- GBP vulnerable to retracement as fundamental backdrop sours.

- Rising ex-U.S. virus cases threaten European currencies Vs USD.

- USD rebound looms but analysts see downtrend remaining intact.

- China tensions, economic data to weigh although Fed a wild card.

Image © Adobe Images

Achieve up to 3-5% more currency for your money transfers. Beat your bank's rate by using a specialist FX provider: find out how.

The Pound-to-Dollar exchange rate advanced further amid a continued sell-off in the greenback but that weakness has left some risk currencies over-extended against the U.S. unit while the fundamental backdrop is souring and could prompt a downward correction for Sterling in the coming days.

Sterling ended the week on its front foot after economic data challenged the popular perception of an economy lagging its rivals in the race out of the coronavirus trough. Brexit negotiations went almost nowhere, although the ongoing deadlock was not enough to trouble Sterling beyond Thursday.

Aided by Friday's data the Pound reclaimed its 200-day and 55-week moving-averages last week but was left knocking on the door of the 78.6% Fibonacci retracement of its March collapse, at a point when the Dollar is oversold and the fundamental backdrop is becoming supportive of a correction.

U.S.-China tensions are rising and second wave outbreaks of coronavirus in Spain, Japan, Hong Kong and others are drawing attention while stock markets have begun to soften. All are a recipe for a potential correction by the Dollar, which has been penalised of late owing to its own second wave.

Recent gains have left Sterling, the Euro and a range of other Dollar Index constituents vulnerable to a deteriorating fundamental backdrop that could encourage a correction over the coming days and a now-rare moment of stability for the barometer of the U.S. unit.

All risk currencies gained over the Dollar last week but Friday saw the Canadian Loonie crack and the coming days may see weakness spread if the Federal Reserve (fed) is unable to revive the stock market rally at 19:00 on Wednesday.

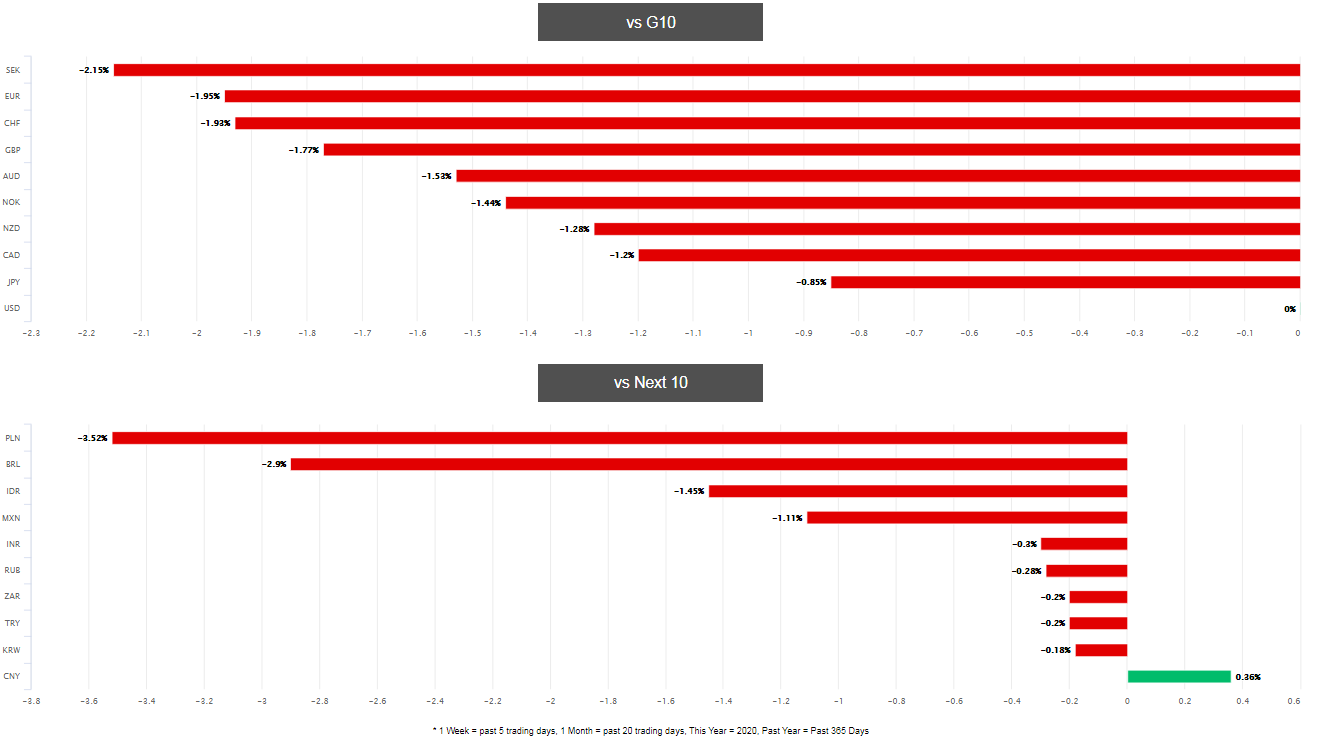

Above: U.S. Dollar performance against major developed and emerging market currencies last week. Source: Pound Sterling Live. Click for larger image.

"Tensions between the US and China have contributed to a halting in the risk-on rally, but have equally failed to trigger any substantial correction as equities continue to treat geopolitics with a good dose of complacency. The coming week will likely test such approach as tensions may escalate to a point where the US-China trade deal appears jeopardized," says Petr Krpata, chief EMEA strategist for currencies and bonds at ING. "The dollar will remain tied to risk-sentiment swings, although more bad data (US 2Q GDP figures next week, along with the key jobless claims) may put a lid on its ability to rally on risk aversion."

Krpata says GBP/USD and EUR/USD should pause for a breather next week after their May recoveries were extended in the weeks since late June.

He also flags the Swedish Krona as vulnerable following a recently relentless advance on the greenback, while colleague Francesco Pesole is looking for a largely range-bound USD/CAD rate that trades between 1.3340 and 1.35.

"We continue to feel the DXY is poised to weaken further and will reach 92 or so in the coming weeks. We still prefer to look for opportunities to fade USD strength," says Shaun Osborne, chief FX strategist at Scotiabank. "A close above its 100-week MA (1.2746) for the first time since early-March would signal a willingness for Cable to make a solid push through 1.28 and a test of the 1.30 mark thereafter. Support is 1.2675/700.

Above: Pound-to-Dollar rate shown at daily intervals with S&P 500 (orange), Fibonacci retracements of March fall and 21, 55 & 200-day (green) moving-averages.

Corrections in Sterling, Euro and Swedish Krona could lift the Dollar Index although risk aversion may see the rebound tempered the Japanese Yen and Swiss Franc. Japanese investors return Sunday from public holidays on Thursday and Friday last week, which brought punishing declines for stock markets that risk prompting delayed USD/JPY selling over the coming days.

"The pound has held its ground this week advancing by 1.4% against the US dollar and weakening only modestly by -0.2% against the euro. Despite a lack of progress, market participants are still assuming a last minute trade deal will be reached later this year when the alternative is to impose another self-inflicted shock onto the UK and European economies," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG. "Short USD/JPY looks a safe way to short the dollar at present. The risk to short USD positions at present is the re-emergence of risk-off but USD/JPY should be least responsive to that. Finally, seasonal patterns for USD/JPY shows the coming two months as strongly biased to the downside."

Halpenny says selling of the greenback could go into reverse in the coming week but that USD/JPY is a Dollar exchange rate that has downside potential almost whatever the market mood, given a deteriorating fundamental backdrop for the U.S. economy and the Yen's safe-haven appeal. The Yen tends to push USD/JPY lower in periods of risk aversion while when the market mood brightens, the exchange rate could still fall if international investors come to favour alternatives to U.S. stock markets.

Above: Dollar Index shown at weekly intervals alongside USD/JPY (orange line).

"GBP/USD continues to trade around the 200 day moving average. Further up sits the June peak at 1.2814 and the market will need to clear here in order to generate some real upside interest," says Karen Jones, head of technical analysis for currencies, commodities and bonds at Commerzbank. "Dips lower are expected to remain contained by the 1.2480 July 14 high and the 1.2470 support line...Where are we wrong? Only a slip below the May low at 1.2072 would negate our view for a slide to the 1.1409 March low."

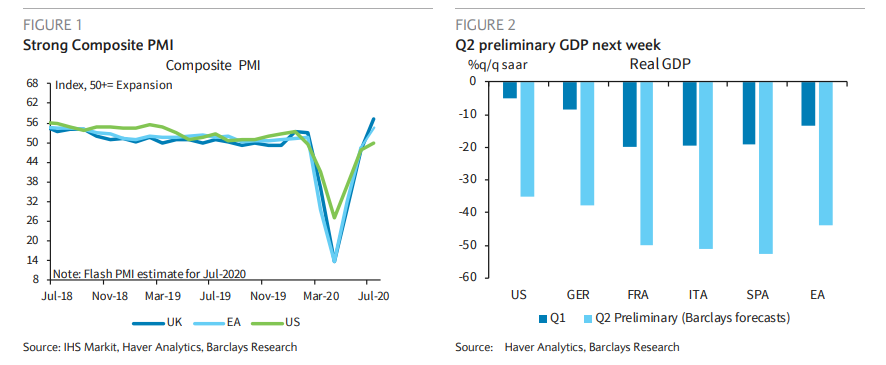

The Pound-to-Dollar rate's upside impetus will be tested in the coming week although this weeks price action follows strong gains on Friday when Office for National Statistics data revealed that UK retail sales surged in June while IHS Markit PMI surveys showed manufacturing and services indices pulling ahead of their Eurozone counterparts for July. This week Sterling will have to contend with U.S. second quarter GDP data and the latest Federal Reserve policy statement.

"With the recovery well underway, we’re often asked about the shape of the path we expect real GDP or employment to trace out. Is it a “U”, a “V’, some other letter? The incoming data increasingly suggest that the US might end up being the VW economy, with no relation, of course, to a certain German carmaker," says Avery Shenfeld, chief economist at CIBC Capital Markets. "Q2 GDP will still capture the down-leg of the cycle. Since April output was so low, even with the economy growing in May/June, the quarterly volume of output was still down sharply from Q1. We’ve pencilled in a 36% annualized decline. But by the same token, June’s GDP was so far above the Q2 average, that Q3 (i.e., the July-Aug-Sept average) will have an easy time registering a solid annualized gain."

Above: Dollar Index shown at weekly intervals alongside S&P 500 Index futures (orange line).

Sterling has been punished in recent weeks for what was comparatively worse economic damage in April when stood next to most other countries, and the near absence of a rebound in May. This has left consensus looking for an -18.2% quarter-on-quarter decline for the three months to the end of June, although if CIBC and other firms are right about the scale of coronavirus-induced destruction in the U.S. then Friday's American number might help to arrest any interim Pound-to-Dollar rate decline.

However, and before that U.S. data is released at 13:30 on Thursday, Sterling, the Dollar and other currencies will first need to navigate Wednesday's 19:00 Fed policy update. The bank has cut the Fed Funds rate to between 0% and 0.25% and launched an unlimited quantitative easing programme in addition to myriad other initiatives designed to support the economy and keep markets' hunger for Dollar liquidity sated. The result has seen an abundance of U.S. washing around the markets.

"We maintain our official Q2 GDP growth forecast at -35.0% q/q saar," says Pooja Sriram, an economist at Barclays. "We expect little new information from the July FOMC meeting. Previous Fed communication has already delivered the message that monetary policy will likely be accommodative for quite some time, if not years. Although the Fed is likely to upgrade its assessment of the incoming data in May and June, the rising number of COVID-19 cases is likely to keep the committee focused on downside risk, the potential scarring of labor markets, and elevated uncertainty."

Above: UK. U.S. & Eurozone PMI surveys alongside Barclays estimates for U.S. and Eurozone GDP figures due this week.