In a world where the Dollar has spent the opening of the new year being wiped across the proverbial floor, market expectations for US inflation and interest rates are more important than ever.

The Federal Reserve’s preferred measure of inflation held steady in December, according to the latest PCE Core Price index released by the Bureau of Economic Analysis Monday.

PCE Core prices rose by 1.5% on an annualised basis, which was unchanged from their November level and in line with the consensus estimate of economists. On a month after month basis, the PCE index rose 0.2% when compared with November.

Separately, but at the same time, personal incomes were shown rising at a faster than expected pace of 0.4% during the recent month when economists had forecast a 0.3% monthly gain.

“Consumers are doing their holiday shopping earlier in the year, but they still had money left for purchases in December. Household spending grew a healthy 0.4%, matching the income gain seen during the month,” says Royce Mendes, an economist at CIBC Capital Markets.

The PCE index is similar to the core-inflation measure, which removes volatile commodity prices from the goods basket measured, although it further excludes any other goods and services that are not consumer directly by households.

Therefore, it is seen by interest rate setters at the Federal Reserve as a more reliable measure of underlying inflation pressures in the economy.

“While growth numbers continue to come in strong, inflation remains subdued,” says CIBC’s Mendez.

“The Fed's preferred tracking measure of prices, core PCE, advanced 0.2%, but that only left that stripped down measure of inflation running at 1.5% on the year, no faster than what was seen in November.”

Inflation numbers are always important for interest rate setters because it is these very price pressures that policy makers are attempting to contain, or stoke, when they make monetary policy decisions.

However, in a world where the US Dollar has spent the opening weeks of the new year being wiped across the proverbial floor, market expectations for US inflation and interest rates are more important than they have been for a long time.

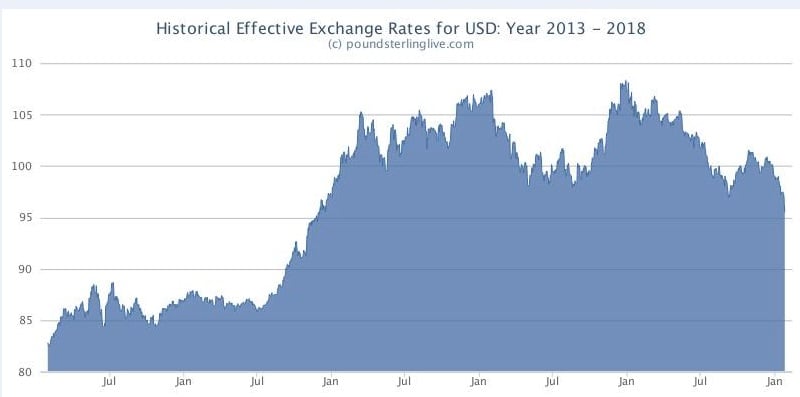

Above: Pound Sterling Live graph showing effective US Dollar exchange rate since 2013.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

How High can US Rates Go?

The Federal Reserve raised the Federal Funds rate by 25 basis points in December so that the top end of the Fed Funds range now sits at 1.5%.

It also suggested in December, via its “dot plot”, that it will raise the Fed Funds rate on three occasions in the current year however, markets are sceptical of whether it will manage to achieve this.

“Investors are still underestimating how much the Fed will raise interest rates given the likelihood of higher core inflation in the US in the coming months,” says Oliver Jones, an economist at Capital Economics.

Pricing in overnight index swaps markets, which enable investors to protect themselves against anticipated changes in interest rates, suggest the majority expect only two rate hikes in 2018.

These two rate hikes would leave the Fed Funds rate at 2%, which is a lowly level when compared with previous interest rate hiking cycles.

Dispensing with scepticism over the Fed’s ability to go on raising interest rates could be crucial to reversing the ongoing decline in the US Dollar.

“We think that a more aggressive Fed will breathe some life back into the dollar before long.... We suspect that prospects for policy will ultimately outweigh the other factors which have been dragging the greenback down,” writes Michael Pearce, another economist at Capital Economics, in a recent note.

The greenback has fallen by more than 3% so far in January, despite US treasury yields also recently having reached close to four year highs, as investors shift out of US assets in order to take advantage of rising returns elsewhere in the world.

Above: Pound-to-Dollar rate shown at 2 hour intervals. It is up nearly 5% so far in January.

Fed to Move Faster and Go Higher than Many Expect

Forecasters at Capital Economics are among the most hawkish in the market, expecting a total of four rate hikes from the Federal Reserve in 2018, which would take the top end of the Federal Funds rate to 2.5%.

However, they are not alone in thinking the Fed will raise rates faster than the market expects and, in doing so, provide some relief to the US Dollar.

“The dollar has slid even as US yields have risen through January, but what is significant in recent days is the medium-term market pricing of the Fed Funds rate seemingly breaking through the range highs,” writes Alvin Tan, a strategist at Societe Generale, in a note Monday.

“If the market expectation of the Fed Funds rate continues to rise beyond ~2.5%, then the higher interest rate cavalry may finally come to the dollar's rescue.”

In fact, the greenback’s decline, which is greater than -10% over a 12 month horizon, may even help inflation make a sustainable return to the central bank’s 2% target and rater setters to push the Fed Funds rate northward.

This is particularly the case if the weaker currency raises the cost of imports, ultimately leading to higher inflation, while also stimulating the export side of the economy through improved competitiveness.

Some economists have said recently that this this is exactly what will happen.

“The Fed will see the weak dollar as a sign of easy financial conditions and a green light to keep tightening monetary policy,” says Aditya Bhave, a global economist at Bank of America Merrill Lynch.

Bhave and the BAML team are forecasting that the Federal Reserve will raise interest rates three times this year and another three times in 2019, which is more than the market currently expects for both years.

Their forecast is based upon the expectation that US inflation will also rise steadily throughout the year, with the Core PCE Price index drifting higher to 1.8% by year-end and core-CPI inflation rising to 2.2% before the end of December.

An important test of the Federal Reserve's appetite for further interest rate rises will take place at its Wednesday meeting, in the current week, as well as after the interest rate setting meeting that is schedule for March.

Wednesday's decision will mark the final meeting chaired by Janet Yellen. By the time the March meeting comes around, the Federal Reserve will be under the watch of Jerome Powell.

Markets will eye the current week's statement closely for signs of a more aggressive rhetoric on interest rates while current expectations are that the FOMC will announce a rate hike at the first meeting to be chaired by Jerome Powell in March.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.