The pound to dollar exchange rate is forecast to fall into the 1.20s by 2017 on a combination of a UK's economic slowdown and repatriation of capital into the US.

- 65% chance UK votes to stay in the European Union say Morgan Stanley

- Worst case scenario forecast is GBP to USD at 1.15 in 2017

- But, pound to fall to 1.25 even in the event of an 'In' vote at referendum

- The dollar's super-cycle not yet complete

The pound sterling will fall notably against the US dollar over coming months, regardless of the outcome of the UK's EU referendum argue analysts at US investment bank Morgan Stanley.

The declines in the event of an 'Out' vote will be substantial argue analysts, but an 'In' vote will be unable to save sterling from a slowing UK economy and the extension of the US dollar's super-cycle higher.

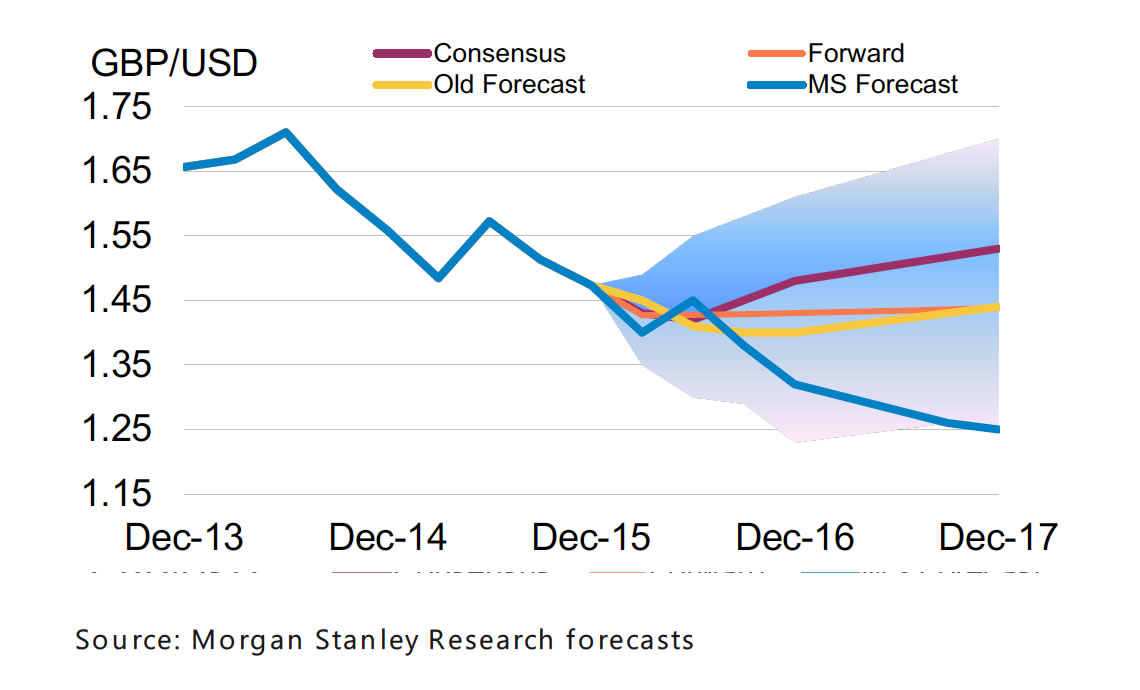

Declines could only stop at around 1.25 in 2017 show forecasts from Morgan Stanley, released in their Spring Global FX Outlook paper.

A key question being asked by those with an interest in sterling is just how low sterling can go on an 'Out' vote?

Latest Pound / US Dollar Exchange Rates

| Live: 1.3197▼ -0.05%12 Month Best:1.3867 |

*Your Bank's Retail Rate

| 1.2748 - 1.2801 |

**Independent Specialist | 1.3012 - 1.3065 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Morgan Stanley: GBP to USD Could hit 1.15 on Brexit

The base-case forecast held by Morgan Stanley is for the sterling to dollar rate to trade at 1.45 by the time of the June referendum and close the year at 1.32.

The base-case scenario does not anticipate the UK voting to leave Europe though with a 65% chance given to an 'In' vote prevailing.

But, “should the UK vote for Brexit on June 23, we estimate GBP/USD could fall as low as 1.20, taking EUR with it,” say Morgan Stanley in a note to clients.

The exchange rate would head as low as 1.15 by the end of 2017 on the event of Brexit; this representing sterling's 'worst case scenario' outcome on a Brexit vote.

Further examples of how soft sterling could become on Brexit are provided by HSBC who forecast a 15-20% decline in the GBP to USD conversion on the combination of an 'Out' vote combined with a delay to Bank of England interest rate rises.

Handelsbanken predict a fall in the exchange rate to 1.22.

Capital Economics see a 15% fall on Brexit, but argue, this is not necessarily a bad thing.

'Boris Shock' Has Faded, But Hedging Pressures to Begin in Earnest

Analysts expect the British pound will remain sensitive to Brexit risks but with the 'Boris shock' out of the market, they believe the next leg down in GBP will be driven by investors hedging UK exposure.

The 'Boris Shock' refers to the sudden slump in sterling witnessed in late February as the Mayor of London made it known he would be campaigning for the Leave camp.

Worryingly for sterling bulls this hedging behaviour still hasn't begun in earnest it is argued.

“GBP will remain sensitive to changes in the polls, gauging probabilities for a Brexit, but this will be of tactical importance, rather than determining the trend,” say Morgan Stanley.

1.25 in 2017, Even in the Event of an In Vote

It must be noted though that analysts at the US investment bank are forecasting a decline in the GBP regardless of Brexit-related concerns.

There are pretty steep declines in GBP/USD ahead even if the UK votes to stay in the European Union.

“Other concerns include a pro-cyclical fiscal policy, the important UK financial sector being challenged by globally low rates, increasing regulation pushing financial sector productivity lower, and a current account deficit fluctuating around 4%,” say Morgan Stanley.

In the eyes of analysts these factors will make it more difficult to fund Britain’s financial needs at current attractive levels, arguing for a lower GBP.

By the end of 2017 Morgan Stanley are forecasting 1.25.

That said, there is the chance for a notable move higher in the GBP to USD exchange rate in the event of an In vote prevailing.

“Our economists put a 65% probability on the UK voting to stay within the EU, so 2Q should see a rebound as markets reprice the selling that occurred as a tail risk for Brexit,” say Morgan Stanley.

But, expect gains to be short-lived as the growth outlook in the UK looks worse, without there even being Brexit worries.

Tightening fiscal policy (watch the budget this week), higher financial services volatility and the manufacturing sector showing signs of a slowdown globally will all weigh on GBP, argue Morgan Stanley.

“Market pricing for the BoE is currently so extreme that there are risks that if wage growth were to pick up significantly, the market repricing would cause GBP to rebound, but we expect that this rebound would be limited,” say Morgan Stanley.

US Dollar Forecast to Benefit From Repatriation Demand in 2016

The pound joins a number of other currencies, euro included, to be found on Morgan Stanley's 'sell' list.

What of the 'buy' list?

"Outside JPY, CHF, USD and SEK, it is hard to find a positive currency story," say researchers, "since USD has not converted into an investment currency yet, the Fed’s ability to dampen USD appreciation should remain limited and not go beyond a tactical impact."

The US dollar is expected to be supported by continued repatriation demand coming out of EM countries.

The strategic USD outlook will likely remain determined by the poor investment outlook elsewhere in the world and the related increase in non-US savings.

"The inability to find adequate local investment opportunities for these savings should lead to a permanent flow of funds into USD," say Morgan Stanley.

Demand for dollars will be broad-based with Emerging Market currency weakness and related US capital inflows driving the performance of USD.

"Simply, it will be weak investment return outside the US and not the superior investment return of USD-denominated funds driving USD valuation," say Morgan Stanley, "hence, USD is likely to remain a repatriation currency in 2016."

The USD’s Super-Cycle Not Yet Over

Analysts at the investment bank believe that this is the final leg higher in the third USD super cycle of the past few decades.

Further adjustment in the emerging world will likely position their economies to benefit afterwards; in such an environment, USD will likely revert back to its status of being a funding currency for higher-yielding investment.

"But that time is not now; while the final leg in the USD bull market is nearing, the magnitude of the rally will potentially be very large in nature as the emerging markets go through a difficult transition period; this is reflected in our forecasts," say Morgan Stanley.