Forecasts for the Pound to Dollar exchange rate for the coming five days.

The new week is underway and it is the US Dollar that is in the driving seat. The US Dollar Basket is up by 0.4% at the time of writing, confirming an all-round desire to increase exposure to the Greenback.

Of course, this move comes after a poor week for the currency, indeed, it was the third-worst performing G10 currency for the week ending 19th August.

We have seen GBPUSD drop sharply after making a fresh high of 1.3186 on Friday.

Strategists at United Overseas Bank (UOB) in Singapore say the outlook for this pair is still viewed as neutral, however, the weak daily closing indicates that a short-term top is in place and the current weakness could extend lower to 1.2940.

“At this stage, a sustained move below this level is not expected. Overall, GBP is expected to remain under pressure in the next several days unless it can move and stay above the 1.3186 high,” say UOB.

The GBP/USD pair continues to form what appears to be a double-bottom reversal pattern.

The current rebound seems to have run out of steam, however, after meeting resistance from the monthly pivot at 1.3168 – a level used by traders to gauge direction of the market, and strong resistance level to boot.

It would probably take a break below Wednesday’s 1.2976 lows, however, to mark a recapitulation of the down-trend, although if that did happen we would be targeting the 1.2863 lows.

Alternatively, a move higher again, and a clear break above the pivot, with confirmation from a move above 1.3200, would probably rise up to 1.3300 initially, before a possible continuation to the level of the neckline at around 1.3400.

We would however expect any weakness in GBP/USD to remain limited having observed the pair's inability to break below that double bottom in the above graphic.

The support for Sterling seen in the approach to 1.28 would suggest it will take a notably negative event to prompt the required selling power to deliver fresh 2016 lows.

This could be a big ask if we note how data from the UK economy for the period following the Brexit vote has been a lot stronger than many analysts and commentators were expecting.

Inflation rose marginally, employment rose and retail sales data easily beat estimates.

Whilst the data does lessen the chances the central bank will have to increase its GBP-negative stimulus measures, most analysts still think the Bank of England (BOE) will cut rates by up to 0.15% and also perhaps increase its quantitative easing programme again in November.

Some economists have also argued the effects of Brexit will not start to come through until the autumn, suggesting a bout of weakness for the pound later in the year.

Indeed, the impact of the weaker Pound on petrol prices and foreign imported goods may take time to hit household’s disposable income.

But then again, we must balance this out with the observation that UK exporters are likely to enjoy a Brexit-boost from the weaker currency.

Latest Pound / US Dollar Exchange Rates

| Live: 1.3441▲ + 0.1%12 Month Best:1.3867 |

*Your Bank's Retail Rate

| 1.2984 - 1.3038 |

**Independent Specialist | 1.3253 - 1.3306 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Will the Pound be Aided by Solid Data this Week?

Will the better-than-expected run of domestic data continue to aid the GBP over coming days?

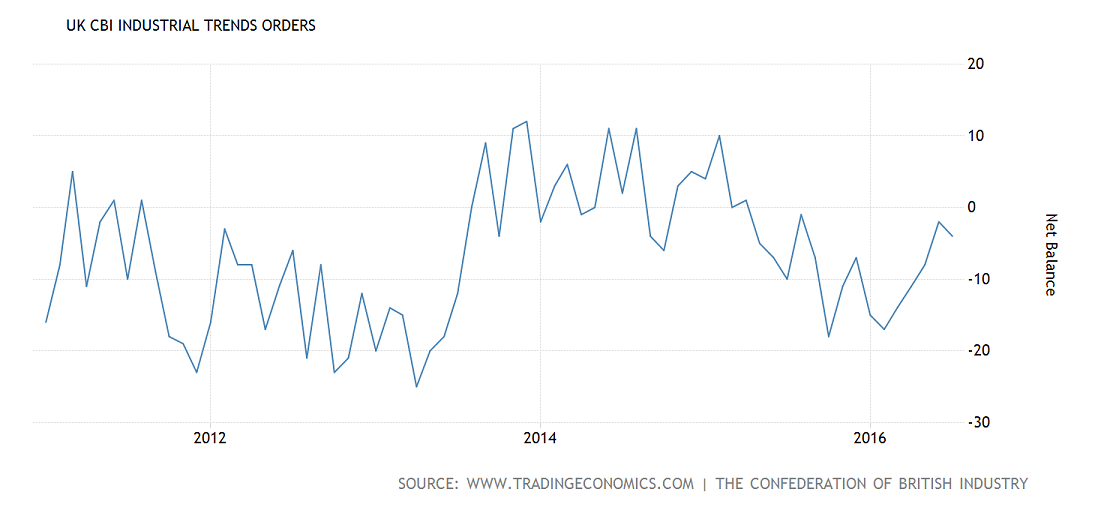

The week kicks off with the Consortium of British Industry (CBI) Order Book Balance in August on Tuesday 23.

This will be the first data for August, so may gain extra attention due its significance in assessing the impact of Brexit, although we would assess the same hit seen in July will not be repeated as the shock of the vote fades.

The July result was -4, which was better than the -6 expected, and was at about the level of the long-run average.

Wednesday sees the release of British Banking Association (BBA) Mortgage Approvals data, which is of limited import to sterling.

There is more significant data out on Friday, however, including Q2 Business Investment (qoq), and then the final estimate of Q2 (qoq) GDP growth data.

The preliminary figure was 0.6% and the consensus estimate for the revised figure is expected to remain at 0.6% qoq (2.2% yoy).

The data, however, does not reflect the impact of Brexit which occurred right at the end pf the period.

The Fed Debate Continues, and Data Therefore Remains Key

Dollar sentiment remains intimately tied to expectations for that elusive interest rate rise at the US Federal Reserve.

The Dollar has fallen as expectations for a September rate rise diminish, with last week's Fed meeting minutes’ casting doubt on when the central bank would increase interest rates in 2016.

However, several voices, including New York Fed’s Dudley and San Francisco Fed’s William’s, said individually, that September was still ‘live’ - strong data in the week ahead could potentially give their views some credence.

From a hard data point of view the week doesn’t really get going until the Tuesday when Manufacturing PMI for the month of August is released, as well as New

Home Sales, which are forecast to fall by -1.8% in July.

Homes will remain under the magnifying glass on Wednesday when Existing Home Sales are expected to show a -0.4% drop mom in July.

On Thursday, Jackson Hole - that yearly central banker conflab – kicks off, with commentary from all major governors closely scrutinized, but especially for Janet Yellen in the case of the dollar, who is set to give a policy speech on the Friday.

The market is still a little bit bewildered by the lack of aggression show by her and her board in raising interest rates and at JH symposium she will have the opportunity to provide more flesh on the bones of current rather thin guidance.

Orders of Durable Goods, that is big things like plant, machinery, transportation vehicles and the such, will also be released on Thursday.

The headline figure is forecast to show a 3.5% rise mom in July, whilst the Core value, which strips out really big ticket one off sales of things like aircraft is expected to increase by 0.5%.

Into the end of the week and it doesn’t let up for the dollar, with a data dump on Friday, consisting of Q2 GDP (albeit second estimate), which is expected to come out at 1.1% from 1.2% preliminary estimate; the Goods Trade Balance, Services PMI in August and Michigan Sentiment in August.