One thing is for certain - pound sterling (GBP) is going to move substantially against the US dollar over coming months. The question is, which way? HSBC's currency team lay out four scenarios.

Political risk has gained traction in British pound exchange rates while the timing of interest rate “lift off” by the Bank of England have proven markets were too optimistic on timing.

As a result, GBP has weakened notably in 2016.

“The GBP’s price action suggests that the market is already worrying about the EU referendum and the associated threat of 'Brexit'. The weakness in GBP we had anticipated for H2 16 has already happened,” says HSBC’s David Bloom, pictured above.

Add to this an unexpected under-performance in the UK economy since the start of 2016 and we can see why the pound has fallen to the degree it has.

The pound to euro exchange rate is down about 5% since the ECB’s December meeting while the pound to dollar exchange rate has fallen from 1.56 in late summer to 1.45 now.

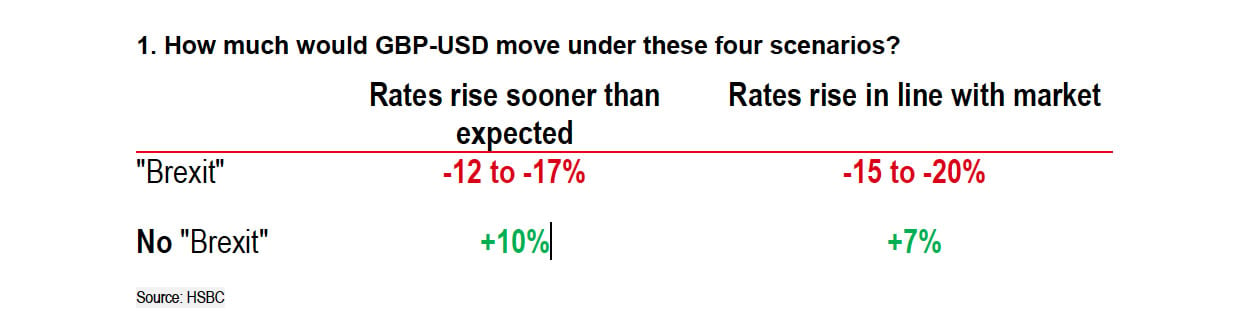

The GBP in 2016: Four Scenarios to Watch

Making currency forecasts rests with variable inputs, of which HSBC have four for sterling’s performance in 2016.

The above represents a simple characterisation of how HSBC view GBP moves from the current spot rate (1.45 as of 10 February 2016).

“Our base case scenario is for the UK to stay in the EU, and rates to rise in November this year, well before the market expects. We see GBP-USD at 1.60 by year end,” says Bloom.

Sterling is Already 7% Lower Than Where it Should Be Thanks to Brexit Fears

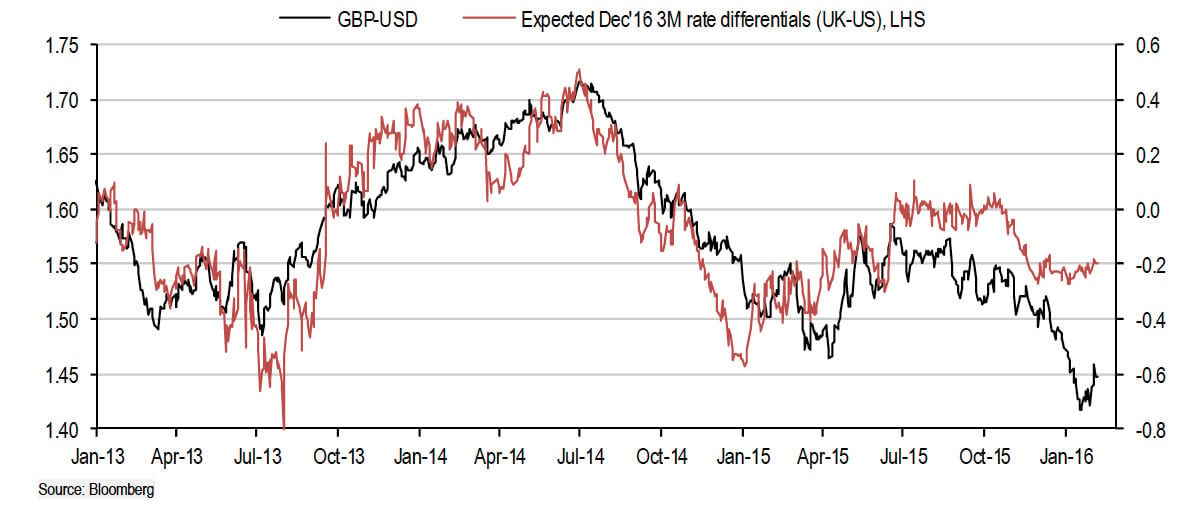

The pound should be higher against the US dollar if it were following its preferred behaviour of tracking the difference in interest rates between the United States and United Kingdom.

“It is clear that a gap opened up a few months after the May 2015 general election and has blown out since December 2015. If we accept that GBP is largely determined by cyclical andn political factors, then any deviation in the currency from the levels implied by cyclical factors is most likely a reflection of politics,” says Bloom.

Currently this gap stands at 7% and HSBC interpret this as a rough approximation for the political risk premium in GBP-USD. i.e the pound has already sucked up much of the risk attributable to the UK exiting the European Union.

GBP/USD undervaluation has also recently been noted by BNP Paribas whose FEER model says the exchange rate should be at 1.64 at the present time.

The acceleration of Brexit-inspired losses has come as David Cameron indicates he is keen to hold the referendum in 2016, and not in 2017.

Furthermore, the numbers favouring leaving have been rising for close to a year now. Judging by these opinion polls, at least, the momentum is with those in favour of leaving.

“A rejection of “Brexit” would see this gap closed immediately, pushing GBP substantially higher. For example, based on the current political risk premium, it would push GBP-USD back to 1.55,” says Bloom.

Eye-Watering 15%-20% Slump if the UK Exits the European Union

HSBC say their preferred scenario is for the UK to remain in the European Union. But what would happen to the currency were the UK to leave?

Bloom explains:

“GBP’s vulnerability would extend beyond the knee-jerk political risk premium reaction to the “Brexit” vote. Extracting the UK from the EU would take a minimum of two years, and most likely many more.

“It would raise questions over the future health of UK export growth, not least for financial service exports. With a current account deficit already at 5% of GDP, GBP can ill afford any additional widening.”

So at the same time as markets would fear a wider current account deficit, there would be questions over its funding.

HSBC point out that amongst the ten worst-performing currencies of last year there are only two countries with worse current account deficits than the UK (Turkey and Colombia) and only one country with a worse fiscal balance (Brazil).

“These structural shortcomings have been ignored by the FX market when it was obsessed with the interest rate outlook. “Brexit” would bring the twin deficits to the centre of the market’s thinking,” says Bloom.

Uncertainty would also likely encourage the BoE to hold off with a rate hike in 2016, and the dovish drift in UK rate expectations that has helped push GBP lower would extend further.

“The combination of a higher political risk premium, a potential crisis of confidence about the UK’s balance of payments, and a more dovish BoE would likely see GBP-USD trading back down to levels not witnessed since the aftermath of the early 1980s UK recession during the ‘Thatcher era’” says Bloom.

HSBC Forecasting an Exchange Rate at 1.60 Though

HSBC are forecasting 1.60 in sterling-dollar by year end, based on their assumption the UK will stay in Europe AND that the Bank of England raises interest rates sooner than markets had expected.

"Once political risk is out of the way, we expect the exclusive preoccupation of the market to revert to interest rate differentials. We believe developments here could foster an additional rally, bringing us to our year-end target of 1.60 on GBP-USD," says Bloom.

The market currently expects no interest rate hike in 2016.

Another View: Barclays say Brexit is Good For the Pound (on one condition)

HSBC could be missing a trick argue Barclays who suggesting that beyond Brexit the pound could strengthen.

“It is not clear to us that EURGBP is the best expression of referendum risk. Indeed, long-horizon risks in EURGBP are ambiguous, and there are clear referendum-related downside risks to EURGBP in the nearer term, in our view,” says Marvin Barth at Barclays.

The initial reaction to a UK exit will likely be EURGBP moving higher, given the market’s bias.

But, further out the exchange rate reaction will depend on how Europe reacts.

If politics in the EU turned for the worse - which is the preferred scenario at Barclays - the UK may be seen as a safe haven from those risks, reversing EURGBP’s appreciation.

In short, the European Union has more to lose from a British exit than Britain does, something markets are not yet fully accounting for.