Above: Federal Reserve Chairman Jerome Powell. Image © Federal Reserve.

- GBP/USD spot rate at time of writing: 1.3915

- Bank transfer rate (indicative guide): 1.3510-1.3607

- FX specialist providers (indicative guide): 1.3688-1.3799

- More information on FX specialist rates here

The Dollar went from hero to zero on Wednesday when in metaphorical terms the runaway U.S. inflation picture effectively bombed at the box office, with February's data coming in lower than was expected by economists and in the area where it really mattered most that it didn't.

U.S. inflation rose at a month-on-month pace of 0.4%, in line with market expectations, which lifted the annual rate of inflation from 1.4% to 1.7% and left it sitting just shy of the 2% target coveted by the Federal Reserve (Fed).

But and on the downside for the Dollar, the more important rate of core inflation rose by only 0.1% from January and not enough to prevent the annual rate falling from 1.4% to 1.3%. Consensus had favoured a 0.2% increase.

Core inflation ignores volatile energy and food goods as well as regulated price items like alcohol and tobacco, so is thought by central bankers to provide a more accurate reflection of true underlying inflation trends in the economy.

"These data don’t tell us anything about the post-Covid outlook, which initially will be a story about margin-rebuilding in the services sector. Later, the wage response to that initial increase will be key. The exception is rents, where the upturn now underway is entirely consistent with rising rental demand, soaring home prices, and record increases in landlords’ asking rents," says Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Shepherdson says the main headline rate of inflation was held back by an unsustainable fall in the cost of jet fuel and that it's likely to rise further in the months ahead, although increases in the main measure of price pressures are not enough for investors, the Fed or the U.S. Dollar.

Wednesday's core inflation rate is more important but couldn't have been worse for currency, bond and stock markets that had in recent weeks gotten hot under the collar over upside risks to the Fed's inflation target.

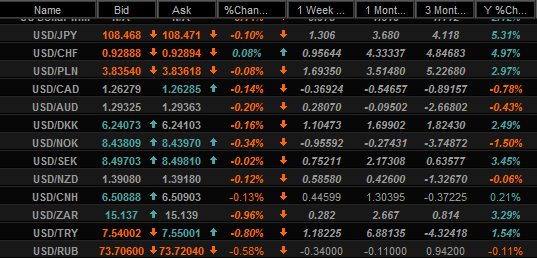

Above: Quotes and performances for selected U.S. Dollar exchange rates. Source: Netdania Markets.

The core number likely explains how the Dollar went from intraday gains over most major rivals, to near the bottom of the bucket after the release.

The Dollar was left trailing only the low-yielding and safe-haven Swiss Franc as hot air escaped all other U.S. exchange rates, which had been charged up in recent weeks by an often-destablising surge in American bond yields.

U.S. progress ramping up its vaccination campaign has bolstered expectations for growth this year and next, while leading some investors to speculate that at least a brief period of runaway inflation could force the Fed to lift its interest rate earlier than the 2023 year it has recently been guiding for.

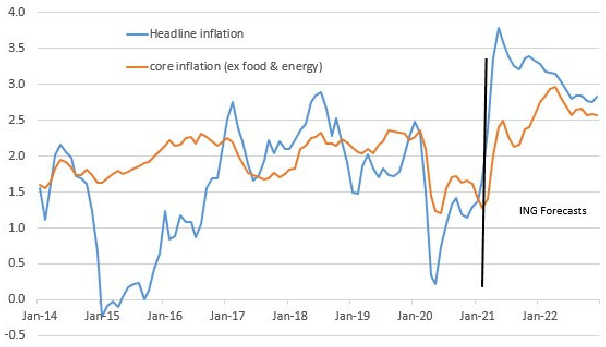

"While officials remain broadly relaxed, we believe inflation could remain elevated through next year, potentially triggering the Fed into earlier action on interest rates than they are currently signalling," says James Knightley, chief international economist at ING. "We are a little less relaxed than Jerome Powell who only last week suggested that high inflation readings will be “transitory” and the notion of “deeply ingrained” low inflation will not fade fast. We are of the view that inflation could stay in a 2.5-3.5% range for the next couple of years which, if correct, implies more upward pressure on longer dated Treasury yields."

Inflation expectations have risen amid unprecedented public financial support for companies and households, although the Fed at least has insisted it won't be spooked or swayed into early rises by "transitory" price changes.

Source: ING Group.

Fed rate setters want higher inflation, and it's what they're obligated to deliver too. They've made clear repeatedly they will want assurance that inflation has risen sufficiently for it to then average the 2% target in a sustainable way, over a period of years rather than mere months, before they raise interest rates.

This is after changing the interpretation of a policy objective that's only loosely defined in statute. Chairman Jerome Powell announced at the 2020 Jackson Hole Symposium that the Fed will now interpret the price stability mandate and view its self-imposed 2% target in a more symmetrical manner, which means it's unlikely to raise rates until inflation has risen above target for something like just as long a period as has been spent beneath it.

Many economists still expect U.S. inflation to rise notably this year and next, and far above the Fed's target too, although this would reflect attainment of the bank's objective and won't necessarily lead it to risk squandering that higher inflation by prematurely raising its interest rate. Central bankers the world over are tasked with using rates to manage inflation, normally with a view to keeping it steady at what are generally and in the developed world at least, 2% targets.

"A burst of transitory inflation seems more probable than a durable shift above target in the inflation trend and an unmooring of inflation expectations to the upside. When considering the inflation outlook, it is important to remember that inflation has averaged slightly below 2 percent for over a quarter-century," says Fed Governor Lael Brainard last Tuesday, reflecting sentiments that were subsequently echoed by Fed Chairman Jerome Powell in discussion with The Wall Street Journal. "While the progress on vaccinations is promising, jobs are currently down by 10 million relative to pre-pandemic levels."

Above: Pound-to-Dollar exchange rate shown at daily intervals alongside ICE U.S. Dollar Index (black line).