expected to raise them even further in 2018. Many even say it will raise rates faster than it has done before in the current cycle.

On the other hand, Eurozone interest rates are not going anywhere fast while the Bank of Canada is the only developed world central bank besides the Fed to have committed to a proper hiking cycle.

This has led to a sharp widening in the gap between yields on two year US government bonds and two year German government bonds.

The so called “two year rates spread” is now in excess of 2.5%, its highest level since before the financial crisis, but the Dollar is still falling against the Euro and other currencies.

This is why recent price falls have left so many scratching their heads, and is also a reason why some Deutsche Bank clients have had trouble buying Saravelos’ bearish call, because changes in short term market interest rates are thought to be a positive driver for a currency.

“Dislocations between FX and rates have been the norm, rather than the exception in pre-crisis years,” Saravelos writes, Wednesday, before flagging that this very same situation occurred during the years leading up to the financial crisis. The last time the “rate spread” got this large.

“This notwithstanding, the dollar yield advantage over the rest of the world is not as large as the level of rates suggests because the yield curve is unusually flat and [inflation compensation] extremely low,” Saravelos adds.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Myth 3: Dollar buying because of US tax repatriation

Much has been made among foreign exchange commentators over the potential impact that President Donald Trump’s tax reforms might have on the US Dollar.

US corporates have squirrelled away an estimated $3.5 trillion of profits in offshore locations over the years, given that these companies already pay tax on their earnings in the foreign countries where they operate, while the US traditionally hit them with another round of corporate tax on repatriation.

President Trump’s tax reforms change this by offering a one time discount that reduces the tax rate on offshore profits to as little as 8% in some instances, in a move designed to encourage repatriation and investment in the United States.

Many an FX strategist has theorised that at least some amount of these foreign profits will be parked in foreign currency assets, meaning they will need to sell foreign currencies and buy back the US Dollar in order to bring them home to America. This has been the foundation of many a bullish Dollar call for the 2018 year.

“We have addressed the issue in detail in previous work, arguing that the vast majority of offshore earnings is already in dollars,” Saravelos responds.

“Even if this is not the case however, the structure of the current tax change is entirely different to the 2005 Homeland Investment Act which saw large scale repatriation and dollar appreciation.”

Following the last round of tax reforms, during the Bush presidency, companies had just one year to transfer their foreign profits back into the US.

This time around, they do not even need to actually transfer those profits as all of the appropriate monies are now “deemed repatriated”. All that companies need do is to pay the tax that is due on those monies.

“Given that a repatriation tax holiday was widely expected, it would be reasonable to assume that the vast majority of companies have reduced their FX exposure to desired levels before the tax reform was put in place,” Saravelos adds.

“Conclusion: stay bearish on the Dollar.”

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.