- GBP/USD supported at 1.38 and looks to reclaim 1.40.

- With economic, central bank policy divergence growing.

- UK data deluge and litany of Fed, BoE speakers ahead.

- As broad USD gains elsewhere call for GBP/USD upside.

Image © Pound Sterling Live

- GBP/USD spot rate at time of writing: 1.3870

- Bank transfer rate (indicative guide): 1.3485-1.3582

- FX specialist providers (indicative guide): 1.3662-1.3773

- More information on FX specialist rates here

- Set an exchange rate alert, here

The Pound-to-Dollar exchange rate was dealt a setback last week but remains well supported on the charts while the UK's economic blessings continue to make a compelling case for further gains back to and above the 1.40 threshold over the coming days, as central bank policy divergences proliferate.

Sterling's performance was chequered in a week dominated by a resurgent Dollar, rising bond yields and central bank policy decisions, with the Pound-to-Dollar rate ending the period -0.4% lower while having remained comfortably above a cluster of technical support levels located around the 1.38 handle.

With the exception of USD/JPY, Dollar exchange rates were bolstered further amid continued gains for U.S. yields and optimism about the outlook for the world's largest economy, which prompted most major currencies to retreat from the greenback steadily throughout the week.

"While the Bank of Japan’s adjustments to its policy framework have limited near-term market implications, we think they are illustrative of differing outlooks that will ultimately lead to further divergence in yields of long-term government bonds across countries," says Thomas Mathews, at Capital Economics. "We think flash PMIs in the UK and Eurozone will point to activity remaining subdued."

The Yen pushed back against the Dollar after the Bank of Japan (BoJ) announced what might have been an interest rate rise in disguise as well as a fine example of the central bank policy divergence that now looks set to dominate the FX market agenda over the coming months.

Thursday sees the Swiss National Bank (SNB) say its part days after the Federal Council in Berne cited "a deterioration in the epidemiological situation," for postponing any further easing of restrictions on activity.

This could mean further upside for USD/CHF and GBP/CHF in the week ahead, even in the possibly unlikely event that GBP/USD ends up sidelined again.

"We remain broadly bullish," says Juan Manuel Herrera, a strategist at Scotiabank, who's warned of some possible sideways trading for Sterling this week. "Support should firm up around 1.3820 now, where trend and the 50-day MA converge. A move above 1.40 should prompt a retest of 1.42 fairly quickly."

Above: Pound-to-Dollar rate at daily intervals with Fibonacci retracements of mid-January rally & 55-day average (yellow).

"Elliott waves are all positive and we would allow for a further upside attempt," says Karen Jones, head of technical analysis for currencies, commodities and bonds at Commerzbank. "Provided the 55-day ma holds, we would allow for a retest of 1.4018 (last week's high), and this guards 1.4238/44 (recent high)."

This was after a week in which the Federal Reserve (Fed) and Bank of England (BoE) gave more optimistic assessments of their economic prospects and made no complaints about recent increases in bond yields, which have proven a draw for currency market investors on boths sides of the Atlantic of late.

Meanwhile, Italy and France returned many large population centres to 'lockdown' last week while Germany warned restrictions may remain in place longer than planned. The virus, vaccination and economic situation in Europe calls for a near-term depreciation of some continental currencies.

"The ECB has made clear that they’ll fight any unwarranted import of higher yields from the US, and so far, it’s working," says Eric Nielsen, group chief economist at UniCredit Bank. "The central banks in vulnerable EM countries face a more complicated task than the ECB."

Above: US Dollar and Pound rally against JPY and CHF, but could have further to go.

Europe's single currency faces economic risks that would demand a lower effective exchange rate of any functional market but declines in the Euro-Dollar rate would make depreciation more difficult and less likely for the Swiss Franc, Swedish Krona and Polish Zloty among others.

"We see more GBP upside near term given the fast UK vaccination rate, but we are long-term bearish because Brexit reduces the UK's growth potential. We are bearish on CHF, particularly vs. USD, and constructive on the commodity block," says Michalis Rousakis, strategist at BofA Global Research.

One equilibrium and possible path of least resistance would be a more nuanced Dollar picture that lifts GBP/USD sufficiently enough for the overall trade-weighted Euro to depreciate through increases in GBP/EUR, while a steady EUR/USD enables depreciation for other troubled European currencies.

However, it could be the case that Sterling first needs to navigate the deluge of economic data due out of the UK and pending series of speeches from Bank of England interest rate setters before the Pound-to-Dollar rate is able to reclaim 1.40 and resume toward higher levels.

"We see the risk environment as likely to stabilise next week and a likely range bound EUR/USD, thus the similar trading dynamics should be present in GBP/USD. Still, the bias remains for modestly higher GBP/USD and the return back to the 1.40 level given the positive GBP outlook driven by the fast vaccination process and the expected sharp economic rebound in 2Q," says Petr Krpata, chief EMEA strategist for FX and interest rates at ING.

Above: Pound-to-Dollar rate shown at daily intervals with EUR/USD (purple) and GBP/EUR (blue).

"It will be very busy week on the UK date front next week, but after the March BoE meeting this week (where the central bank did not lean against higher bond yields), these should have a limited impact on sterling," Krpata says.

A broad Dollar turn lower against all but the lowest of yielders like the Swiss Franc and certain other European currencies cannot be ruled out this week either however, given its already-large months-long rally and the litany of speeches from Fed policymakers in the calendar each day this week.

"While the Fed, BoC, Norges Bank, RBA and the BoE have welcomed the latest rally in bond yields, the ECB and the BoJ have pushed back against the tightening of global financial conditions," says Valentin Marinov, head of FX strategy at Credit Agricole CIB. "Policy divergence is here to stay and could fuel demand for FX carry trades where investors buy the USD, CAD, NOK, AUD, NZD and to a lesser degree the GBP and sell the JPY, the CHF and the EUR."

No less than five Federal Open Market Committee members are set to speak about assorted topics from various locations on Monday alone, with three more on Tuesday, a further three on Wednesday and no less than six addresses over the course of Thursday before the Fed falls quiet for the week.

Fed Chair Jerome Powell's Tuesday and Wednesday appearances before Congress are the highlights although all of the speeches are opportunities to hammer home the message that while unfazed by rallying yields, investors are jumping the gun by expecting the Fed to raise rates as soon as 2022.

Above: Selected yields. Green & Red (10-year Norwegian yield) Blue line (10-year GB yield), Red line (10-year U.S. yield). Yellow line (10-year Italian yield). Clicking this image will enlarge it within a new browser tab.

"While we still see scope for further USD gains over the short-term, we feel the upside from here is beginning to diminish," says Derek Halpenny, head of research global markets EMEA and international securities at MUFG.

U.S. vaccine success and a $1.9 trillion spending package are a big part of why the Fed showed little concern about bond yields, some of which have doubled this year, although the bank remains averse to investors' recent expectations for it to lift rates as many as three times by the end of 2023.

This is not least because the U.S. central bank now seeks to generate more inflation than was the case previously or is the case elsewhere in the G10 world, which necessitates a lower-for-longer rate stance. Its new average-inflation-targeting strategy requires a period where inflation is allowed to rise above the 2% target without eliciting Dollar-positive rate rises, with the idea being to compensate for past periods where inflation has been below target.

Official measures of inflation have "averaged slightly below 2 percent for over a quarter-century," which is what the Fed is seeking to rectify and means that U.S. policymakers are likely to be slower lifting interest rates coming out of the coronavirus crisis than when emerging from past crises. Parts of the financial markets may be yet to fully get the message and its implications, although this week's speeches from FOMC members could help them do that, which would be supportive of the Pound-Dollar rate.

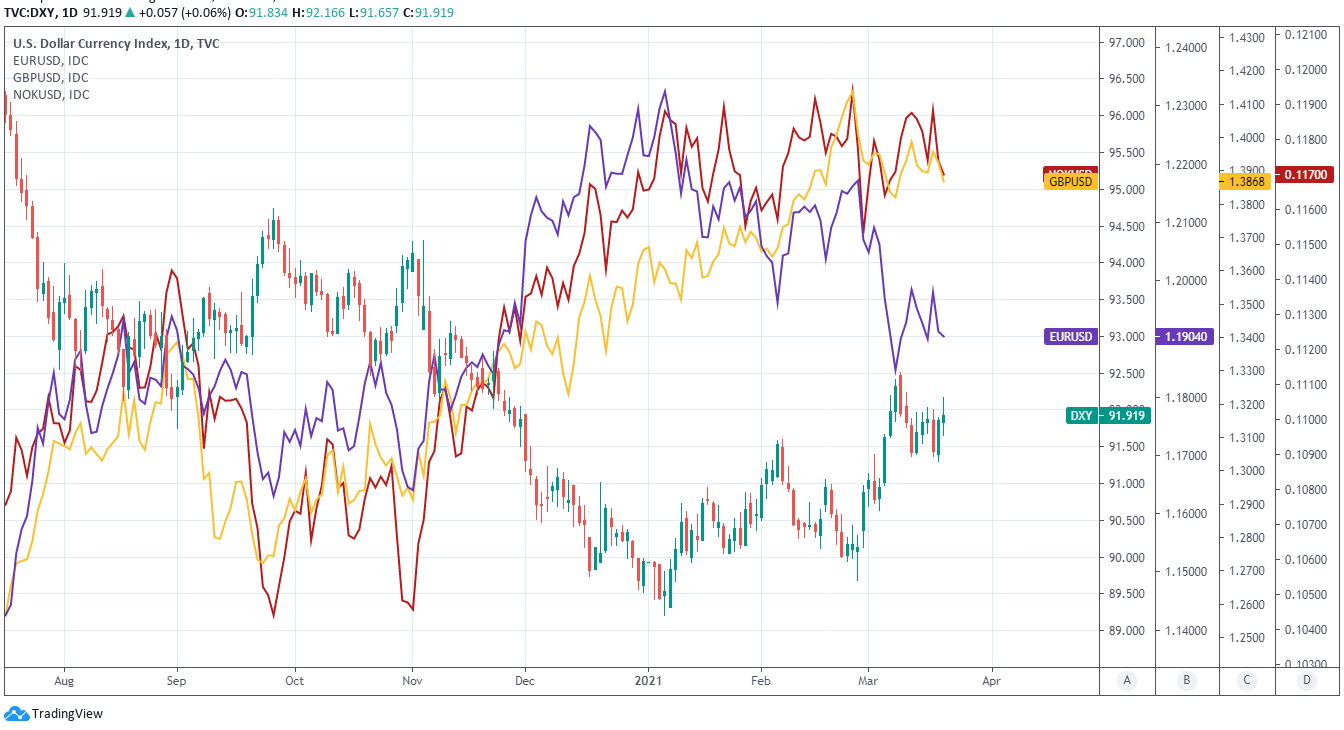

"The Bank of England's stance was in sharp contrast to the ECB last week, which has planned to increase the pace of its QE purchases, and even the Fed," says Jacqui Douglas, chief European macro strategist at TD Securities. "We look for sterling to outperform EUR but lag NOK as the theme of intra-European divergence begins to get more traction."

Above: Dollar Index shown at daily intervals wtih EUR/USD (purple), GBP/USD (yellow) and NOK/USD (red).