Above: Federal Reserve Chairman Jerome Powell. Image © Federal Reserve.

The Federal Reserve will continue to hike interest rates by sizeable increments and underpin conditions for further Dollar strength say analysts.

The Dollar is broadly stronger in the wake of the decision by the Fed to hike interest rates by 75 basis points on Wednesday June 16, a move aimed at tackling high and persistent U.S. inflation.

The market had been predicting a 50bp move until last Friday's strong U.S. inflation report shifted expectations once more and ultimately pushed the Fed to act aggressively in order to get inflation expectations under control.

This was the biggest hike since 1994 and the Federal Open Market Committee (FOMC) signalled further sizeable hikes are likely over coming months, before the brakes are applied in 2023.

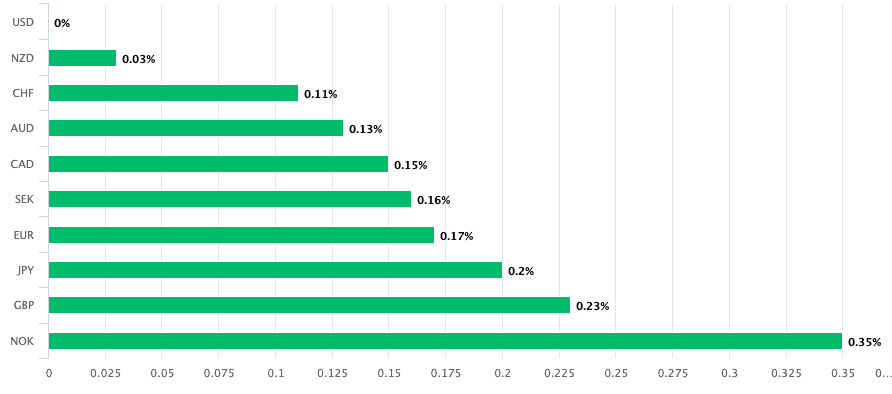

For the Dollar the developments have proven broadly supportive and the U.S. currency is the best performing major of the day thus far on Thursday.

Above: USD performance on Thursday June 16.

The Pound had rallied against the Dollar on Wednesday but much of Sterling's 1.46% gain was a result of a broader relief bounce mid-week following the sizeable sell-off of Monday and Tuesday.

The Pound to Dollar exchange rate is now quoted at 1.2145, having been as low as 1.19338 earlier in the week. (Set your FX rate alert here).

The Euro recorded a 0.30% advance on the Dollar on the day but price action here is decidedly choppy and the Euro-Dollar rate is back at 1.0438 at the time of writing; the level it closed out FOMC day.

New projections showed the Federal Reserve raised its inflation forecasts to 5.2% for 2022 (previously 4.3%), 2.6% in 2023 (prev. 2.7%) and 2.2% in 2024 (prev. 2.3%).

In the longer-run inflation is however seen to be back at the target of 2.0%.

The Fed's policy statement indicated that officials anticipate that ongoing increases in the target range will be appropriate, and Chair Jerome Powell noted in his press conference that a change of 50 or 75 basis points is likely in July.

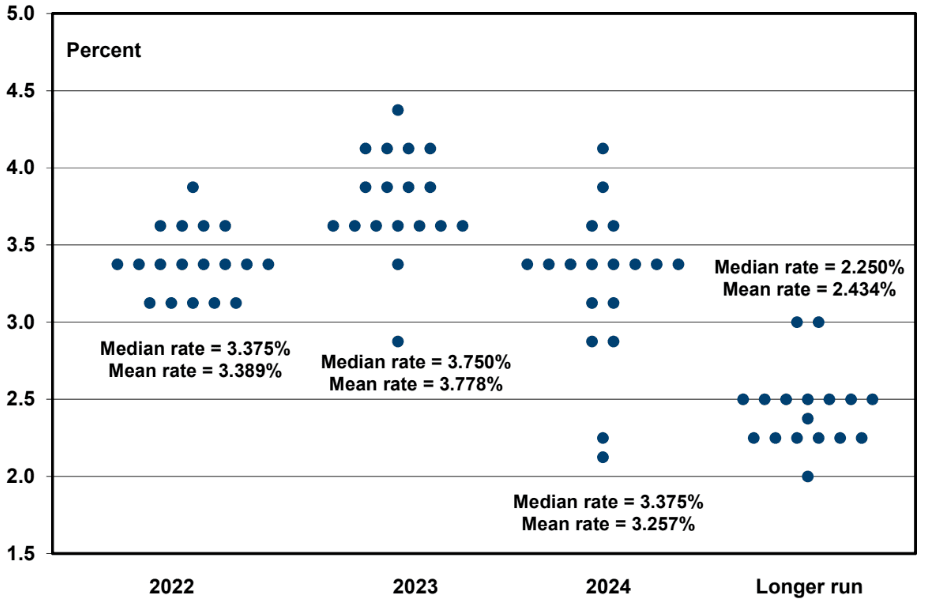

Importantly, the new dot plot of FOMC voters' projections shows a median expectation for a federal funds rate of 3.375% at the end of this year, above the perceived neutral rate of 2.5%.

The move above neutral means U.S. monetary policy will become decidedly contractionary, which should quell domestic inflation expectations but also slow economic growth and provide support to the Dollar which tends to outperform in times of economic stress.

Projections of the Funds rate shows the FOMC expects it to be at 3.4% by the end of 2022, up on the previous estimate of 1.9%. It is seen at 3.8% by the end of 2023 (previously 2.8%) and 3.4% by the end of 2024 (previously 2.8%).

Above: The FOMC's projections. Image courtesy of Daiwa Capital Markets. See appendix for description.

"We expect that the hawkish Fed will tighten financial conditions, push global rates up and support the Dollar over time," says economist Ebrahim Rahbari at Citi.

Economists at Westpac now look for a second 75bp hike in July followed by a 50bp move in September (both +25bp on their prior forecast). Two more 25bp hikes are then expected in November and December (unchanged from their previous forecast), taking the fed funds rate to 3.375% at peak end-2022.

But importantly Westpac sees the rate hiking cycle ending at the end of the year and this suggests limited potential for further major gains in the U.S. Dollar.

"The consequence for the US dollar is that we continue to see it as being near its peak for this cycle," says Elliot Clarke, an economist with Westpac.

FX Strategist Francesco Pesole at ING Bank is however looking for further Dollar strength in the wake of the 75bp hike and guidance for further hefty hikes.

"We deem it unlikely that investors will turn materially less bullish on USD in an environment of accelerating Fed tightening, sharply rising Treasury yields (and inverted yield curve), the prospect of a global slowdown and equities in bear-market territory," says Pesole.

The rapid rise in U.S. interest rates will raise the cost of borrowing and ultimately dampen consumer activity as mortgage rates shoot up and the wealth effect of falling stock markets is felt.

It will potentially also increase the use of savings accounts as the cost of holding cash improves.

The question facing economists is whether or not this results in a U.S. recession.

"The FOMC’s strong commitment to dampen inflation raises the risk of a US recession in our view. History shows the FOMC has struggled to engineer a soft economic landing," says Carol Kong, a strategist with CBA.

Research from HSBC finds a U.S. recession is ultimately supportive of the U.S. Dollar.

"If the market is concerned about the tail risks of a possible US recession, it should be buying the USD, not selling it. In most instances, this is backed up by the performance of the USD during peak-to-trough economic cycles in the US," says Daragh Maher, Head of Research for the Americas at HSBC.

But economists at Pantheon Macroeconomics don't yet see a recession as being a given.

"A central bank promising to hike until inflation is clearly falling is effectively promising to overtighten," says Ian Shepherdson, Chief Economist at Pantheon Macroeconomics.

"But the healthy state of the private sector’s finances mean that a recession should be averted," he adds.

For the Dollar to fall the U.S. economy would most likely need to avoid recession and the global economy would need to start growing again.

"The FOMC’s strong commitment to dampen inflation raises the risk of a US recession in our view. History shows the FOMC has struggled to engineer a soft economic landing," says Carol Kong, a strategist at CBA.

About the dot plot: * Each dot represents the expected federal funds rate of a Fed official at the ends of 2022, 2023, 2024, and long-term. Normally, this graph would contain 19 projections (seven governors of the Federal Reserve Board and 12 reserve bank presidents), but one governorship was open at the June 2022 meeting. Moreover, only 17 Committee members provided forecasts for the long-term projection. Source: Federal Open Market Committee, Summary of Economic Projections, June 2022.