Above: File still of Scott Bessent. Courtesy of Bloomberg.

The U.S. and Japan appear keen to coordinate attempts to weaken the dollar.

A new week sees welcome volatility in global foreign exchange markets as USD weakness triggers breaks in familiar trading ranges, introducing opportunity and risk for those with impending currency transactions.

Renewed dollar weakness is being driven by signs that Japanese and U.S. authorities could coordinate to defend the yen and weaken the dollar.

"Trading desks are on intervention watch after the New York Federal Reserve reportedly conducted 'rate checks' for the Treasury on Friday," says Karl Schamotta, FX strategist at Corpay.

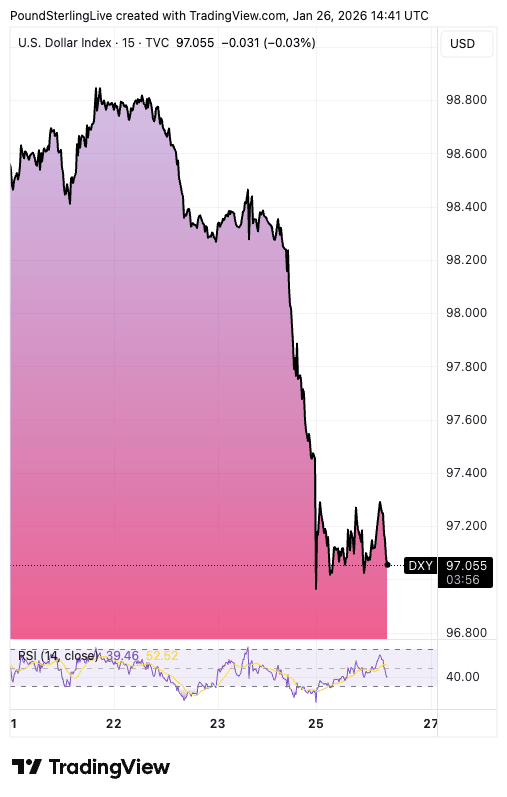

Above: The dollar index, a broad measure of USD value, has fallen sharply since intervention risks started to rise.

A rate check occurs when monetary authorities contact banks to ask for current exchange rates and market conditions, which is widely considered more of a signalling exercise than anything, as such checks are typically followed by direct intervention.

The Bank of Japan offers the most obvious examples of such activity and "for currency market veterans, the reported involvement of the US Treasury is the more intriguing element," explains Schamotta.

(Reach out to Horizon Currency's dealing desk for assistance in optimising your international transfer, more information here).

What's behind the U.S. involvement? Schamotta explains there are two possible explanations, with one having a particularly far-reaching implication for currency markets:

🔘 The more likely is that Bessent believes yen weakness amplified last week’s sell-off in Japanese government bonds, indirectly lifting US borrowing costs and warranting a response.

🔘 A less likely, but more consequential, possibility is a Plaza Accord-style agreement to push the yen higher in a sustained way, aimed at curbing inflation in Japan and narrowing cross-Pacific trade imbalances. The former would point to modest adjustments to stabilise bond markets.

"The latter would mark a profound shift in how advanced economies manage exchange rates, and could usher in a period of extreme volatility as intervention joins tariffs as a routine policy tool," explains Schamotta.

"The U.S. authorities, led by President Trump and Treasury Secretary Scott Bessent, have made no secret of their desire to see a weaker U.S. dollar," says Kit Juckes, FX strategist at Société Générale. "From a U.S. perspective, the North Asian currencies are very undervalued, and they run big trade surpluses with the U.S."

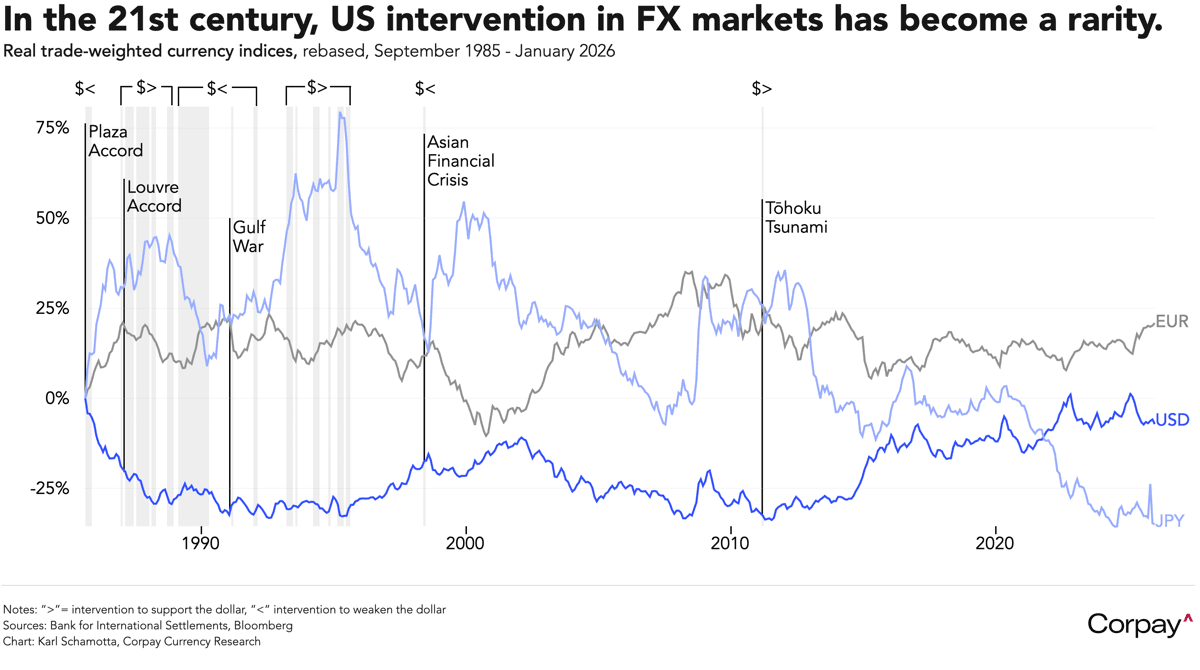

Image courtesy of Corpay.